Bullet points on the trends in the Dry Bulk Shipping Sector for 2026

(published on Substack on 6 Feb 2026)

The shipping industry has a few sectors that are engaged in transport: tanker, dry bulk, container, gas (LNG and LPG) and industrial (such as car carriers, chemical, etc.).

In this post, we will focus on the dry bulk sector and its potential for a bullish outlook for 2026. This sector of shipping is related to the transportation of unpackaged bulk cargoes such as grain, coal, iron ore, cement and so on.

The underlying thesis is based on the following assumptions and data:

1. In 2025, China imported 1.26 billion tonnes of iron ore (source: China Iron Ore Imports Hit Record 1.26 Billion Tons in 2025). According to the source, the imports are slated to grow by 2.6 percent and shipments via dry bulk vessels are expected to increase by 36-38 million tons compared to 2025.

2. Brazil’s export of iron ore is expected to remain strong in 2026 after the record export volumes of 2025 (source: After record high, Brazil’s iron ore exports expected to remain strong in 2026 - BNamericas).

3. Vale’s iron ore production is forecasted to be around 335-345 million tonnes in 2026, compared to 336 million tonnes produced in 2025 (sources: Vale lowers its forecast for iron ore production in 2026 - Shanghai Metals Market (SMM); Vale’s iron ore output hits seven-year high in 2025, surpassing Rio Tinto’s Pilbara | Reuters).

4. The Simandou mine, which is located in Guinea (West Africa), holds one of the largest deposits of iron ore and with Chinese interests of 39.95 per cent in the project (via Chinaalco), has already shipped its first cargo (around 200,000 mt) to Ningbo, China (sources: https://www.ft.com/content/80f37963-c718-4f8b-8d77-0f0d5b1c99fe; After years of delay, $24 billion iron ore mine in West African nation ships first cargo to China | Business Insider Africa).

5. The above could be positive for companies that own a fleet of Capesize bulk carriers (which range 170,000-200,000 tons of deadweight capacity) with the usual route being from Brazil to China:

Source: The Baltic Exchange

6. Moreover, the fleet of Capesize bulk carriers is ageing, and the delivery of the new ones (New-Built or NB) is limited. The shipping industry, therefore, expects the Capesize segment to outperform other segments (i.e. Panamax, Handymax and Handysize, source: Stable 2026 and softer 2027 for dry bulk, Bimco predicts).

Taking into account that Capesize bulk carriers have the potential to earn more in 2026 than in 2025, and companies that own the mentioned bulk carriers should benefit from these fundamental factors, we value investors might find a few companies that are undervalued as of today.

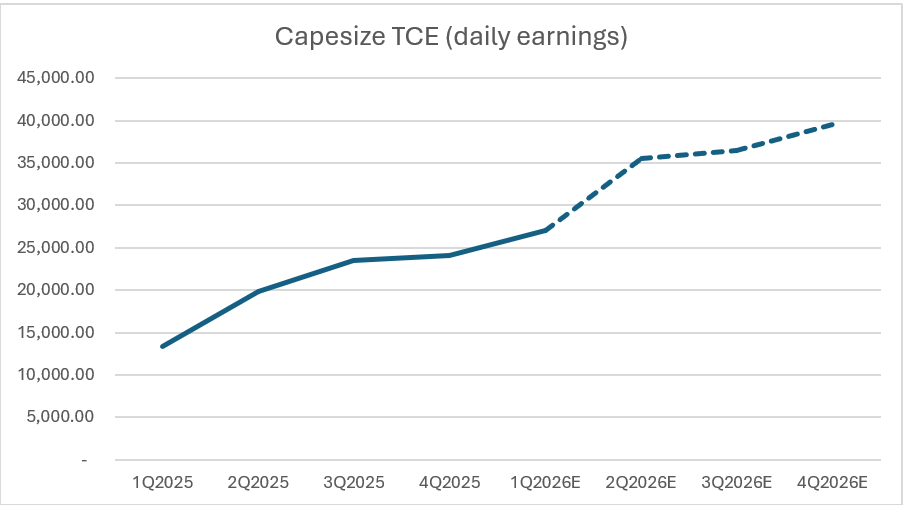

As per my analysis, the average daily earnings or TCE (time-charter equivalent) in 2026 are expected to be around USD 34,625 per day vs USD 20,200 per day in 2025:

Source: Internal analysis

It is worth noting that the term daily earnings or TCE will be used by me often in my research, as it is an important aspect that keeps the shipping company solvent as any other company in this world. The TCE shows how much a vessel earns per day, including the subtracted voyage expenses or, in other words, net earnings per vessel per day.

If the TCE is expected to go up, the market also expects the stock to go up, considering the company’s underlying potential.

Soon, I will publish deep dive research on one of the companies that owns Capesize bulk carriers in its fleet portfolio.

Kind regards,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com