Deep Dive: A.P. Møller - Mærsk A/S (ticker symbol: MAERSK-B.CO)

(published on Substack on 27 Feb 2026)

Business overview

Maersk A/S is a publicly listed Danish company which deploys container vessels (Ocean segment), operates terminals (Terminals segment), manages warehouses and provides services (Logistics & Services segment):

Source: A.P. Møller - Mærsk A/S

The company has been investing heavily and integrating the logistics and terminal segments.

They manage 721 container vessels, 500+ logistics sides and operate 53 terminals across 20 countries:

Source: A.P. Møller - Mærsk A/S

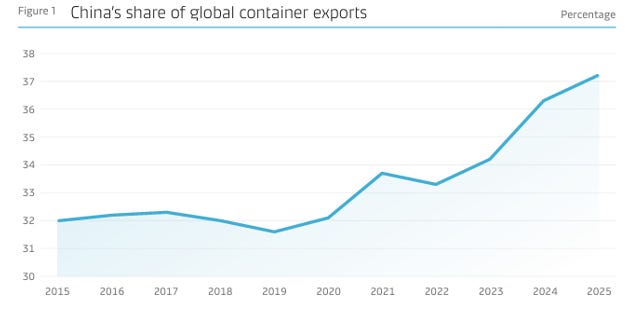

According to the company’s recent 4Q2025 and FY2025 reports, China’s share of the global container exports in 2025 is believed to be more than 37 per cent, which is up from 32 per cent in 2015:

Source: A.P. Møller - Mærsk A/S

Interestingly, their outlook for 2026 forecasts that the global container volume should grow 2-4 per cent more than in 2025. The TEU over 2025 reached 192.9m TEU, which increased from the 184.3m TEU in 2024 (source: https://www.tradewindsnews.com/containers/record-breaking-year-for-global-container-volumes-in-2025/2-1-1942307).

For a more detailed report on the outlook of the container sector in 2026, please see the previous post.

Despite the above positive demand outlook, their financial guidance for 2026 is not so cheerful. We will talk about the risks too (a crucial aspect which relates to the price, from a value investing point of view).

Financials

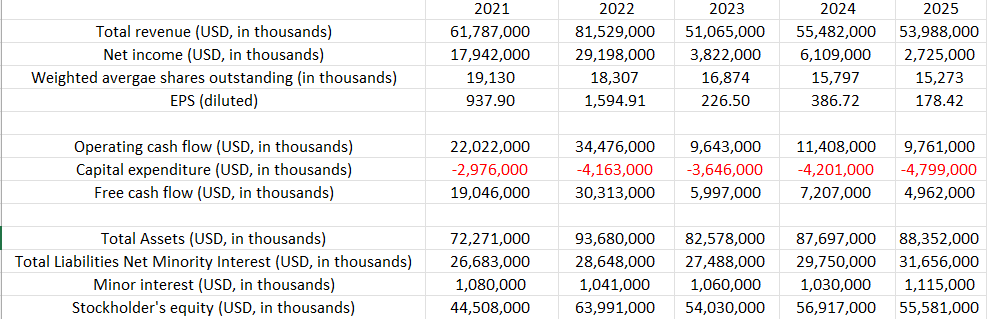

Despite an overall positive 2025, the performance worsened compared to 2024:

Source: A.P. Møller - Mærsk A/S

Source: Internal analysis based on MAERSK reports

Even though revenue and net income were in line with previous years, you can notice that FCF in 2025 is lower than in previous years, due to investments (such as ordering vessels, share buy-backs, dividend pay-outs and investing in their terminals and logistics centres).

The balance sheet is very solid with USD 56 billion in equity (we like it as shareholders):

Source: Yahoo Finance

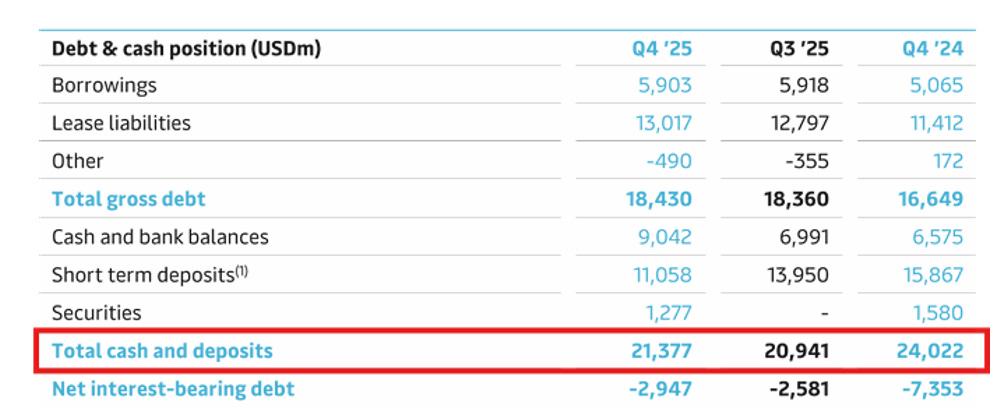

Source: A.P. Møller - Mærsk A/S, Q4 and FY 2025 Investor Presentation

The company sits on USD 21B in cash and deposits, which is good, as it will help ensure the company remains solvent in bad times.

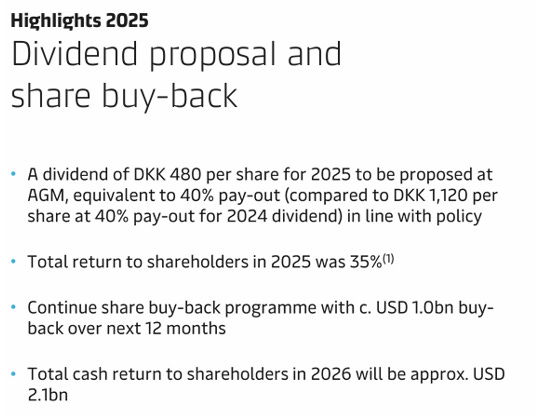

The company has been rewarding its shareholders via dividend payments and share buy-backs:

Source: A.P. Møller - Mærsk A/S, Q4 and FY 2025 Investor Presentation

As you can see from their report (please see above), the segments Logistics & Services and Terminals performed better than the Ocean segment, and even though the company has been investing heavily into the Terminals segment, I will still consider the company as a maritime one, due to the sheer revenues coming from the latter segment.

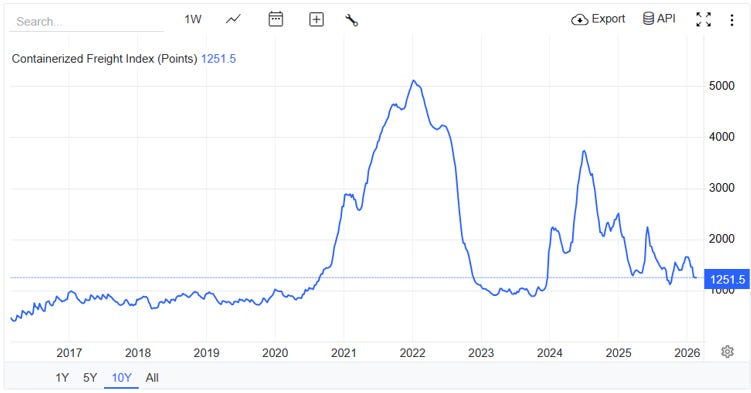

The situation in the Red Sea in 2025 prevented the container rates from slipping, as vessels had to take the longer route via the Cape of Good Hope. However, when in 2026 Maersk and CMA CGM tested the passage via the Suez Canal and the Red Sea, the rates did drop (please see my post dated 20 Feb 2026):

Source: https://tradingeconomics.com/commodity/containerized-freight-index

So overall, the company is doing well financially. However, a high probability of change in wind direction over 2026 and even 2027 is looming.

Risks: What to expect in 2026?

As per usual, our approach to identifying the risks will be a bottom-up approach, and we shall evaluate these risks against the current stock price.

Now, according to Maersk’s 4Q2025 and FY2025 reports, there are a few important risks to consider, which should be part of our decisions as value investors. Let me begin by reiterating the same points as I did in my previous post dated 20 Feb 2026:

1. Over-capacity of the containership vessels due to the low scrapping rate and high delivery rates in 2026. The current order book is at c. 9.6m TEU, and around 3.3m TEU is slated to be delivered in 2026 (source: https://seagatelogistics.org/news/key-trends-of-container-transportation-shaping-2026/). Since 2023, around 5.1m TEU has been added to the global container vessel capacity, and this saturation with capacity is putting pressure on the container rates.

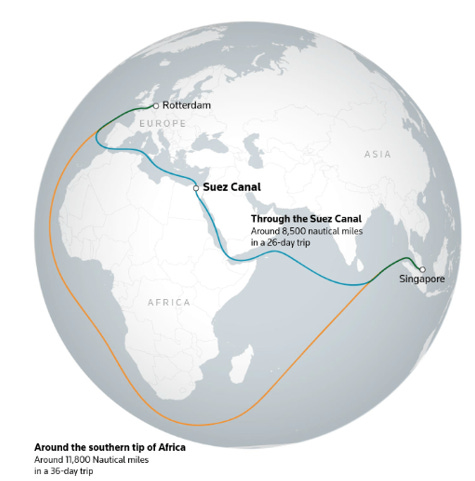

2. The second important risk on the rates will be the full return of the Red Sea and the passage via the Suez Canal, which will shorten the vessels’ route by 10 days, thereby putting pressure on the rates as Charterers will have more vessels to choose from and lower rates can be negotiated:

Source: LSEG

3. The third one is related to a lowered demand for containerised items/goods, a potential recession or in general, the macro-factors.

Stock valuation: Bad times ahead?

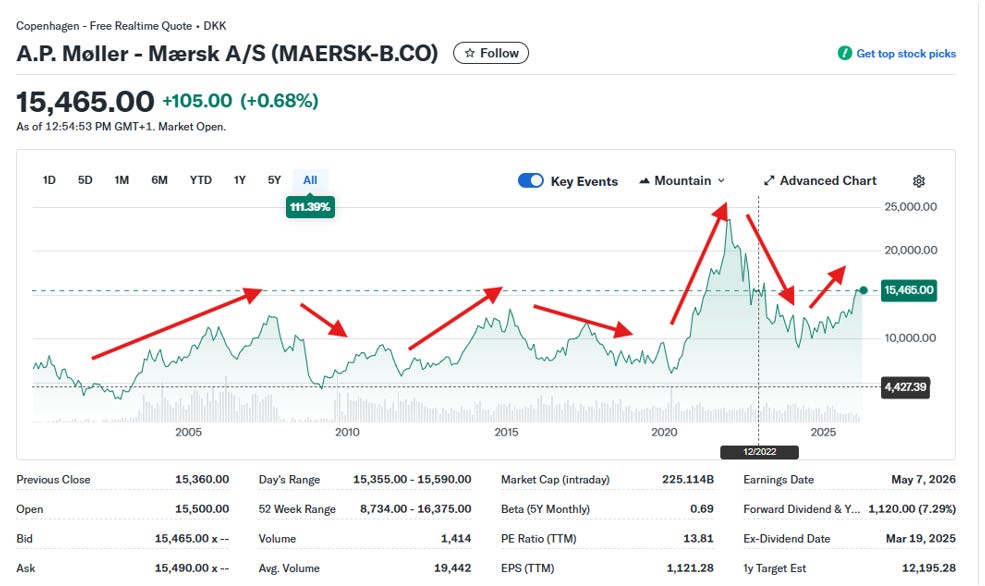

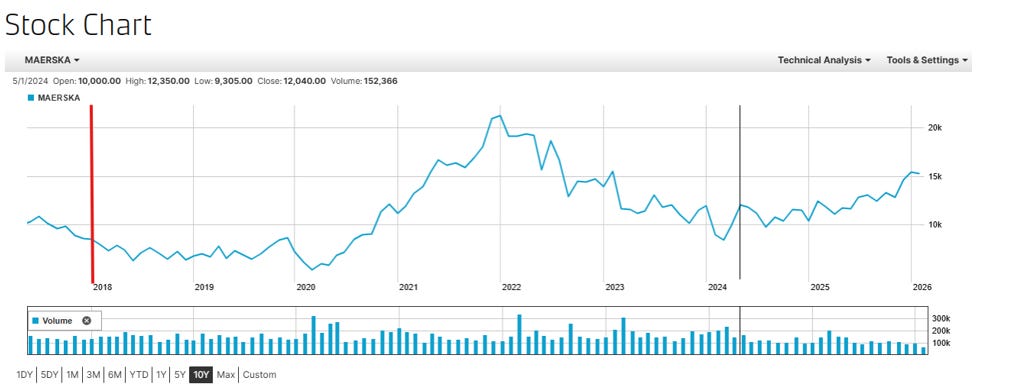

The stock has been trading in cycles with its up and down trends:

Source: Yahoo Finance

By looking at fundamental factors and risks (please see above), and comparing them with the stock price, I believe that the stock price is overvalued, and it might adjust according to the points I laid out above.

Also, the foregoing is being advised by guidance from the company’s management:

Source: A.P. Møller - Mærsk A/S, Q4 and FY 2025 Investor Presentation

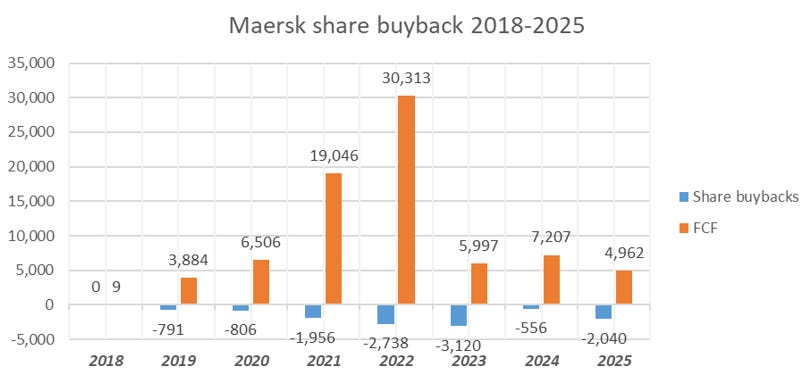

One should expect dividends to be cut as the FCF is expected to be negative (at minus USD 3B and more), and they also reduced by half their share buy-backs, which is a typical approach in today’s business world.

The above chart represents the FCF (in USD billions) and share buybacks (in millions) from 2018 to 2025.

Source: A.P. Møller - Mærsk A/S

As you can see, they purchased fewer shares back when the stock was lower compared to higher prices, which is a typical Wall Street game to purchase back stock when the stock is traded at its highest. Of course, the company needs to preserve capital in bad times, but to buy back shares at its apex, in my view, is a waste of shareholders’ value. Namely, if we assume that the stock price should go from the current levels to, let’s say, DKK 9,500-10,000 range, the money invested in buying back stocks is wasted, i.e. down the drain. In my view, that’s a very bad capital allocation.

Now, back to our stock valuation from a value perspective. If we consider all fundamental factors and evaluate from a low-risk/high-reward approach, I do believe the stock is overvalued, and it shall adjust to lower levels. This negative cycle of lower revenue, negative net income and FCF will most likely lead to lower buybacks (and this has already been communicated) and potentially to dividend cuts. All the aforementioned have not been recognised by the market yet, and hence, we witness the current stock price.

No one can say what the exact container rates will be in 2026, 2027 or 2028, but taking into account the supply of newly built vessels and potential return of the Red Sea passage via the Suez Canal, we are looking at factors that can put pressure on the current stock price.

From a value investing point of view, the stock is on the waiting list for a low-risk/high-reward offer. As of now, it is a high-risk/low-reward option, and I do strongly believe that we can find better options.

But as I mentioned before, it is up to you, my fellow value investors, to decide how the position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com