Deep Dive: DHT Holdings Inc. (ticker symbol: DHT)

(published on Substack on 17 Feb 2026)

Business overview

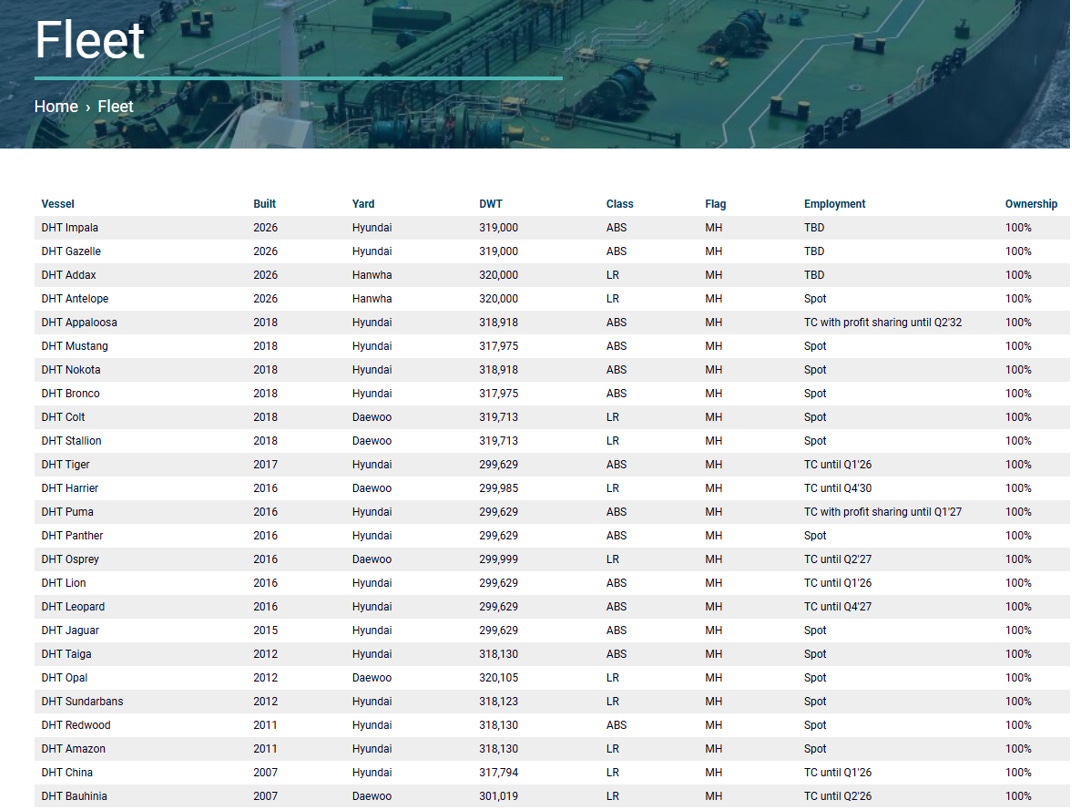

DHT Holdings Inc. owns 26 tankers (VLCC – Very Large Crude Carrier (around 200,000-320,000 metric tons)) and operates worldwide. They transport crude oil from the port of loading to the port of discharge and are paid for this service. The average age of their vessels is 2016 (i.e. the vessels are 10 years old, which is one of the youngest fleets).

Market capitalisation is around 2.48B with a P/E ratio of 11.77.

The company’s 9 vessels are on Time-Charter (i.e. relet to a company for a period of time for employment), and the rest are being traded on spot (i.e. they have to find a company that will hire their vessels):

Source: DHT Holdings Inc., Annual Report 2025

On a side note, the company owns 100 per cent of all their vessels.

Financials

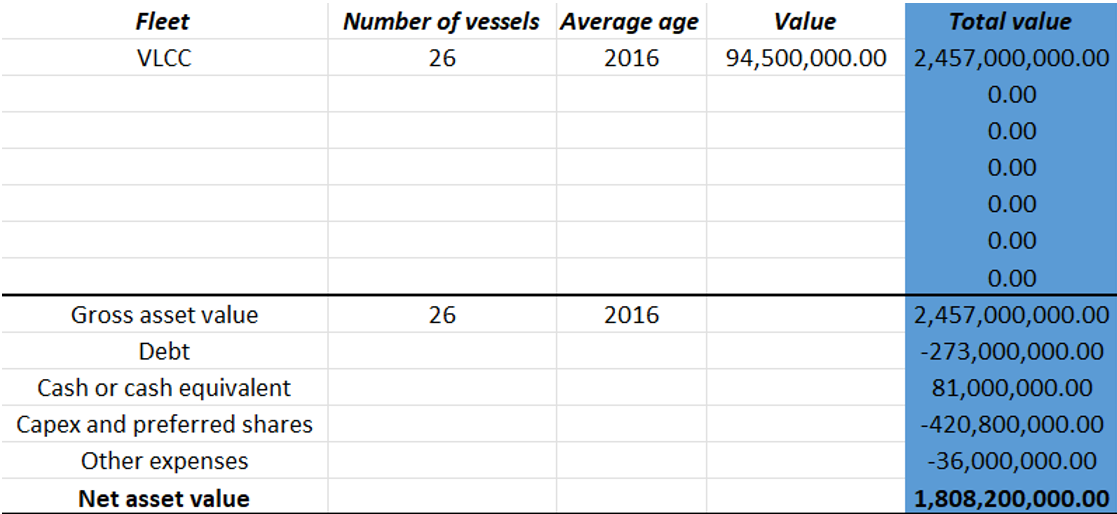

As mentioned, their fleet consists of 26 VLCC vessels, and we shall consider those as assets, as any shipping company can sell any of the vessels to cover expenses:

Source: Internal analysis

I put the average value per vessel of the fleet at USD 94.5M, and after deducting debts and expenses, we get a Net Asset Value of USD 1.81B. I do strongly believe that the company is financially very healthy.

Revenues and net income are also healthy (2020 and 2021 were terrible for the tanker sector due to reduced demand and low volume of transported crude oil):

Source: Yahoo Finance

FCF became positive after 2021:

Source: Yahoo Finance

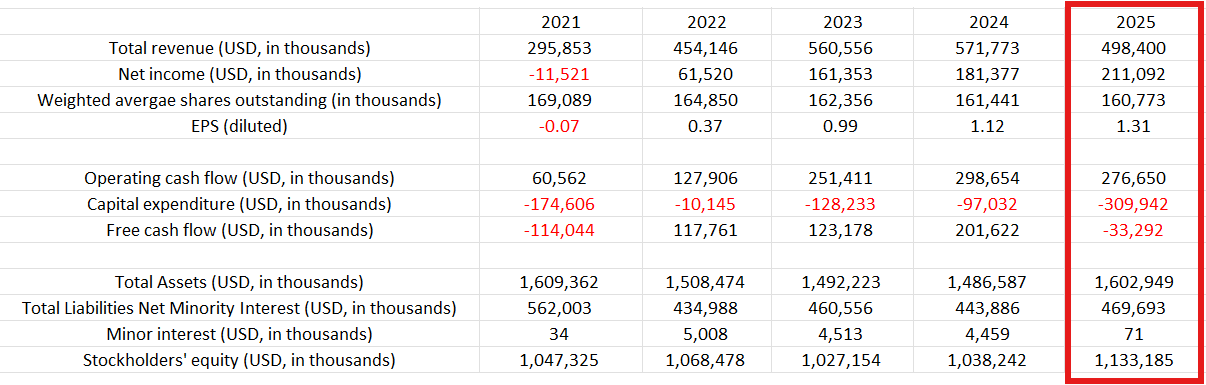

Below are my personal records of the financials, including the updated FY2025:

Source: Internal analysis based on DHT reports

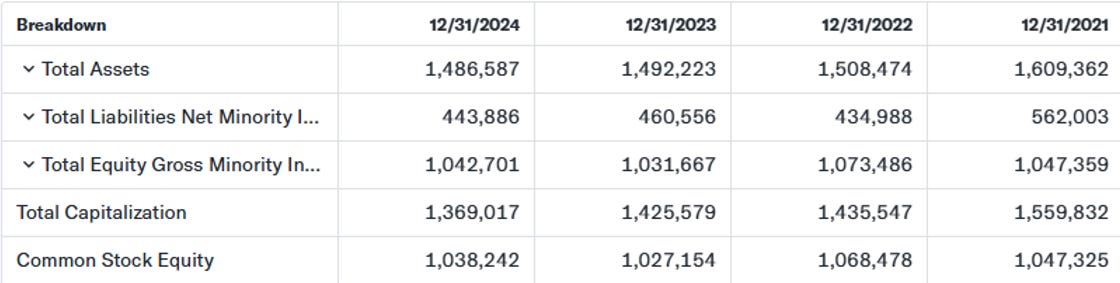

The balance sheet is strong:

Source: Yahoo Finance

As per my calculations, for 2025, they have 1.133B of stockholders’ equity. Very solid.

According to the company, the 4Q2025 was healthy:

Source: DHT Holdings Inc., Fourth Quarter 2025 Results

They are positive about the outlook for 2026:

Source: DHT Holdings Inc., Fourth Quarter 2025 Results

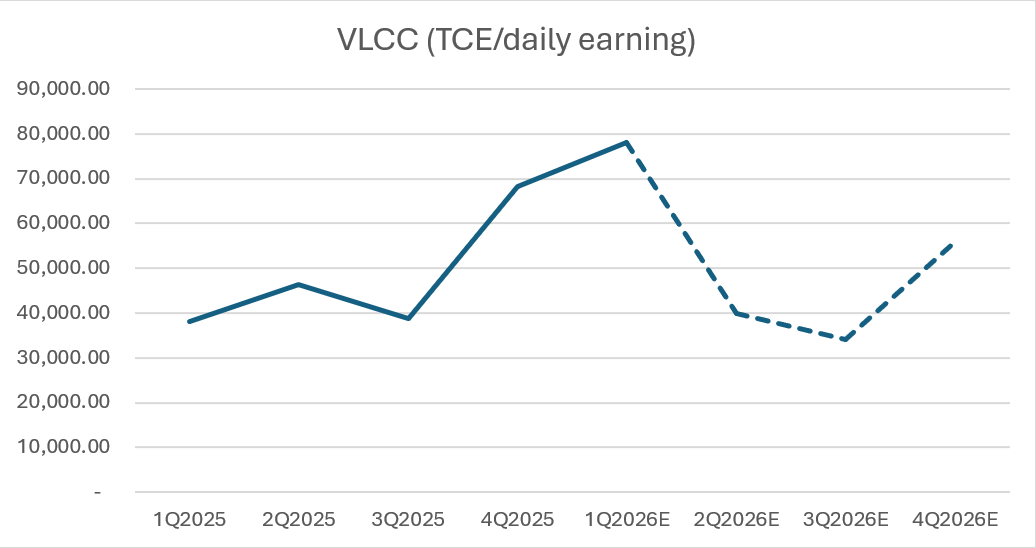

They described the positive outlook based on healthy crude oil demand, its transportation and ageing fleet. The same points that I laid out in my previous post, dated 13 Feb 2026 (Outlook on tankers market in 2026). In the same post, I projected that the average VLCC daily earnings/TCE in 2026 should potentially be USD 52,000, which is higher than in 2025 (average USD 47,833 per day):

Source: Internal analysis

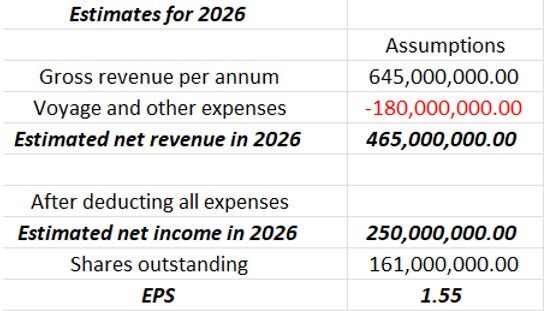

Based on the above projected daily earnings/TCE for 2026, we get approximately EPS of USD 1.55 per share:

Source: Internal analysis

In 2025, the EPS was around USD 1.31 per share. The above projections for revenue and net income will also lead to a positive FCF.

As of 31 December 2025, the company has USD 79,000,000 of cash and cash equivalents:

Source: DHT Holdings Inc., Fourth Quarter 2025 Results

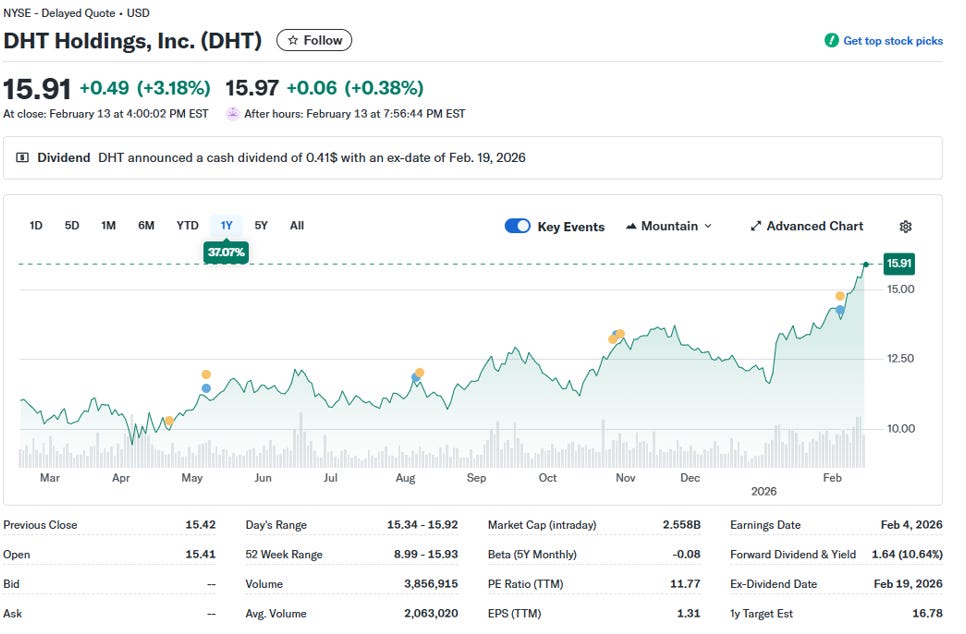

Stock valuation: Is DHT overpriced or is it fairly priced?

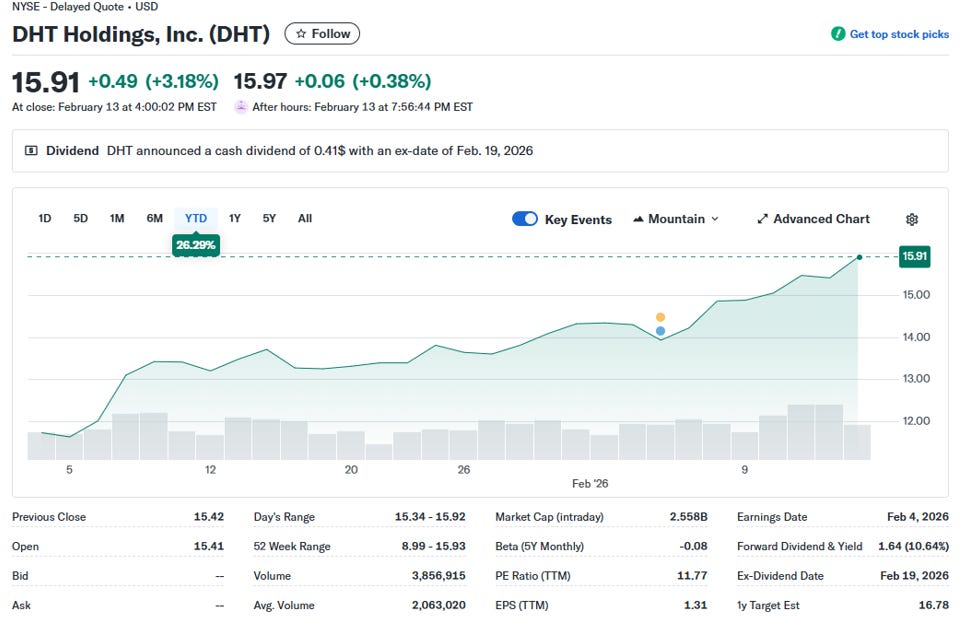

Source: Yahoo Finance

Looking at the YTD and 1-year chart of the stock and comparing it with the projections of TCE mentioned above, I have a strong view that the stock is overpriced.

If we buy today at the price of USD 15.91 per share, strongly convinced that the price can go up to USD 20 per share (which it might), but due to seasonality and cyclicality, the stock drops initially to USD 11.00 per share, we risk facing a twofold loss:

a) the Margin of Safety or MoS (a crucial rule in the world of cyclical stocks); and b) Opportunity Cost.

The first rule is a vital one, as it allows us to err a bit and gives us a bit of a cushion. As W. Buffett indicated in one of his letters, he would rather be vaguely right than precisely wrong. But the original quote comes from John Maynard Keynes (the economist): It is better to be roughly correct than to be precise.

The MoS will allow us to avoid the possibility of being wrong precisely as we want a sound investment which has low risk/high reward, not a bet.

The second issue is related to the opportunity cost. Namely, if our invested capital is stuck in an investment that was bought basis FOMO or without any thorough analysis, we face an issue of bad deployment of the capital. And we, being the CEOs of our investments, shall invest our capital wherever the ROI is the best for us. I do not suggest chasing the returns at any cost. That would be reckless. Hence, after thorough analysis of sound companies, we make an investment based on the best ROI. Our major task is to preserve our capital and invest in low-risk/high-reward investments.

As of now, the stock of DHT is at its highest point since the past 5 years, and it seems overvalued. Based on my estimations of TCE for 2026, the stock should adjust according to its fundamental factors. For now, we shall wait for the right price, which offers us, value investors, low risk/high rewards.

It is worth noting that we also have to consider the factor of risk, which entails macro-factors, lower demand for crude oil and of course a recession.

But as I mentioned before, it is up to you, my fellow value investors, how the position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com