Deep Dive: Danaos Corporation (ticker symbol: DAC)

Dear fellow value investors,

We continue to analyse businesses in the shipping industry, getting familiar with them, understanding how they function, and how they produce cash (as value investors, we are most interested in the cash flow from operating activities) from their core business spheres. And even if they turn out to be expensive with a high-risk/low-reward option at the time of analysis, we still can keep an eye on them, so when they present themselves with a discount against their intrinsic value, we can buy these businesses at a low-risk/high-reward option. Always subject to the analysis of the fundamental factors.

As we discussed in one of our previous posts, sometimes Mr Market wakes up cranky and whimsical, offering certain businesses at discounts. And by continuously analysing the shipping companies, we make sure that we seize the opportunity Mr Market offers and compound our invested capital.

Let’s dive into today’s company, whose business consists of two segments, thereby adding diversification to its business portfolio. Please do enjoy the analysis of Danaos Corporation (DAC).

Business overview

The company Danaos Corporation was established in 1963 by Mr Dimitris Coustas, or “The Father of Danaos”. In 2006, DAC began trading on the NYSE under the ticker symbol “DAC”. So, the company survived all types of crises, including the restructuring of its USD 3 billion debt with 14 lending institutions (in 2010, post 2008 financial crises) and the bankruptcy of Hanjin Shipping (2016-2017), as 20 per cent of contracted revenues were slated to come from eight vessels chartered by Hanjin Shipping.

DAC is engaged in the container and dry bulk transportation businesses of the shipping industry. They own 75 containerships (from 2,200 TEU to 13,100 TEU) and 11 Capesize dry bulk carriers (as of 31 Mar 2026). It is worth noting that 67 vessels out of 86 are debt-free and unencumbered. This fact gives the company a vital competitive edge.

The average age of the current fleet is 18 years for containerships and 16 years for dry bulk carriers.

The company expects 29 new containerships (from 1,800 TEU to 9,200 TEU), which should be delivered in 2026 (3 vessels), in 2027 (15 vessels), in 2028 (7 vessels) and in 2028 (4 vessels). In addition, DAC expects 4 Newcastlemax carriers (dry bulk) to be delivered in 2028.

DAC’s business strategy is to charter out its container carriers to CMA CGM, Hapag Lloyd, COSCO, Maersk, etc., under multi-year fixed-rate charters. This line of business provides stable cash flow and allows DAC to allocate its capital accordingly. For instance, according to the management (1), 100 per cent of its fleet operating days are contracted for 2026, 87.9 per cent for 2027 and 65.3 per cent for 2028. The above includes the new vessels that are expected to be delivered as per above (23 out of 29 new-built containerships have been secured with multi-year chartering agreements). Hence, the company can already forecast its revenues for 2026 and onwards:

Source: DAC, Investor Presentation, May 2026

In contrast to the containership line of business, DAC employs its Capesize carriers on short-term time- and spot charters, which allows the company to capture the upside and, at the same time, exposes the company to the downside of the spot market fluctuations of the dry bulk segment.

The company has another competitive advantage in the form of low daily operating costs per vessel. Namely, according to E. Chatzis (CFO), the company’s daily operating costs are USD 6,680 per day (2).

The company is a shareholder of various companies. For instance, DAC owns around 1.9 per cent of Yoda Plc (ticker symbol: YODA (on the CSE)), which engages in investments in LNG and container sectors of the shipping industry, real estate, etc. DAC also holds 6.2 million shares (around 5,6 per cent) of Star Bulk Carriers Corp. (SBLK), another publicly listed shipping company that operates in the dry bulk sector.

Overall, an interesting business with a diversified portfolio in various segments.

Now, let’s have a look at its financial results, including Q1 2026.

Financials

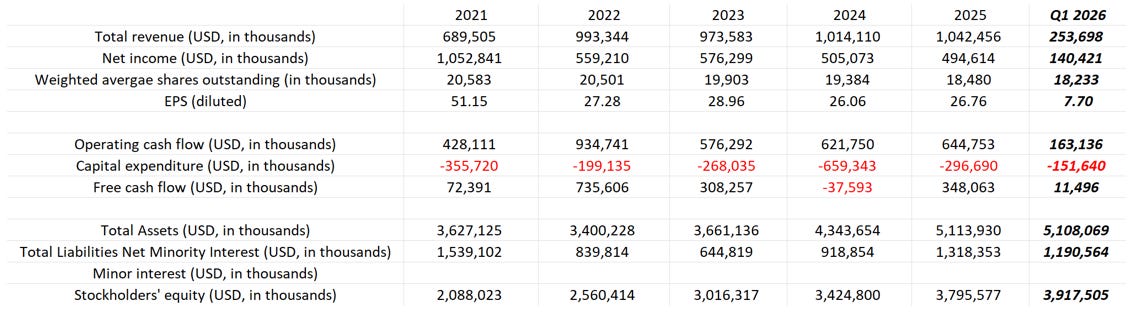

The financial results of Q1 2026 came better than in Q1 2025:

Source: Internal analysis based on DAC reports

The containership segment’s revenue saw a decline by 2.8 per cent or USD 6.6 million (to USD 229.6 million) in Q1 2026 versus USD 236.2 million in Q1 2025. The reason lies in the softer container freight rates. Meanwhile, the dry bulk segment’s revenue increased by 40.9 per cent or USD 7 million (to USD 24.1 million) for the same period versus USD 17.1 million in Q1 2025. In other words, even though the dry bulk carriers occupy a small part of DAC’s fleet, the diversification from solely container ships allowed the company to benefit from the enhanced dry bulk rates.

The company spent in Q1 2026 around USD 152 million on capital expenditures, such as vessel additions and advances for vessels under construction.

Overall, it was a decent Q1 2026 financial result.

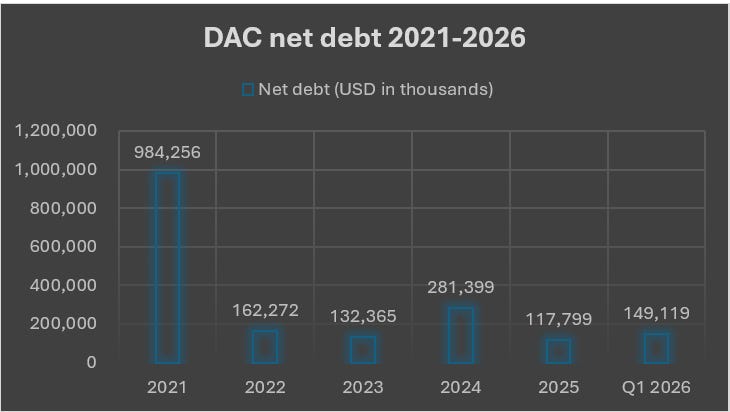

The net debt has been reduced aggressively for the past 5 years:

Source: Internal analysis based on DAC reports

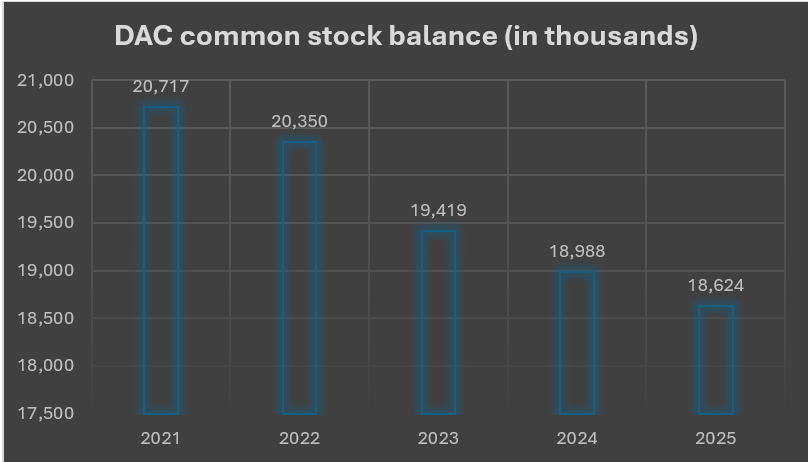

The company’s number of outstanding shares has been going down:

Source: Internal analysis based on DAC reports

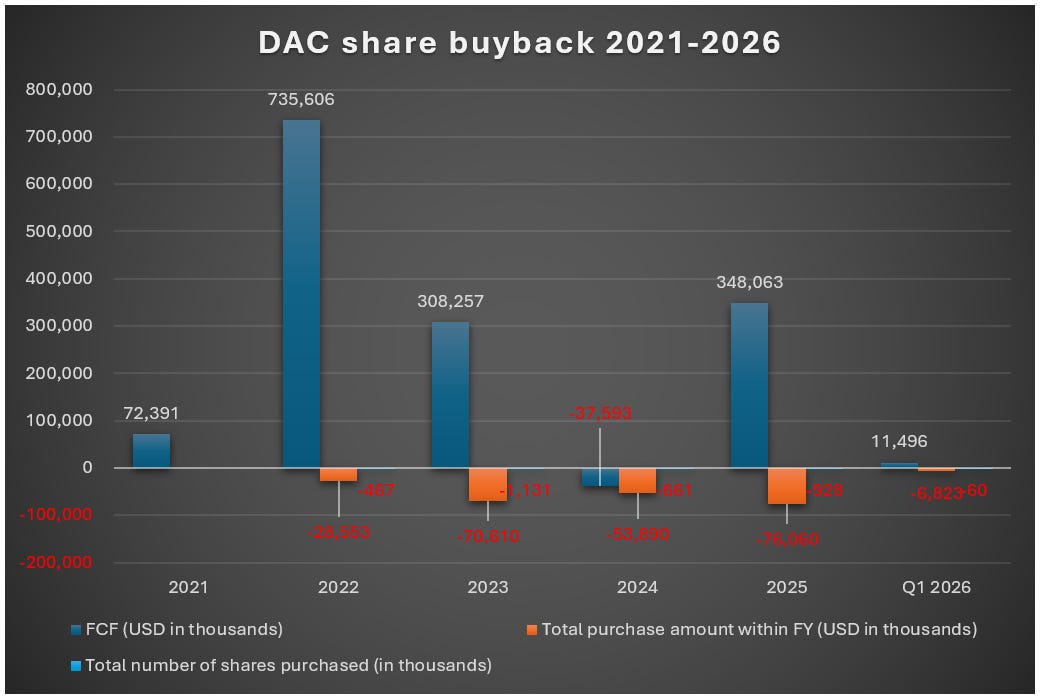

Now, we are getting on very thin ice. The company’s stock price trades at its highest since 2010 and 2022, and they have already repurchased around 3.2 million shares worth USD 235 million since 2022 as of Q1 2026 (cumulative from 2022 to Q1 2026):

Source: Internal analysis based on DAC reports

During the earnings call, DAC management was asked if they would continue applying share buyback programs as the stock trades at high levels, and they said yes, as they think the stock is undervalued. This depends on their NAV calculation per share, inputs and their outlook on the containership segment (please find below our NAV calculation).

In 2025, the company’s Board of Directors approved the increase of the common stock repurchase program from USD 200 million to USD 300 million (3). So, considering the repurchased amount of USD 235 million and the total number of outstanding shares repurchased (3.2 million), the average price paid per share was USD 72.66 for the cumulative period of 2022 until Q1 2026. Now, the following remains open: will they again increase the share buyback program from USD 300 million to a higher number, like USD 500 million?

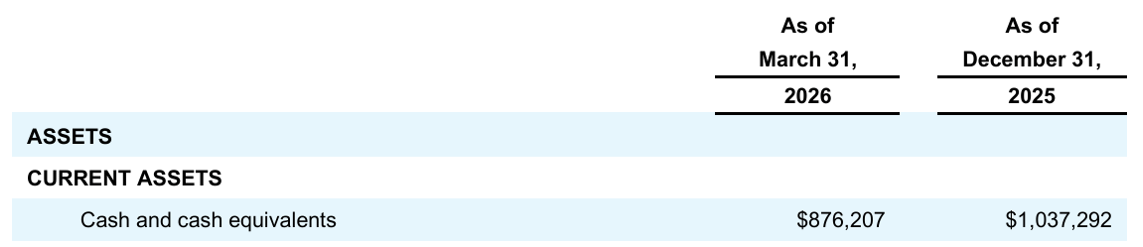

The cash and cash equivalents stand at USD 876 million:

Source: DAC, First Quarter Results for Period Ended March 31, 2026, May 11, 2026

If we add to the above undrawn commitments of USD 248 million, we get around USD 1.3 billion of available liquidity.

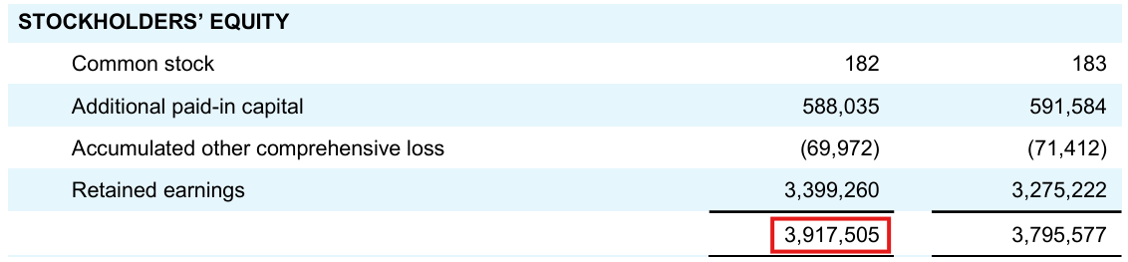

The shareholders’ equity is around USD 4 billion:

Source: DAC, First Quarter Results for Period Ended March 31, 2026, May 11, 2026

DAC is a strong company, a financial fortress, with most of its assets being debt-free. It practices disciplined capital allocation and has reduced the net debt aggressively.

Now, what shall we expect from both segments (container and dry bulk) in 2026 and how to position ourselves?

What to expect in 2026?

Containership segment

Global containership fleet

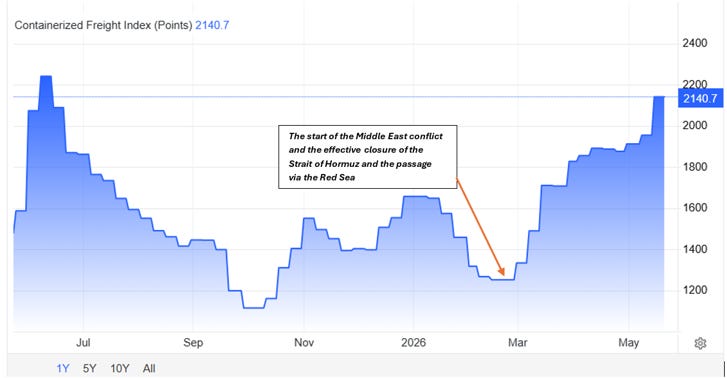

We expect that the new container carriers’ deliveries in 2026 might put pressure on the rates (as we have seen before the start of the Middle East conflict, Q1 2026 financial results and guidance of various container shipping companies, such as A.P. Møller - Mærsk A/S (MAERSK-A.CO)):

Source: Trading Economics

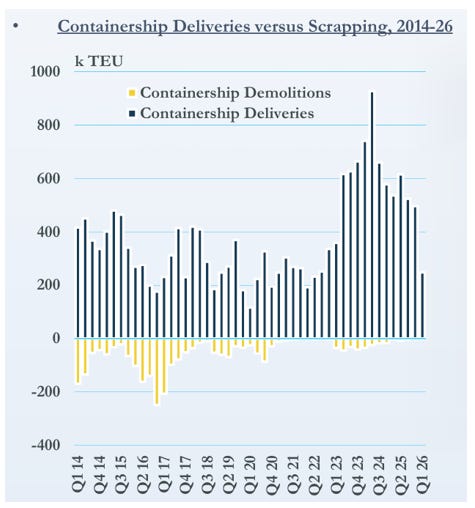

The container carriers that were ordered during the boom periods of 2022-2023 have been delivered since 2024 and onwards, thereby increasing the total global fleet. For example, the overcapacity of container carriers is expected to be around 19 per cent in 2026 and reach an average of 27 per cent in 2028 (4). The current order book is at c. 9.6m TEU, and around 3.3m TEU is slated to be delivered in 2026 (5). Around 248k TEU of vessel equivalent were delivered in Q1 2026 (1).

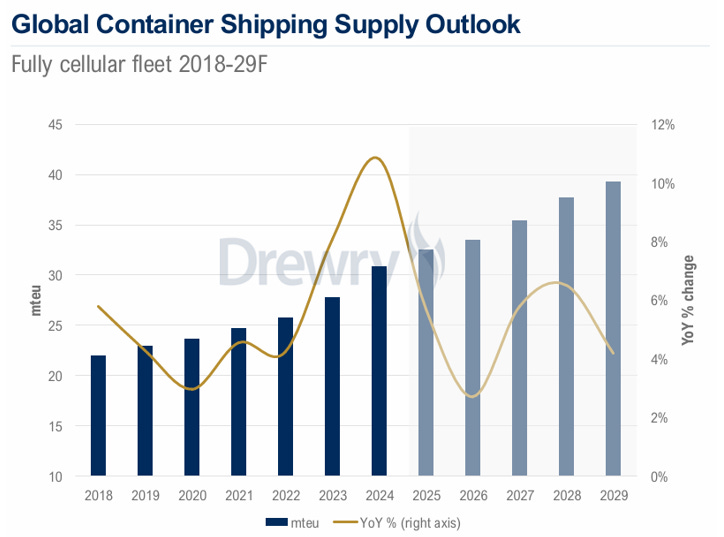

Drewry has the same projection of the global container supply outlook for 2026 (6):

Source: Drewry

Although the supply rate of new container carriers is still lower than in 2024 and 2025.

If we look at the demolition rate of older units, it is at its lowest (around 1k TEU of vessel equivalent):

Despite the delivery of new container carriers, the rates remain elevated as a result of the Middle East conflict, but are expected to stabilise and revert to fundamental factors. As the situation around the resolution of the conflict remains fluid, we shall see how things evolve. However, if truce between the USA and Iran is achieved, apart from the opening of the passage in the Strait of Hormuz, the Suez Canal and the Red Sea passage has a potential to revive, which will put additional pressure on the rates due to the shortened voyage between the ports of loading and discharge (via the Suez Canal – 26 days, via the Cape of Good Hope – 36 days).

However, as per DAC management, the current situation in connection to the passage in the Suez Canal and the Red Sea is unlikely to change:

Source: DAC, Investor Presentation, May 2026

We shall see what the future holds.

World container trade and GDP growth rates

Despite the current situation in the Middle East and elevated energy prices (crude oil, LNG, etc.), the IMF forecasts that GDP growth in 2026 should be around 3.1 per cent (7). This shows how resilient our global economy is.

Now, according to TradeWinds (8), the global container volumes reached an all-time high and made up 192.8 million TEU in 2025. A.P. Møller - Mærsk A/S (9) expects the global container volume in 2026 to grow by 2-4 per cent, which potentially can reach 196.7-200.5 million TEU. But despite the increasing global container volume, most of the containership shipping companies reported weak Q1 2026 results, which stems from the overcapacity due to the supply of new container carriers.

Dry bulk segment

Global dry bulk fleet

We have touched upon the subject of the global dry bulk fleet in previous posts. As DAC has 11 Capesize dry bulk carriers, we shall focus on this segment briefly.

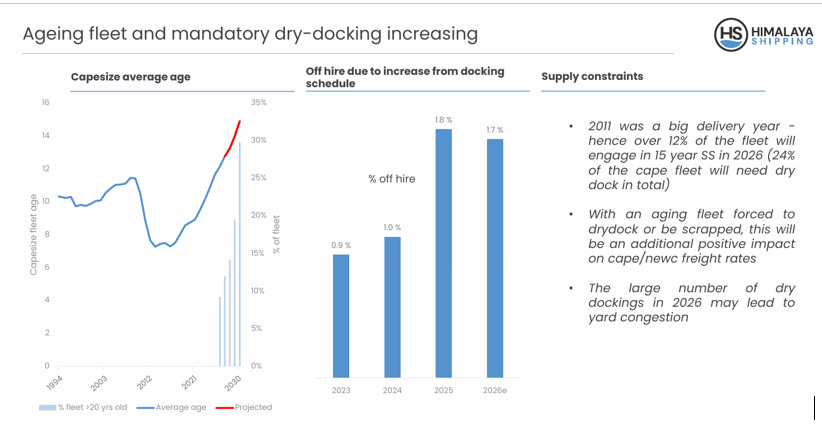

As per DAC (Danaos Corporation, (1) and HSHP (Himalaya Shipping Ltd., (10)), there is a limited supply of new Capesize, and the market has an ageing fleet of Capesize carriers:

Source: HSHP, Q1 2026 Results Presentation, 21 May 2026

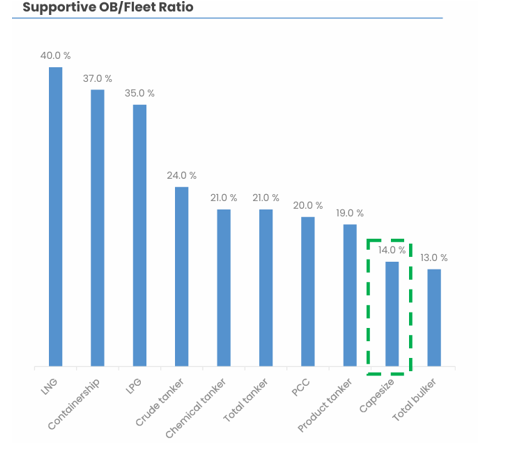

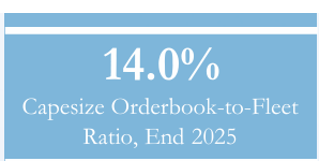

Also, according to DAC (1) and HSHP, the orderbook/fleet ratio as of today stands at 14 per cent:

Source: HSHP, Q1 2026 Results Presentation, 21 May 2026

Source: DAC, Investor Presentation, May 2026

According to Star Bulk Carriers Corp.’s research (11), there is limited shipyard capacity, and the slot will not be available before 2H 2029.

Now let’s have a look at the GDP and demand for dry bulk commodities.

GDP and demand for dry bulk commodities

As we know, the dry bulk shipping companies’ performance is closely correlated with the GDP, global supply and demand for dry bulk commodities.

We already mentioned above that the expected GDP growth is pinned around 3.1 per cent (7), which should be supportive to the dry bulk carriers. It is worth noting that in 2025, the GDP was also 3.1 per cent (12).

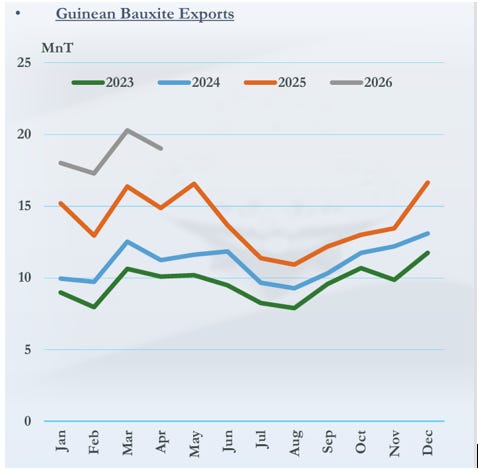

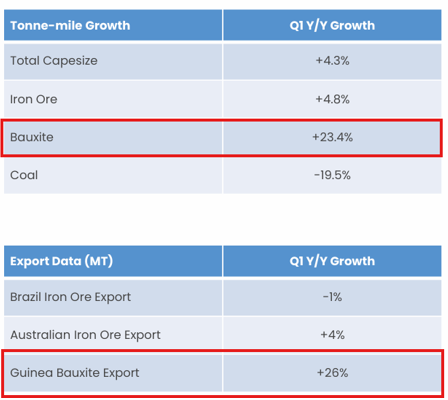

China’s import of iron ore is slated to grow by 2.6 per cent, with 36-38 million tons more compared to 2025 (13). As we mentioned before, the Simandou mine (Guinea, West Africa) has one of the largest bauxite deposits, and its export volume is higher than in previous years, which adds ton/mile to the utilisation of the fleet:

Source: DAC, Investor Presentation, May 2026

Source: HSHP, Q1 2026 Results Presentation, 21 May 2026

Now, by looking at fundamental factors of both containership and dry bulk segments, we get a mixed outlook (weak containership/strong dry bulk). However, as the majority of DAC’s revenue comes from the container ship segment, we shall put more weight on it rather than on the dry bulk segment. But the dry bulk segment can be viewed as a supportive segment for DAC’s overall financial performance.

Risks

If we look at DAC’s business model, most of its cash flow comes from the containership segment. The company has a strong cash flow visibility for 2026 in this segment as it contracted 100 per cent of its fleet operating days (1):

Source: DAC, Investor Presentation, May 2026

Source: DAC, Investor Presentation, May 2026

However, despite the above firming time-charter rates, the fundamental factors laid out in previous sections might have a potential negative impact. We elaborated on the overcapacity in the global container ship fleet and that the growth of global container volume might not be able to absorb the growth of the new deliveries of container carriers. That would be one of the major risks to bear in mind.

Moreover, the elevated energy prices do pose a potential negative impact on the GDP and, hence, on the global containership volume. If GDP growth in major economies such as the US, EU or China slows, container demand might slow too.

Another potential risk is related to the trade wars in the form of imposed tariffs. These types of trade wars can negatively impact the global container volume.

It is important to mull over the above risk factors and make an informed decision.

Stock valuation

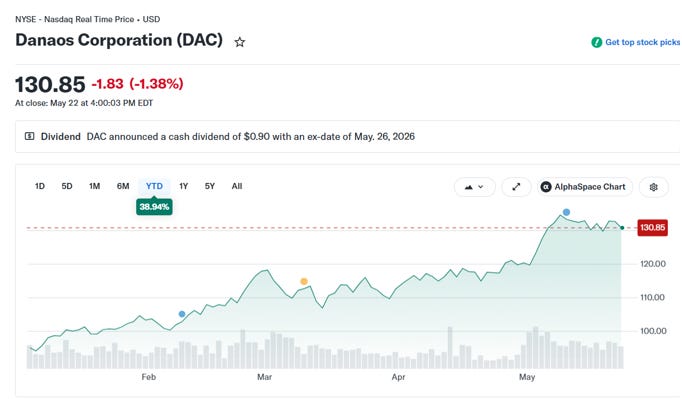

The stock is up 38.94 per cent YTD (as of COB 22 May 2026):

Source: Yahoo Finance

The stock closed on 22 May 2026 at USD 130.85 per share. Now, let’s have a look at the NAV per share:

Source: Internal analysis

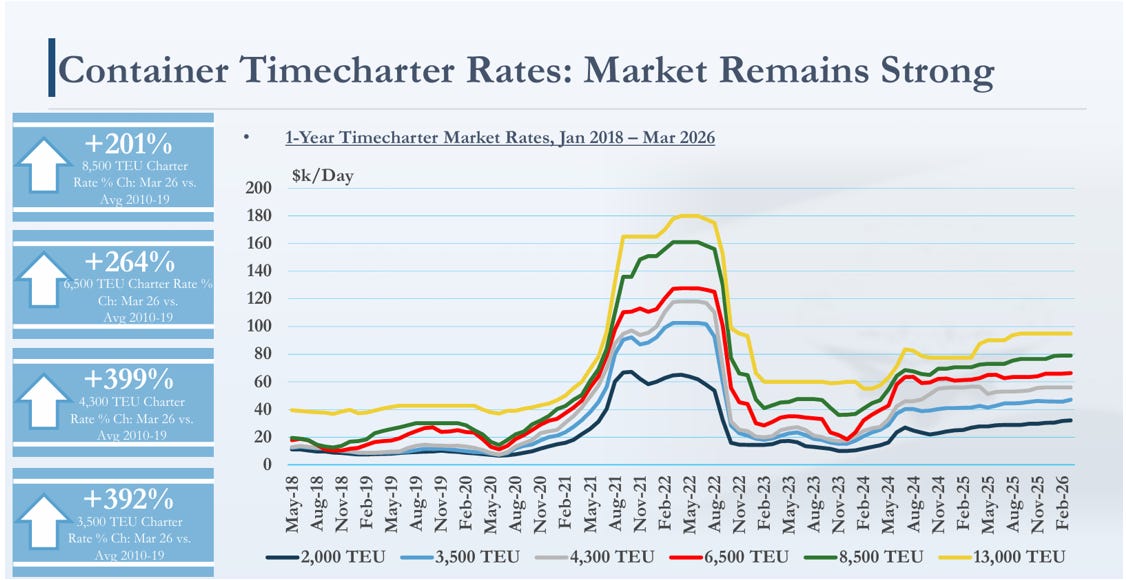

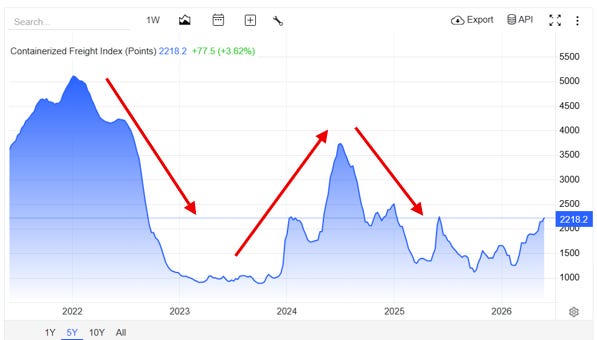

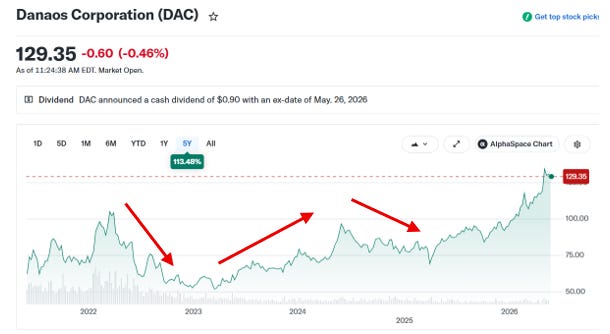

We agree with the DAC’s management that the stock is undervalued compared to its NAV per share. However, there are a few factors that we have to take into consideration. One of them is a bitter one. Even though they have 100 per cent contract coverage of their container fleet’s operating days for 2026 and almost 90 per cent for 2027 (they have visibility into their revenue and are not operating in the spot market), the stock will not be insulated from broader market sentiment. As we have mentioned numerous times, the stock market is a voting machine in the short run and a weighing machine in the long run (B. Graham). As an example of the above statement, please see below the charts of container freight rates and DAC stock price:

Source: Trading Economics

Source: Yahoo Finance

So, although the business model of DAC’s container ship segment has not changed and they have always chartered out their container carriers on multiple-year time charters, the stock price mostly followed the container freight index. The business of DAC is sound at its core, and the cash flow stream has been visible in advance (for example, in 2026 they expect USD 966 million and in 2027 – USD 948 million of revenue), but the sentiment still affected the company’s stock price. Therefore, we have to follow the principle of Warren Buffett: “Price is what you pay; value is what you get”.

Despite the high NAV per share, analysts’ 12-month price target is pinned between USD 140 and USD 157 per share. And depending on the target price, the potential upside from the current level lies between 6 per cent and 20 per cent.

By looking merely at the supply of the new deliveries of the container carriers and their impact on the Q1 2026 financial results of all container shipping companies, we can conclude that the share price might revert from the current elevated levels. Especially, if the resolution around the Strait of Hormuz and the Red Sea passage is found, and the traffic levels revive.

From a value investing perspective, the risk of fundamental factors outweighs the probability of the potential reward.

The guidance from major container shipping companies is negative for 2026 and onwards, and we simply cannot ignore these signs. Even though DAC’s container fleet is covered respectively in 2026 and 2027, the bearish sentiment of the container spot market might influence future investors looking ahead of 2027. Therefore, despite strong financial metrics, the current business will be put in the file called “Watchlist: Low-Risk/High-Reward” because, as of today, the risks outweigh the rewards. And of course, we have to apply the margin of safety.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, don’t hesitate to get in touch with me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Please find us on: https://valueinvestinginshipping@substack.com

Sources:

1 DAC, Investor Presentation, May 2026

2 Danaos Corporation (DAC), Q1 FY2026 earnings call, May 12, 2026

3 DAC, Form 20-F, 2025

4 https://logicall.com/blog/new-vessel-deliveries-reshape-container-shipping/

5 https://seagatelogistics.org/news/key-trends-of-container-transportation-shaping-2026/

6 Drewry, Container Market Outlook 2026

7 IMF, Global Economy in the Shadow of War, Apr 2026

9 A.P. Møller - Mærsk A/S, Q1 2026 Results Presentation, May 7, 2026

10 HSHP, Q1 2026 Results Presentation, 21 May 2026

11 Star Bulk Carriers Corp., Corporate Presentation, Mar 2026

12 IMF, Real GDP growth, Mar 2026

13 https://skillings.net/chinas-iron-ore-appetite-imports-hit-record-1-26-billion-tons-in-2025/