Deep Dive: BW LPG Limited (ticker symbols: BWLPG.OL/BWLP)

(published on Substack on 06 Mar 2026)

Business overview

The company’s market capitalisation is NOK 26.727B (USD 2.768B), and the PE ratio is 16.93. The stock is being traded both on the Oslo Stock Exchange under the ticker symbol BWLPG.OL and on the NYSE under the ticker symbol BWLP.

BW LPG owns and operates one of the largest fleets of LPG carriers. As of the end of 2025, the company manages around 54 vessels:

Source: BW LPG

The average age of their fleet is 9.1 years.

The company has two major business segments: LPG Shipping and Product Services.

LPG Shipping is engaged in providing transportation services for companies that need loading, transporting and discharging of LPG cargoes from the ports of loading to the ports of discharge. The company operates globally, but as mentioned in my previous post dated 03 Mar 2026, most LPG cargoes are exported from either the US Gulf or the Middle East terminals.

The Product Services segment is an in-house trading arm that is involved in the buying, selling and delivering of LPG cargoes.

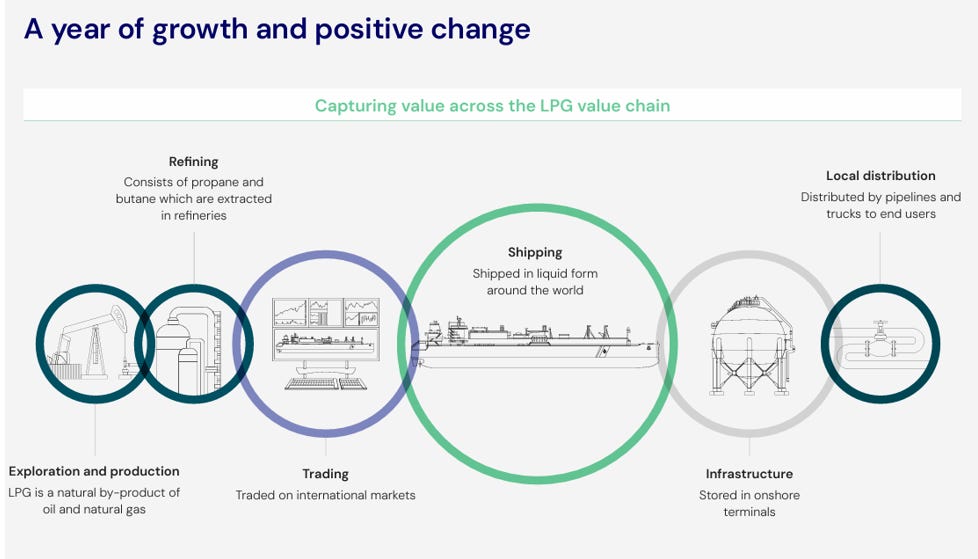

Recently, however, the management started to diversify the business by investing in exploration, production and refining (as LPG is a byproduct of oil and natural gas production) and infrastructure (storage in onshore terminals):

Source: BW LPG, Annual Report 2024

Still, the Shipping and Product Services segments are huge contributors to the company’s revenue:

Source: BW LPG, Annual Report 2025

Financials

Now, let’s look at the financials.

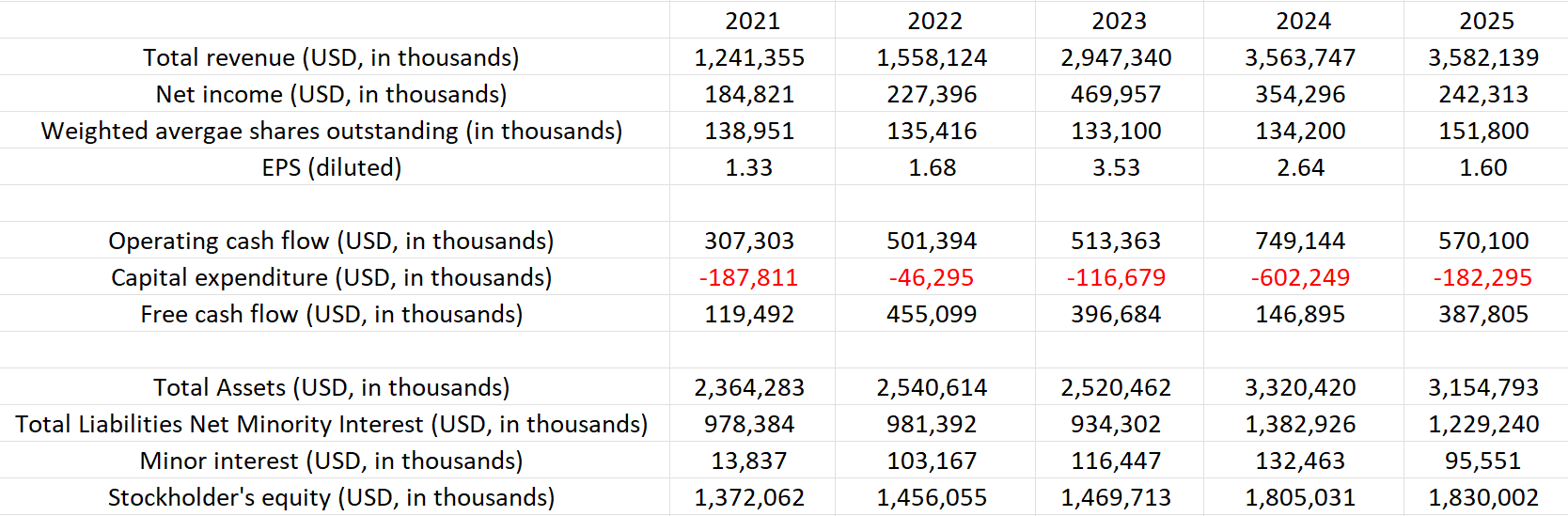

The company’s revenue in 2025 was in line with the previous year. Still, the net income fell due to increased operating vessel expenses, net income loss in Product Service and higher net financial expenses:

Source: Internal analysis based on BWLPG reports

Nevertheless, the revenue and the net income figures have been positive for the past 5 years. FCF has been positive too. In 2025, the company made USD 388m in free cash flow.

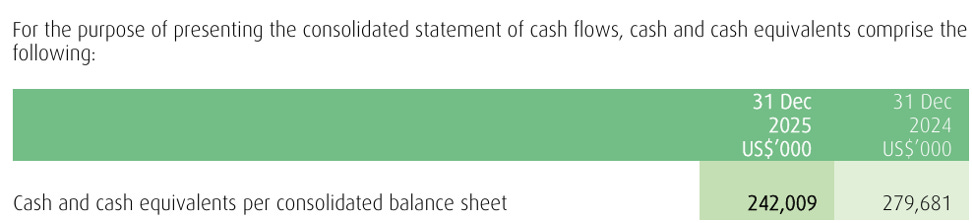

Stockholders’ equity is standing at USD 1.83B as of 31 December 2025. Cash and cash equivalents are at USD 242M:

Source: BW LPG, Annual Report 2025

From the above, we can deduce that the company’s financial health is good.

The company has been rewarding shareholders via dividend payouts in 2025 with an annualised dividend yield of 12.5 per cent:

Source: BW LPG, Q4 2025 Earnings Presentation, 3 March 2026

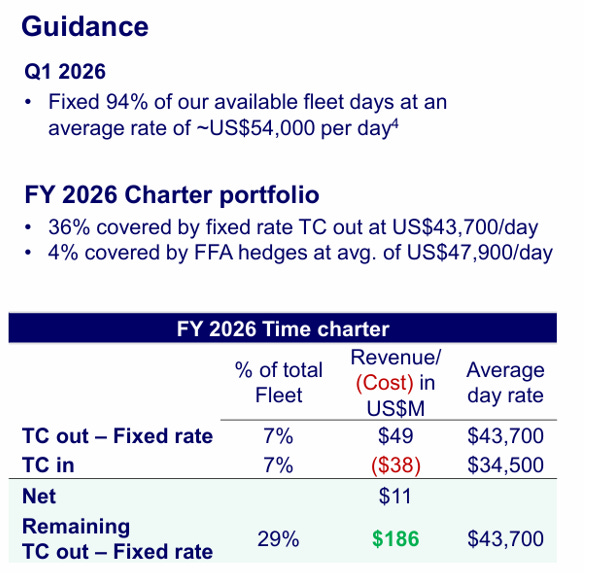

Their guidance of 1Q2026 indicates solid earnings, although the posted figures of the company can be lower than the spot due to recent events in the Middle East and the Strait of Hormuz:

Source: BW LPG, Q4 2025 Earnings Presentation, 3 March 2026

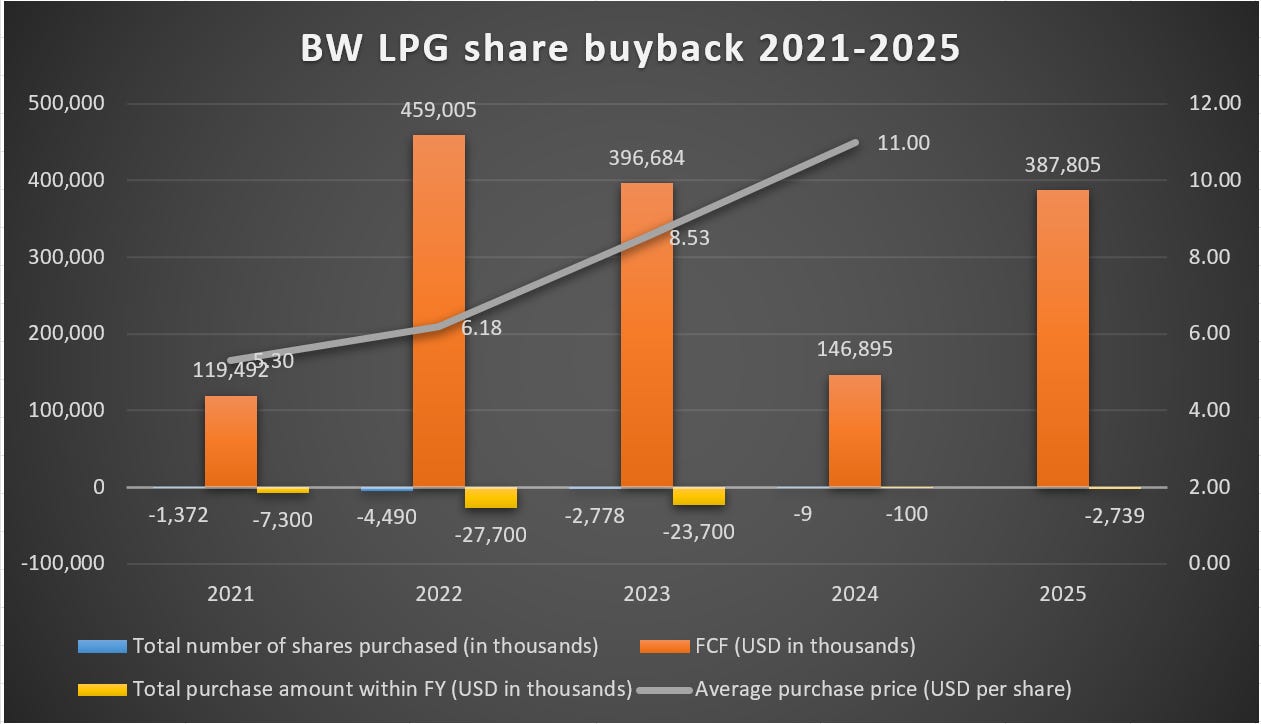

In terms of the share buy-backs, the picture for the past 5 financial years is the following:

Source: Internal analysis based on BWLPG reports

Here is the summary of the share buy-back program for 2021-2025:

Source: Internal analysis based on BWLPG reports

What is remarkable, the company reduced the share buy-back program from 2024 onwards (compared to previous years), by purchasing in 2024 only 9,000 shares worth USD 100,000 (with an average purchase price of USD 11.00 per share) and in 2025, they conducted a share buy-back program worth USD 2,739,000. The information on the number of shares purchased and the average purchase price for 2025has not been communicated yet. We will be waiting for their annual report and will update the missing information (green cells in the table). The company returned to shareholders dividend payouts instead of purchasing shares back at higher price levels:

Source: Yahoo Finance

In the case of dividend payouts, the shareholders can decide by themselves what to do with the cash received, whereas when a company does a share buy-back program at the peak of the stock price, the value is gone if the stock price plummets. So, no value will be created for shareholders.

In this case, the company decided to reward shareholders via dividends, i.e. in 2023 the company paid USD 3.46 per share, in 2024 – USD 2.42 per share and in 2025 – 1.47 per share.

What to expect in 2026?

The company’s outlook is positive due to increased export volume capacity from the Middle East and the consumption of LPG in Southeast Asia:

Source: BW LPG, Q4 2025 Earnings Presentation, 3 March 2026

As I discussed in the mentioned post and based on my fundamental analysis, we have a very constructive outlook. One of the major factors contributing to the positive outlook is the addition of new LPG infrastructure to the current export capacities in 2026 and onwards, both in the US Gulf and the Middle East. Another important aspect is the forecasted increase in the consumption of LPG in Asia (the leading countries are China and India).

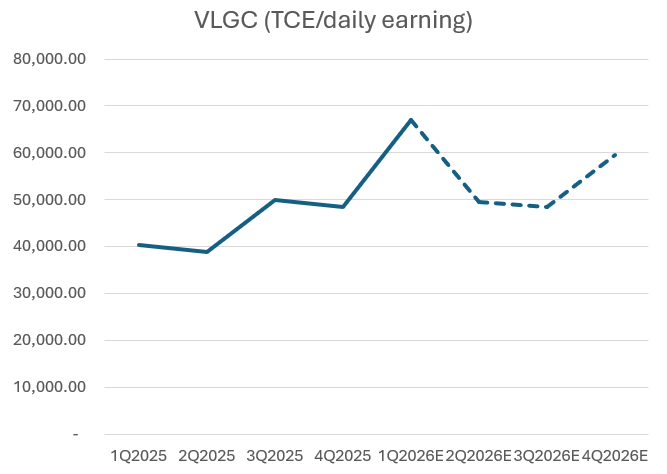

Taking into account the above fundamental factors, the average daily earnings/TCE of VLGC shall be higher than in 2025:

Source: Internal analysis

The current situation in the Middle East will influence daily earnings/TCE in 1Q2026. Baseline of the average daily earnings/TCE of VLGC in 2026, as per my model, should reach USD 56,125 per day vs USD 44,393 per day in 2025.

Risks

The stock price of BW LPG is directly related to the daily earnings/TCE expectation, which in turn is connected to the demand for LPG and demand for LPG carriers. So, any reduced demand for LPG, economic slowdown or a recession shall affect the stock of BW LPG directly, and we shall bear this in mind when we compare risk vs reward.

Is BW LPG stock overvalued now?

Let’s look at the current stock level of YTD and 1 year:

Source: Yahoo Finance

The stock is cyclical and, from time to time, offers a very good entry point with low risk/high reward. As Mohnish Pabrai likes to sum up in his book “The Dhandho Investor: The Low-Risk Value Method to High Returns”: “Heads, I win; tails, I don’t lose much!”

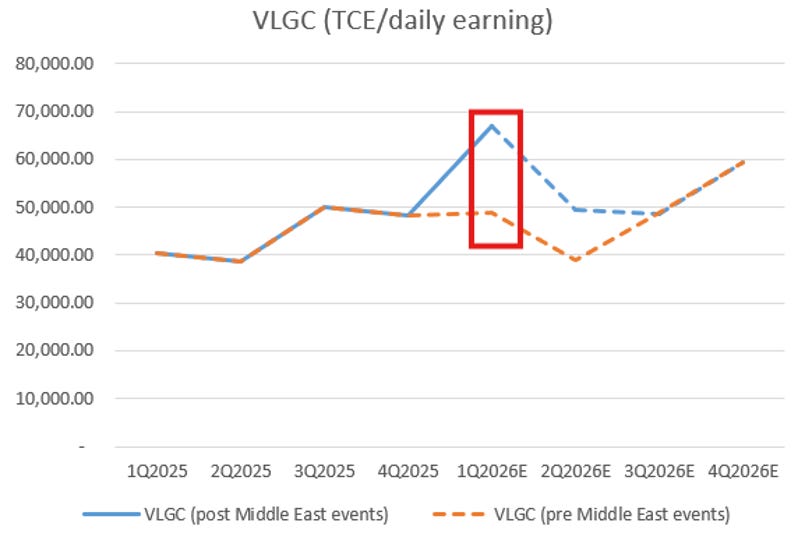

As of today, the stock is 40 per cent up, much of it due to the recent situation in the Middle East. See below my model of the expected daily earnings/TCE of VLGC:

Source: Internal analysis

As you can see, the difference in 1Q2026 in terms of earnings comparing pre- (orange line, conducted in November 2025) and post-recent (blue line) events in the Middle East is around USD 18,000 per day. But as advised before, the actual daily earnings/TCE for 1Q2026 shall be higher than the projected above post Middle East events (blue line).

But is it a buy now? The stock can go higher from the current level, but it can go lower, too, back to fundamental factors. For me personally, it is not value investing but a bet. Namely, when the price is going up, for me, the risks are also increasing. As value investors, apart from the risks mentioned above, we have to avoid buying stocks with high-risk/low-reward options. Once the situation in the Middle East becomes clearer, we can re-evaluate the stock, but as of now, too many pieces of the picture are moving, and it is quite difficult to evaluate the stock level vs fundamental factors.

Patience shall be our beacon, and we have to resist succumbing to FOMO emotions. As mentioned in my comment, “You don’t make money when you buy stocks. And you don’t make money when you sell stocks. You make money by waiting.” – Mohnish Pabrai. And with cyclical stocks such as BW LPG, we have to apply the same principles of value investing.

From a value investing point of view, the stock is on the waiting list for a low-risk/high-reward offer. As of now, it is a high-risk/low-reward option, and hence, we have to wait till the stock offers a better return.

Let’s see how 1Q2026 evolves, and I shall update the analysis of the BW LPG stock.

But as I mentioned before, it is up to you, my fellow value investors, to decide how the position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com