Deep Dive: Okeanis Eco Tankers Corp. (ticker symbols: OET / ECO)

Dear fellow value investors,

Today, we will discuss the company Okeanis Eco Tankers Corp., with ticker symbols ECO (on the NYSE) and OET (on the Oslo Stock Exchange). The company operates in the tanker sector of the shipping industry. The Q1 2026 results for the tanker shipping companies were very strong. But will the current elevated rates remain at their current levels, or revert to their fundamental drivers?

Let’s analyse the business.

Business overview

CO focuses solely on the tanker sector and operates in the VLCC and Suezmax segments. The company was established in 2018 and started trading in 2021 on the Oslo Stock Exchange (ticker symbol: OET), and in 2023, the company was listed on the NYSE under the ticker symbol: ECO (1).

For the simplicity of the research, we will elaborate and show data for the ticker symbol: ECO.

The market capitalisation is around USD 2.1 billion:

Source: Yahoo Finance

The PE ratio at the time of writing is 9.27, and the stock price is up 58 per cent YTD.

As per the annual report of ECO, the major shareholders of the company are Ioannis Alafouzos and Themistoklis Alafouzos:

Source: ECO, Annual Report 2025

In short, the Alafouzos family holds around 46 per cent of the company (out of the total 39,044,655 shares outstanding, as of 31 Mar 2026).

Now, the business is very straightforward. The company owns and manages 17 tankers (8 VLCC and 9 Suezmax tankers). In 2026, they received 3 new Suezmax tankers (2 in Jan 2026 and 1 in May 2026). They expect 1 last Suezmax tanker to be delivered by Jul 2026. So in total, in 2026, the company’s fleet will consist of 18 tankers with an average age of 5 years, which is deemed a young fleet.

The company operates globally and mostly acts in the spot market. Out of its current 17 tankers, only 1 tanker is on a 12-month time charter. Their Suezmax tankers usually operate in the Atlantic region, whereas their VLCC tankers operate globally (Middle East, US Gulf, South America and West Africa).

A very important note that should be mentioned is that the company, until recently, had a few tankers on sale and leaseback financial arrangements. But they closed them all by announcing purchase options for the relevant tankers, which is a good sign for investors, as the balance sheet became less leveraged from a value investing point of view.

The delivery of 4 new Suezmax tankers (3 delivered and 1 is expected by Jul 2026) positions ECO to take advantage of strong tanker freight rates going forward.

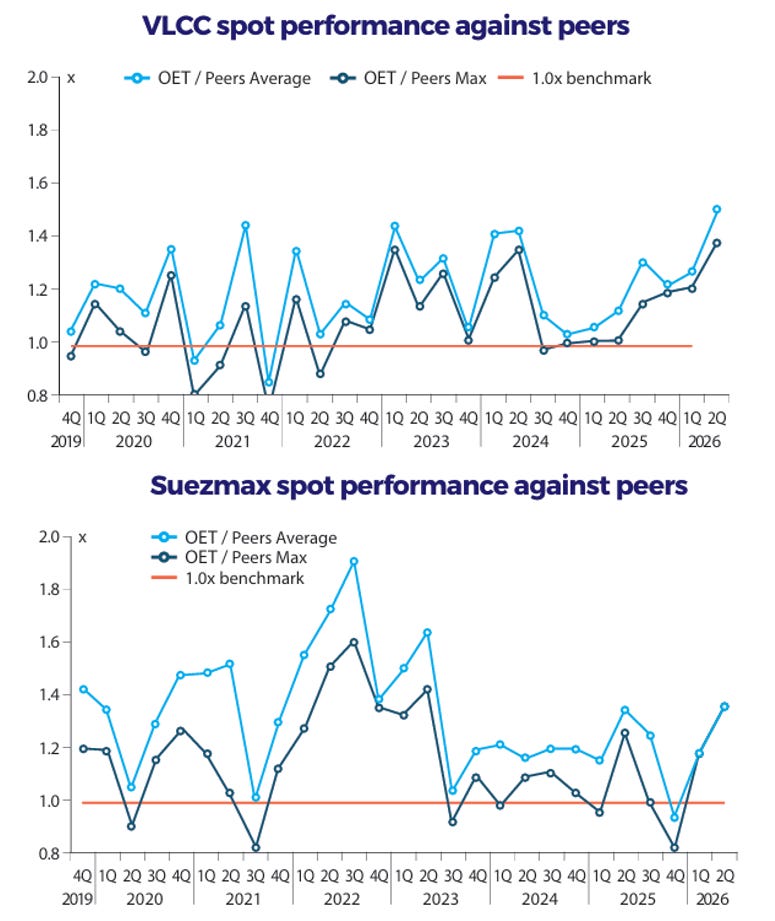

Also, it is worth noting that ECO outperformed its peers in the tanker sector since Q4 2019, both in VLCC and Suezmax segments:

Source: ECO, First Quarter 2026 Presentation

According to management, OET’s superior daily TCE performance versus its peer group generated approximately USD 256 million of cumulative incremental TCE earnings since Q4 2019, which is quite encouraging indeed.

Let’s have a look at their financial metrics.

Financials

As previously mentioned, the Q1 2026 results came in strong:

Source: Internal analysis based on ECO reports

As you can see, the FCF in Q1 2026 is negative, but the cash flow from operating activities is almost the same as the entirety of 2025. The company spent almost USD 197 million as CAPEX, most of which, USD 196 million, was spent on payments related to the delivery of 2 new Suezmax tankers in Q1 2026. The rest (USD 0.9 million) was spent on dry dock surveys. As the company received a new Suezmax tanker in May 2026, we shall expect additional CAPEX related to this delivery. The same is applicable to the Suezmax tanker (Nissos Vous), which is slated to be delivered in Jul 2026. So, in total, we should expect additional payments that will appear in the Cash Flow statements in Q2 and Q3 2026. According to the ECO management, the company expects only 1 drydock expense for 2026 (2).

If we compare the Q1 2026 with Q1 2025 and Q4 2025, we notice a stark difference:

Source: Internal analysis based on ECO reports

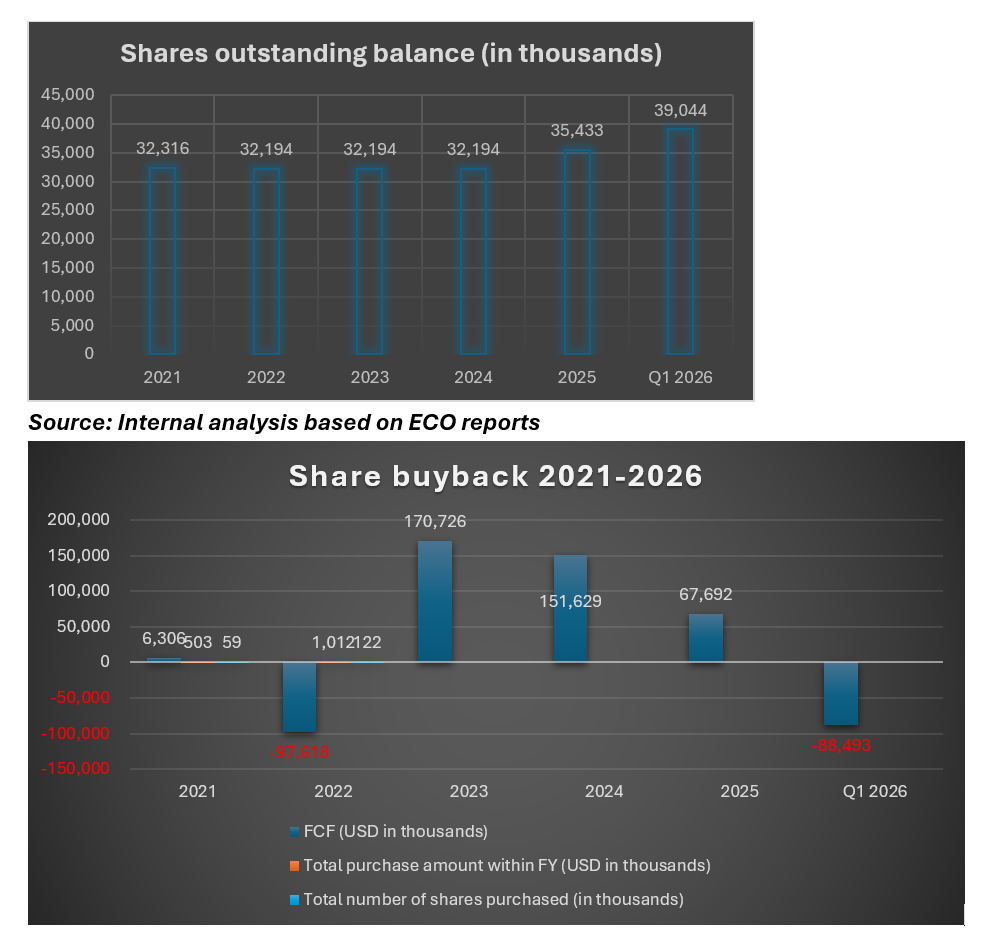

Now, let’s have a look at the number of shares outstanding and whether they conducted any share buy-backs:

Source: Internal analysis based on ECO reports

As you can see from the first chart, the number of shares outstanding has been growing. In 2025, they issued 3,239,436, and in Q1 2026, they issued an additional 3,611,111 common shares. In both cases, the issuance of common shares was related to the investments in new acquisitions and fleet expansion. If we add the above issuances of common shares, we get around 17.5 per cent of dilution, which means the share of the total pie for long-term investors decreased proportionally, which in turn also affects the EPS.

Nevertheless, the company prefers to reward its shareholders via dividend payouts and not via buyback programs.

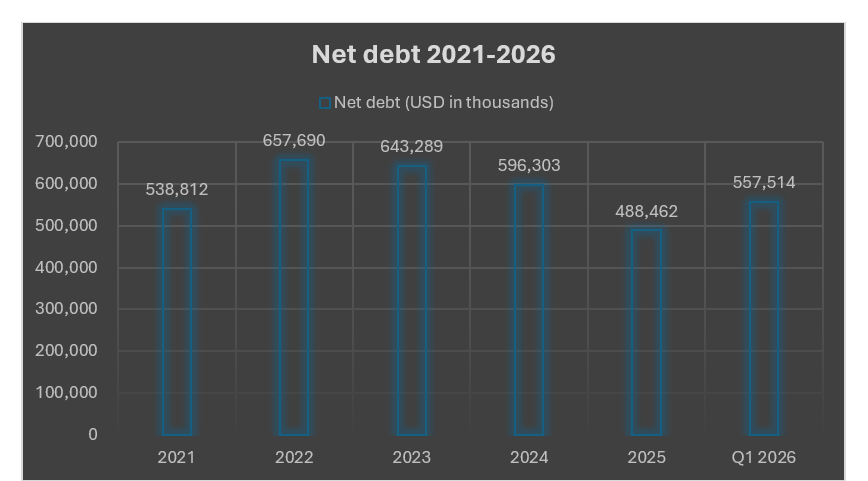

Let’s have a look at how healthy the company is in terms of the net debt, taking into account recent fleet expansion.

Source: Internal analysis based on ECO reports

ECO has been reducing the net debt since 2022, but due to the expansion of the fleet, the net debt is up again. As per the management’s comments, the company will improve this metric.

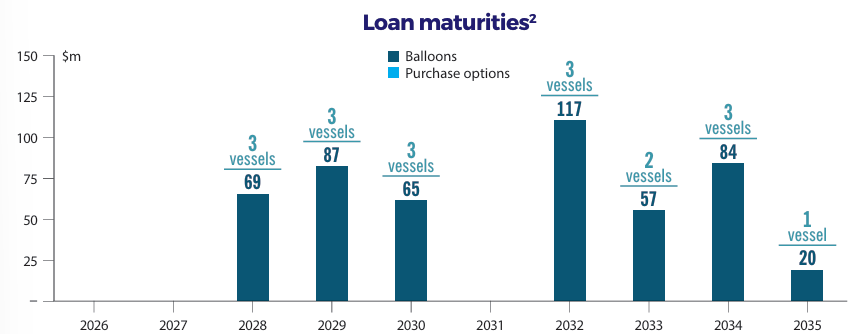

ECO does not have any loan maturities till 2028 and only USD 69 million (3):

Source: ECO, First Quarter 2026 Presentation

The last loan matures in 2035 (as of 31 Mar 2026). Meanwhile, ECO is able to accumulate the cash and should be able to meet its financial obligations in due time. Taking into account the fundamental factors in the tanker segment, we do believe that the company shouldn’t have any issues with the above.

Cash and cash equivalents stand at USD 126 million:

Source: ECO, First Quarter 2026 Presentation

Whereas the stockholders’ equity as of 31 Mar 2026 was at USD 725 million:

Source: ECO, First Quarter 2026 Presentation

Let’s have a look at what we should expect from the tanker market.

Outlook for 2026

Before the outbreak of the Middle East conflict on 28 Feb 2026, we analysed the fundamental factors of the tanker sector and its outlook (for a deep dive outlook, please read the post “Outlook on the tanker market in 2026” published on 13 Feb 2026). In this analysis, we elaborated on the ageing tanker fleet, especially VLCC and Suezmax tankers. Also, in our analysis and the gathered information, we showed that the demand for crude oil in 2026 will be higher than in 2025. So, the fundamental factors were already constructive.

Now, since the outbreak of the war, the freight rates have been elevated. Including the stock prices of the tanker shipping companies. The companies that posted their Q1 2026 results, including ECO, advised that there have been fewer cargoes, but the distance between the ports of loading and discharge increased.

On 14 Jun 2026, the US and Iran agreed to a peace deal. The framework also advises on the reopening of the Strait of Hormuz. As per our view, the reopening of the passage should potentially lead to a short-term spike in the freight rates, which in turn might affect the stock prices, including ECO. The thesis stems from the fact that the drawn crude oil inventories of the consuming nations should be replenished at any cost due to energy security concerns. But upon normalisation of the flow and rebuilding of inventories, we do reckon the freight rates and hence, stock prices of ECO should adjust to fundamental factors.

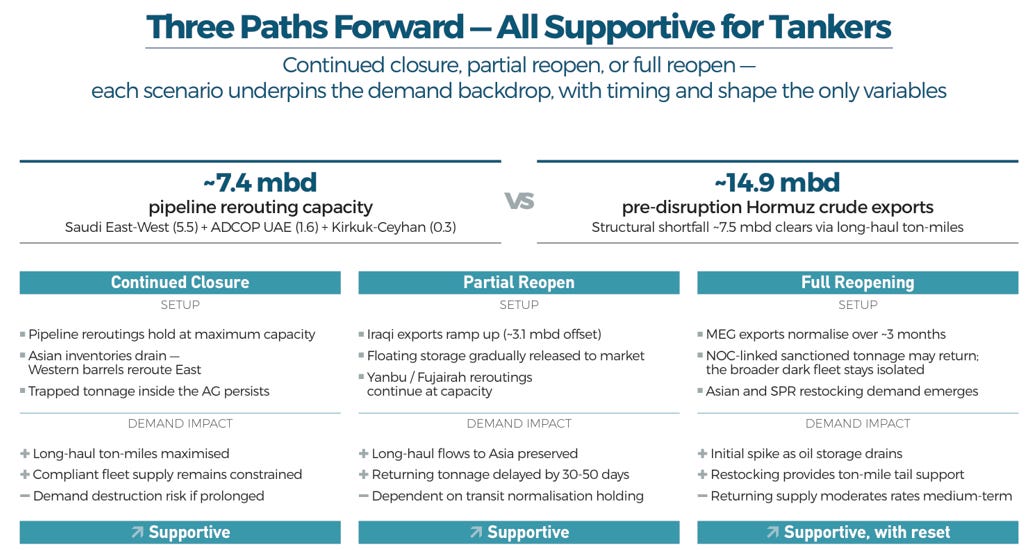

The management of ECO has the same view on the above. They even presented three scenarios:

Source: ECO, First Quarter 2026 Presentation

All three scenarios are supportive of the VLCC and Suezmax tankers. But the last one implies the normalisation of the rates due to the normalisation of the supply of tankers. One should ask oneself: what price is a good buy with low risk/high reward? Let’s elaborate.

We do agree with ECO’s last scenario that the tanker freight rates (especially VLCC) will spike, but the question remains: to what extent and for how long?

Risks

One of the major risks that we have to underline is the potential recession due to a potential economic slowdown, which stems from high energy prices, inflation, high interest rates, etc. But, we do believe that despite this risk, the impact on ECO will be limited due to the fact that crude oil-consuming nations will refill the depleted crude oil inventories at any expense due to its strategic significance.

Another important aspect is related to the freight rates and ECO stock price. The questions that we posed above on the tanker sector are: to what extent and for how long? And what if the tanker freight rates (and ECO stock price) adjust to their fundamental factors faster than we anticipated?

There are too many uncertainties on how it will actually play out, which is a bit of a red flag for a value investor.

Is ECO stock fairly valued, undervalued or at exuberant levels? Let’s evaluate the stock.

Stock valuation

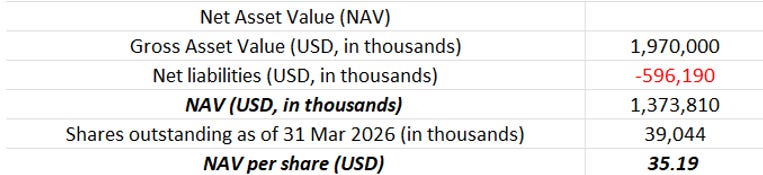

We shall start with the NAV per share calculation:

Source: Internal analysis

So, we get NAV as USD 35.19 per share. The range of analysts pin the 12-month target price at USD 61.50 and 62.00 per share.

The price of ECO at the time of writing is USD 52.12 per share:

Source: Yahoo Finance

If we compare the NAV per share with the current price and analysts’ price target, we can see that ECO is overvalued and there is limited upside (around 11-12 per cent) with a high-risk/low-reward option.

We mentioned in our previous post, “Opinion on tanker segment” published on 05 Jun 2026, that any resolution of this conflict and the potential opening of the passage will be a boon for the tanker segment of the shipping industry. The same was the consensus of the market participants.

But as value investors, we always focus first on the risk. We try to reduce it, and if it is risky, if it appears to be a bet, we focus on other businesses that offer low-risk/high-reward options. Meanwhile, if ECO presents itself at a discounted price, we will again have a closer look at whether the fundamental factors would still justify a buy.

As of now, considering the current price, we shall put the stock on a monitoring list till times when ECO offers better opportunities and the fundamentals are still in place. Nevertheless, we would like to underline that the business in itself looks good and sound. But the price of the stock is a bit high with limited upside.

We will not add it to our Model Portfolio due to the reasons mentioned above, as we simply found other businesses with low-risk/high-reward options.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, don’t hesitate to get in touch with me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Please find us on: https://valueinvestinginshipping@substack.com

Sources:

1 ECO, Annual Report 2025

2 ECO, First Quarter 2026, Earnings Call

3 ECO, First Quarter 2026 Presentation