Deep Dive: FLEX LNG (ticker symbol: FLNG)

(published on Substack on 17 Mar 2026)

Business overview

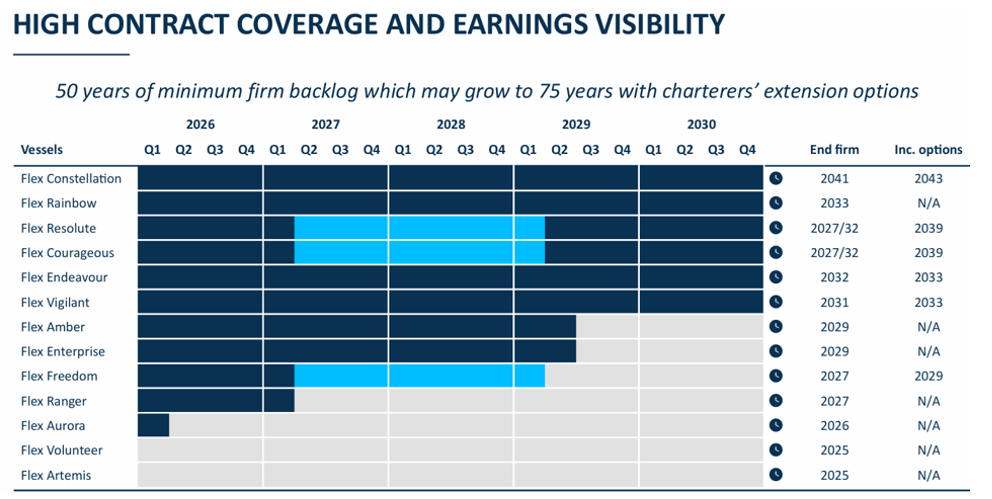

The company owns and manages 13 LNG carriers, most of which are scheduled on time-charter conditions for several years:

Source: FLEX LNG, DNB Carnegie's Energy & Shipping Conference, March 2026

The average age of the fleet is 6.3 years, and all thirteen vessels’ capacity is 173,400-174,000m3.

The company became publicly listed in 2019 and is traded on the NYSE under the ticker symbol FLNG.

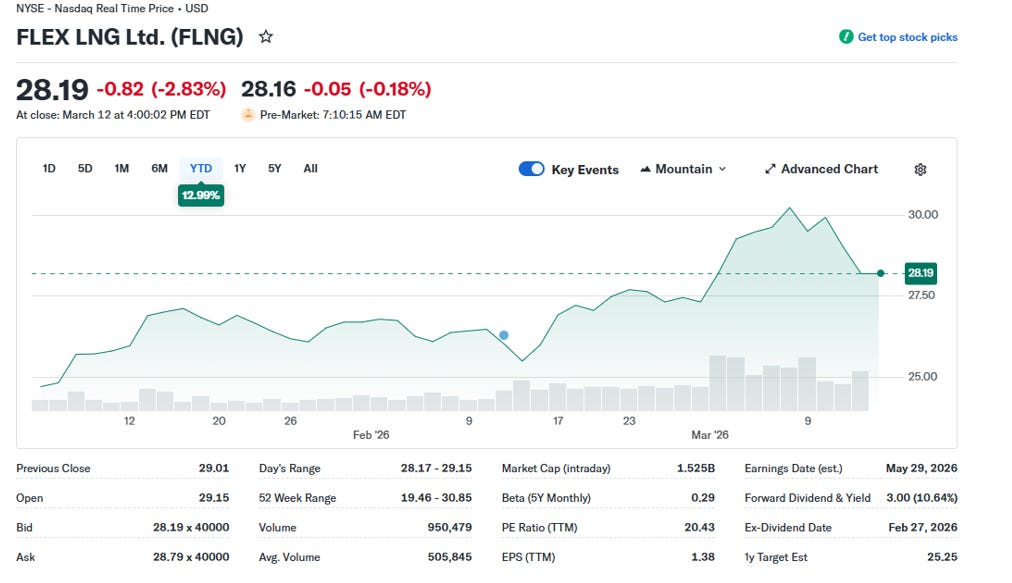

The company’s market capitalisation is 1.525B, and the P/E ratio is 20.43 (cheaper than the S&P 500, with the current P/E ratio being at 28.67):

Source: Yahoo Finance

The company’s business is purely related to the marine transportation of LNG.

Financials

Now, let’s have a look at their finances:

Source: Internal analysis based on FLNG reports

Now, looking at the revenue, it has been in line with previous years, but the net income has dropped. The reason for the drop lies in the losses on derivative instruments (loss of USD 7.4 million), increased LNG carriers’ operating expenses (by USD 4.9 million compared to 2024), and increased voyage expenses (by USD 9 million compared to 2024). Stockholders’ equity is at USD 719 million.

If we look at FCF, the company has USD 141 million and has no capital expenditure.

The company has nearly USD 448 million in cash and cash equivalents:

Source: FLEX LNG, Annual Report 2025

Financially, the company looks very strong, and the USD 448 million cash and cash equivalents are a good sign.

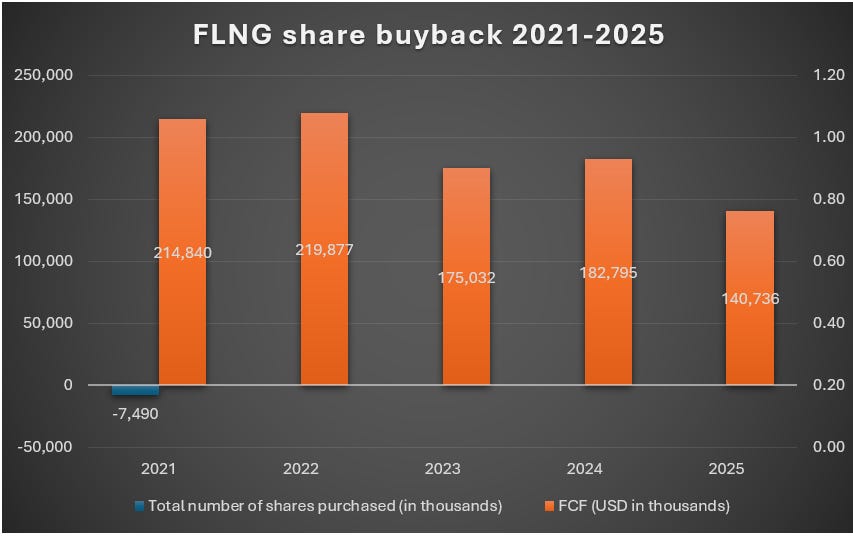

The company has not made any share buy-backs since 2021 and returned dividend payouts to its shareholders instead:

Source: Internal analysis based on FLNG reports

According to FLEX LNG’s presentation, it has returned approximately USD 850 million since the listing, yielding a total shareholder return of c. 390 per cent (1).

According to management (2), the longer distances (i.e., the avoidance of the Suez and Panama Canals) and colder winter in Europe in 2025 did not help LNG carrier rates firm, thereby affecting the company’s revenue and net income. The underlying reason for the aforementioned lies in the high number of new LNG carriers delivered in 2025. According to FLEX LNG, 60 vessels were delivered in 2025, thereby affecting the rates of LNG carriers. It is worth noting that the average rate declined from USD 54,000 per day in 2024 to USD 37,000 per day in 2025. The expansion of new LNG export facilities did not absorb the growth in the delivery of new LNG carriers.

What to expect in 2026?

As per my previous post, “Outlook on LNG sector in 2026” dated 13.03.2026, the LNG export infrastructure is slated to expand and add 56-58 million tons per annum in 2026. But, with Qatari supplies being out (around 77 million tons per annum), we have to see if the addition of North Field East (32 mtpa) and North Field South (16 mtpa) will take place. Demand is also projected to increase, with Asia and Europe being the drivers. The demand in 2026 in Asia and Europe should increase by 10 per cent and 5 per cent, respectively, compared with 2025 (3).

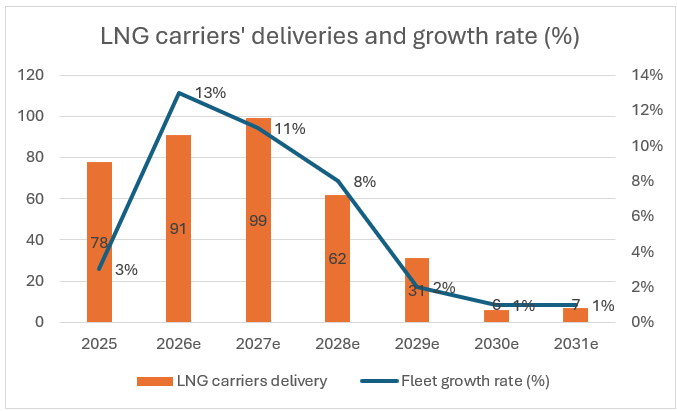

On the other hand, we have 91 vessels scheduled to be delivered in 2026, which should pose risks to spot rates of LNG carriers:

Source: Internal analysis

The same guidance has been communicated by the CEO of FLEX LNG, Marius Foss (4). Their 2026 guidance is softer compared to 2025.

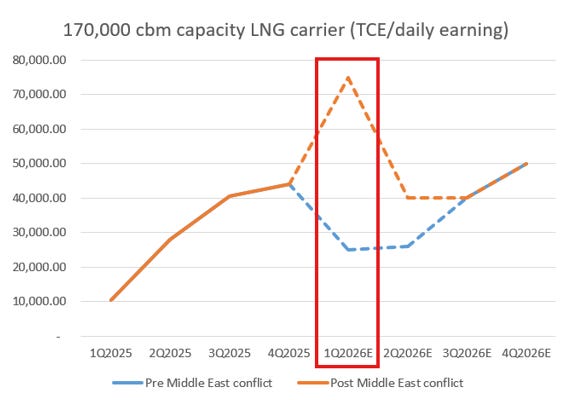

However, the Middle East conflict and the closure of the Strait of Hormuz pushed the daily earnings/TCE from USD 33,500 per day on Mar 4, 2026, to USD 227,500 per day on Mar 5, 2026:

Source: Internal analysis

Thereby pushing the provisional 1Q2026 daily earnings/TCE from USD 25,000 per day (pre-conflict) to USD 75,000 per day (post-conflict). As you can see from the above, the whole 2026 curve changed. Namely, the pre-conflict rates assumed daily earnings/TCE were estimated at USD 35,000-35,250 per day versus post-conflict rates, which are projected at USD 51,000-51,250 per day. However, it is worth noting that last week, the daily earnings/TCE have softened a bit to USD 187,500 per day.

Let’s have a look at risks.

Risks

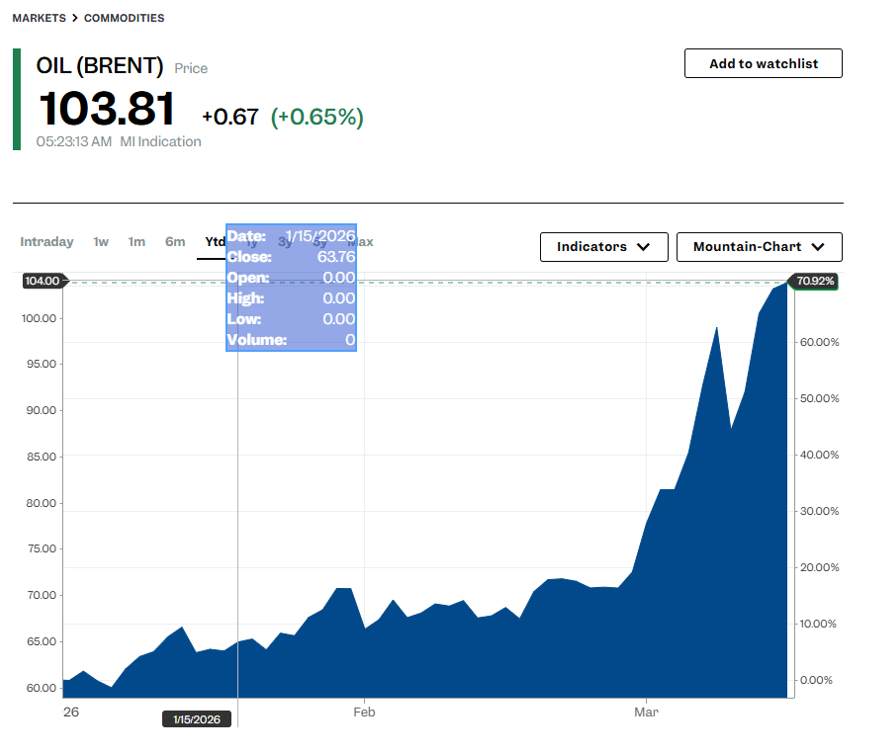

The major risk that stands out is the prolonged conflict in the Middle East and the closure of the Strait of Hormuz. This pushes the price of commodities, such as crude oil prices, LNG and LPG. At the time of writing, the crude oil benchmark was at USD 103.81 per barrel:

Source: Business Insider

The Dutch TTF (Title Transfer Facility) was at USD 51.995:

Source: Investing.com

The above high prices are posing a huge risk to the global economy, with the potential of a recession, especially in Asia and Europe, as these two regions are the most vulnerable to the energy price volatility.

Another risk is related to the delivery of the new LNG carriers in 2026 and the potential impact on the rates. This trend has already been impacting the rates starting from 2025, and as per my analysis, it should continue to affect the rates in 2026, as the growth rate of the new deliveries of LNG carriers will not be absorbed by the growth rate of the expansion of LNG export facilities.

The third risk is related to the outage of LNG production, which already has a huge impact on LNG carrier rates. There is additional risk related to their expansion of the mentioned above fields, and the plans can be delayed.

We shall see how the events unfold. But as mentioned before, the answer lies in the duration of this conflict and its overall impact.

Is FLEX LNG stock overvalued now?

Let’s have a look at the YTD chart:

Source: FLEX LNG

As you can see, the stock price reflects the current situation in the Middle East and is still elevated. Now, if we look at the 2024-2026 period, we can see that the deliveries of new LNG carriers did indeed affect the daily earnings/TCE rates, which were reflected in the company’s stock price:

By looking at the fundamental factors such as additions to LNG export infrastructure, the current outage of LNG facilities in Qatar, the delivery number of new LNG carriers in 2026 and the current stock price, I do believe that the stock offers a high-risk/low-reward option (we have better options as of today). Namely, as of now, the risks outweigh the rewards in terms of returns if we intend to invest.

But, it’s worth mentioning that if the situation arises where the war in the Middle East resolves and/or the Strait of Hormuz opens, there might be a short-term spike as LNG-importing countries will ramp up their depleted volumes (including LPG and crude oil volumes). And this might be beneficial for the FLEX LNG stock price (or for tanker and LPG publicly listed companies). But from a value-investing perspective, it would be more of a bet rather than a bottom-up approach.

From a value investing point of view, the stock is on the waiting list for a low-risk/high-reward offer.

But as I mentioned before, it is up to you, my fellow value investors, to decide how the position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 https://mb.cision.com/Main/22886/4317408/3967954.pdf

2 https://mb.cision.com/Main/22886/4314357/3957116.pdf

3 https://adi-analytics.com/2026/01/13/2026-adi-global-natural-gas-lng-outlook/