Deep Dive: Diana Shipping Inc.(ticker symbol: DSX)

(published on Substack on 20 Feb 2026)

Business overview

Diana Shipping Inc. is a publicly listed company engaged in the global transportation of dry bulk commodities. They own dry bulk carriers and make a profit by leasing them to commodity traders, miners and industrial customers.

Source: Diana Shipping Inc.

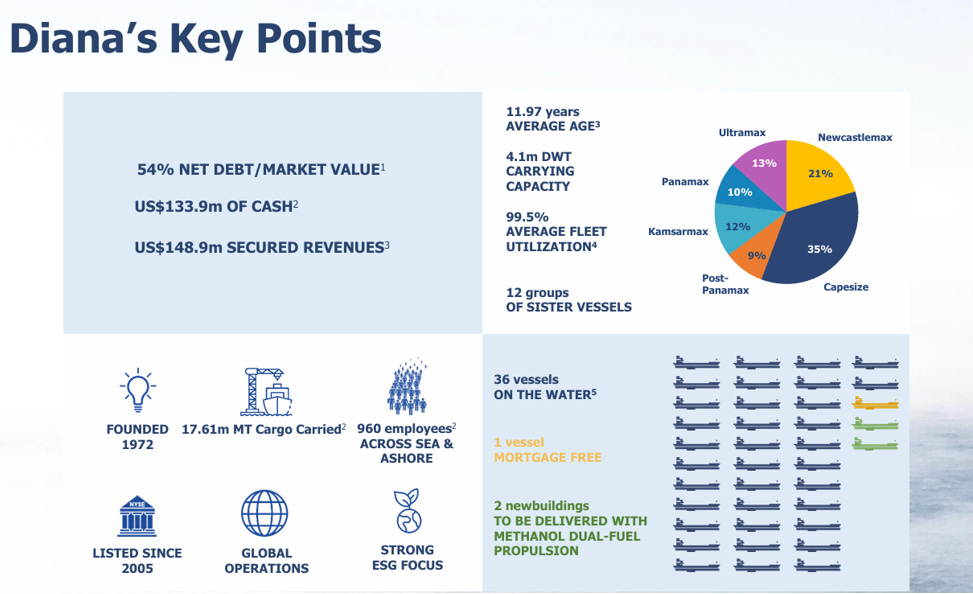

Diana Shipping owns 36 vessels ranging from Ultramax (50,000-65,000 mt) to Newcastlemax (200,000-220,000 mt) carriers, which are 12 years old on average:

Source: Diana Shipping Inc., Financial Results for the 4th Quarter of 2025, 26 February 2026

Financials

The market capitalisation is USD 285m, and the PE ratio is at 16.40.

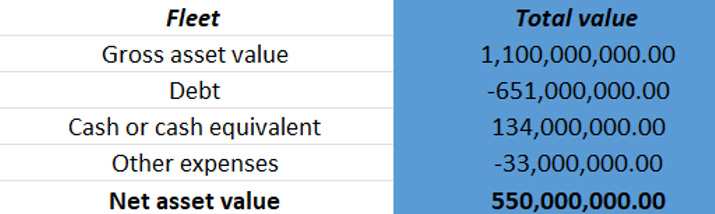

The company’s Net Asset Value stands at USD 550m:

Source: Internal analysis

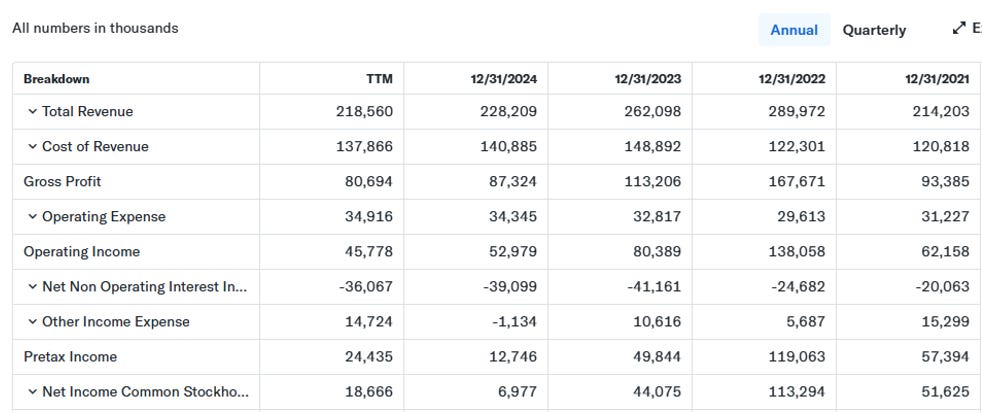

Revenue and net income are positive:

Source: Yahoo Finance

Source: Internal analysis based on DSX reports

For nine months in 2025, the company made around USD 161m in revenue and USD 15m in net income. For final numbers for FY2025, I estimate the revenue and net income to be around USD 215-217m and USD 9-11m, respectively.

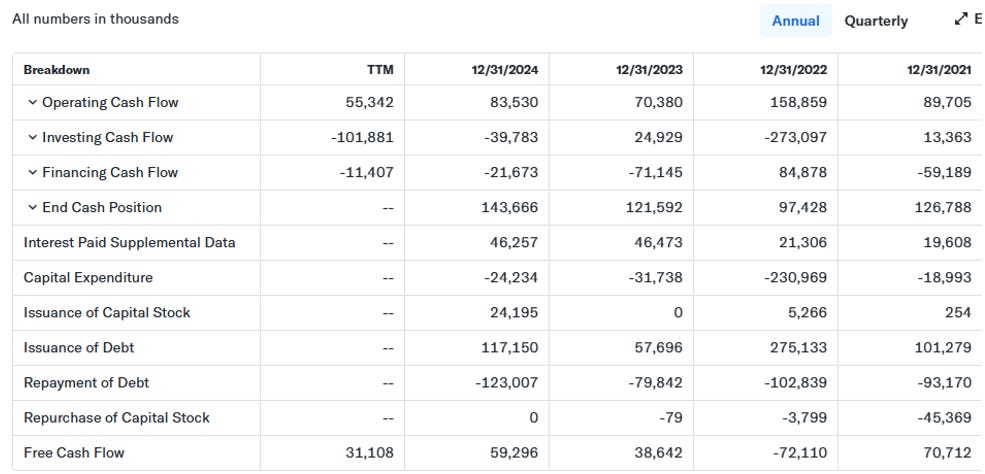

FCF has been positive except in 2022, when they allocated around USD 230m to acquire vessels:

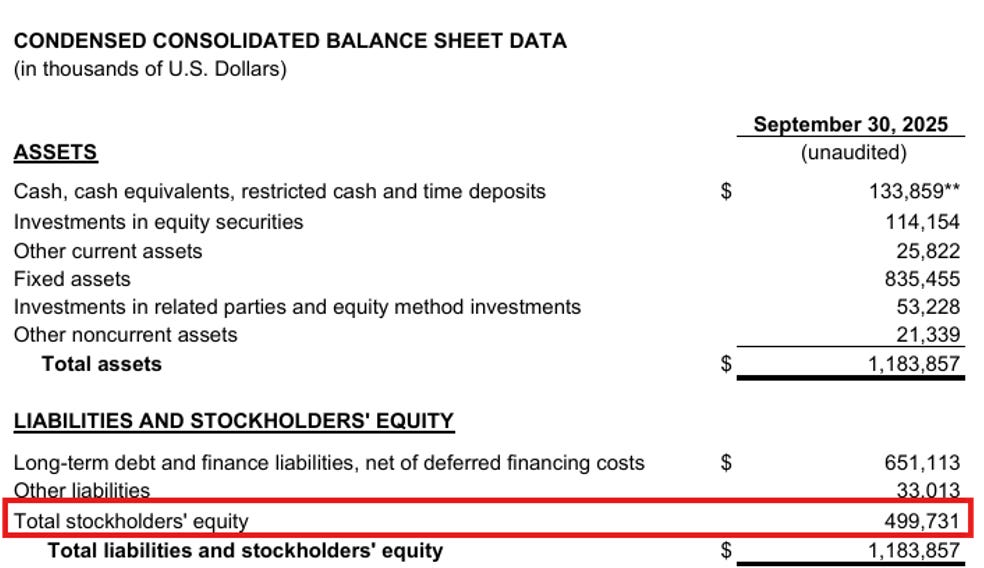

If I look at stockholders’ equity, it stands at USD 500m (as of Sep 2025):

Source: Diana Shipping Inc., Financial Results for the 3rd Quarter of 2025

So, the company is healthy and has cash and deposits of USD 134m, which is good.

Risks

As with any commodity-related industry, the company is dependent on the demand for transporting dry bulk commodities. The demand can be negatively affected by tariff wars, recession or any other factor that can undermine the demand, especially geopolitics.

But all else being equal, the factors mentioned in my dry bulk outlook for 2026 should be positive for companies with a dry bulk fleet (for more details, please read my post dated 06 Feb 2026). Here are a few reminders:

· A higher export volume of iron ore from Brazil and Guinea, and bauxite from Guinea;

· Low delivery of dry bulk carriers due to underinvestment; and

· Ageing fleet of current bulk carriers.

Stock valuation: is it undervalued or fairly priced?

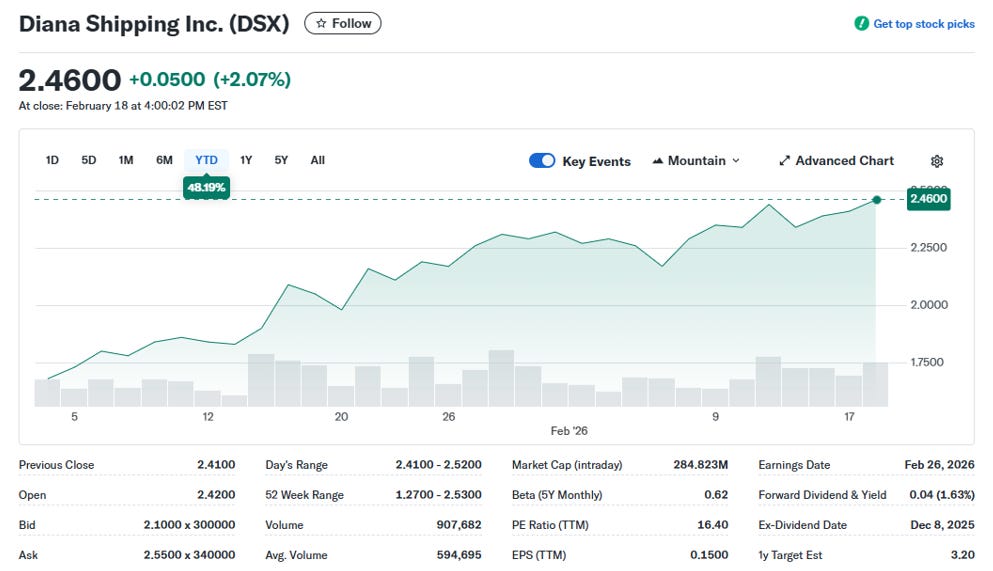

Source: Yahoo Finance

The stock is up 48 per cent YTD, which underpins my thesis that the dry bulk shipping sector and its players should benefit from the fundamental factors mentioned above, and in my post dated 06 Feb 2026.

Source: Diana Shipping Inc.

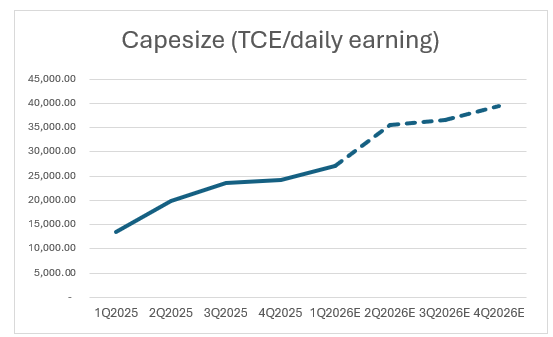

The stock is going up and down with the dry bulk shipping cycle and offers, at times, very interesting opportunities. The company has 8 Capesize and 4 Newcastlemax vessels, which should benefit from the positive trend.

The 4Q2025 (to be reported on 26 Feb 2026) and 1Q2026 have not been posted yet, but with the average daily earnings/TCE in 2026 being estimated at USD 34,625 for the Capesize segment, I do believe the current price of the stock seems undervalued:

Source: Internal analysis

Namely, as per my calculations, the company’s revenue and net income shall go up due to daily earnings/TCE. After modelling the above and other dry bulk segments of vessels, I estimate that the revenue should be around USD 280-285m and net income should reach USD 59-62m (meaning EPS can potentially be USD 0.53-0.56). Now, in this case, the FCF shall be higher than in 2025, due to the positive metrics mentioned above, I reckon USD 90-95m, but we shall see if they invest in fixed assets. The reports for 4Q2025 and 1Q2026 shall shed some light on their outlook.

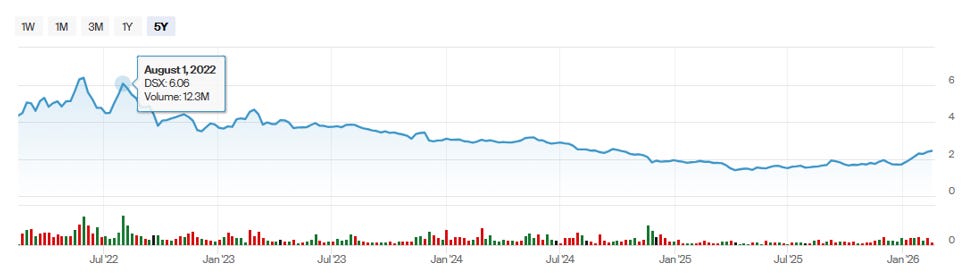

If you look at the YTD chart of the stock price, you can see that the price is already adjusting to the 1Q2026 trend, which is in line with the above daily earnings/TCE projections.

As mentioned in one of my prior posts, despite applying a value investing approach to the shipping industry and analysing the stocks based on a bottom-up viewpoint, we shall not hold the purchased stock forever. Even Warren Buffett sold 9 out of 10 purchased stocks. But taking into account the cyclicality of the shipping industry, we, as value investors, have to be extra careful not to invest in stocks with high risk/low reward. We prefer low-risk/high-reward options, which the subject stock still offers due to the factors laid out above and in one of my previous posts.

But as I mentioned before, it is up to you, my fellow value investors, how the position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com