Deep Dive: Frontline plc (ticker symbols: FRO and FRO.OL)

(published on Substack on 24 Mar 2026)

Business overview

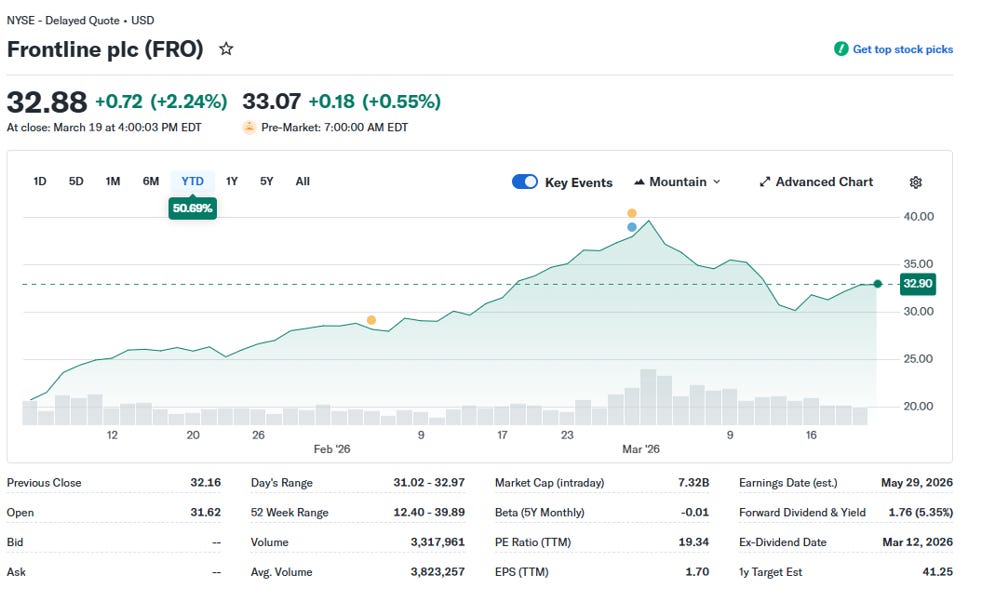

The company’s market capitalisation is USD 7.32 billion with a P/E ratio of 19.34:

Source: Yahoo Finance

The company’s stock is traded both on the New York Stock Exchange (“NYSE”) and the Oslo Stock Exchange (“OSE”).

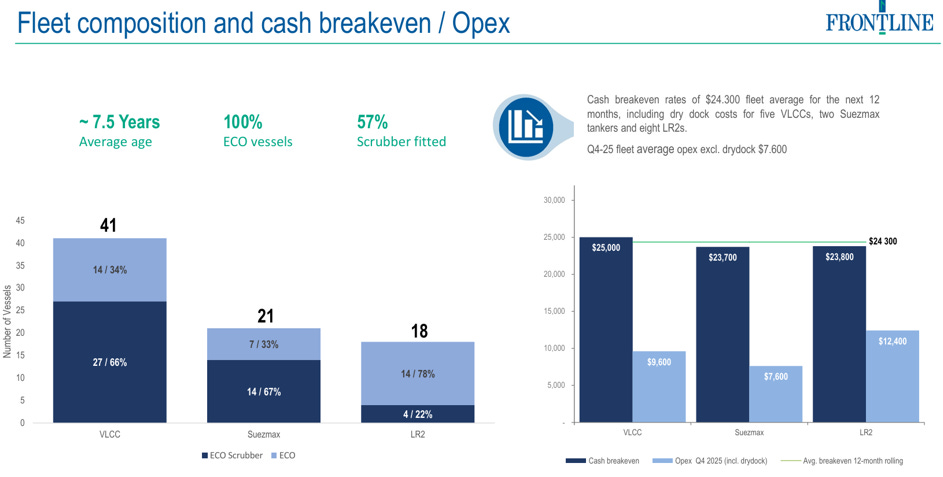

Frontline plc’s business is solely concentrated in the tanker sector of the shipping industry, and it is engaged in the transportation of crude oil or petroleum products globally. The company has 41 VLCCs (Very Large Crude Carrier, with a deadweight of 200,000+ mt) with an average age of 6 years, 21 Suezmax (with a deadweight of 121,000-199,000 mt) with an average age of 8 years and 18 Aframax/LR2 (with a deadweight of 80,000-120,000 mt) with an average age of 8 years.

As a side note, Aframax and LR2 (Long Range 2) have the same deadweight but are different in terms of their employment. Aframax are used mostly for transporting crude oil or dirty petroleum products, such as fuel oil. Whereas LR2s are mostly used to transport clean petroleum products, such as diesel, jet or gasoline, etc. But both types of vessels are interchangeable, namely, after certain cleaning procedures, Aframax vessels can transport clean petroleum products, and LR2 can transport crude oil or dirty petroleum products.

The average age of their fleet is around 7.5 years:

Source: Frontline plc

Now, looking at the fleet, we can see that it is very young and hence, capital expenditures should remain low, thereby enhancing the FCF (we shall analyse financial aspects below).

The company operates globally and has a diversified tanker fleet portfolio, unlike the company DHT, whose fleet portfolio is concentrated solely in VLCC tankers (For the DHT analysis, please read the post “Deep Dive: DHT Holdings Inc (DHT)” dated 17 Feb 2026).

They recently announced the sale of 8 VLCCs that were built between 2015 and 2016 and the acquisition of 9 new VLCCs (2).

Let’s have a look at how they are doing financially.

Financials

The company has been doing quite well since 2021:

Source: Internal analysis based on FRO annual reports

The net income loss in 2021 is attributable to the COVID-19 pandemic, during which time the tanker industry experienced great losses due to the low global oil demand. They have not been conducting share buybacks but have instead been issuing additional shares to renew their fleet. It is evident in the capital expenditure section of the cash flows.

The stockholders’ equity is USD 2.5 billion, which is favourable.

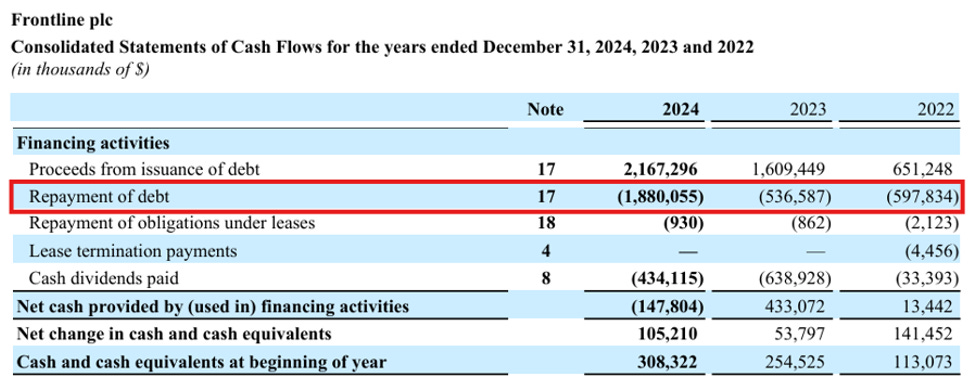

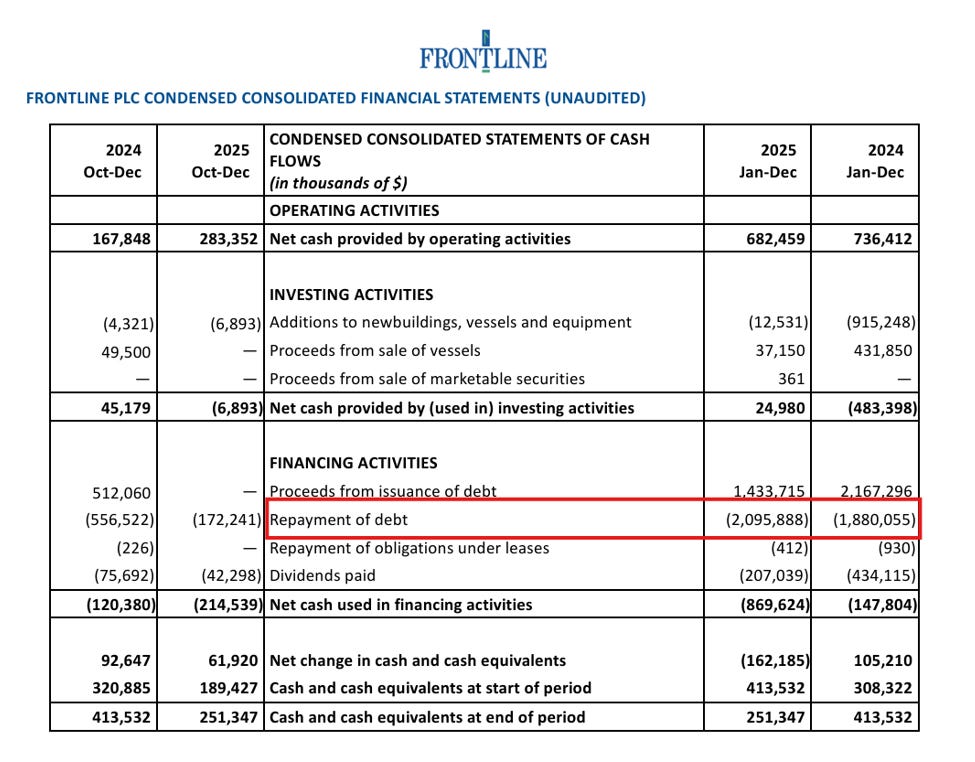

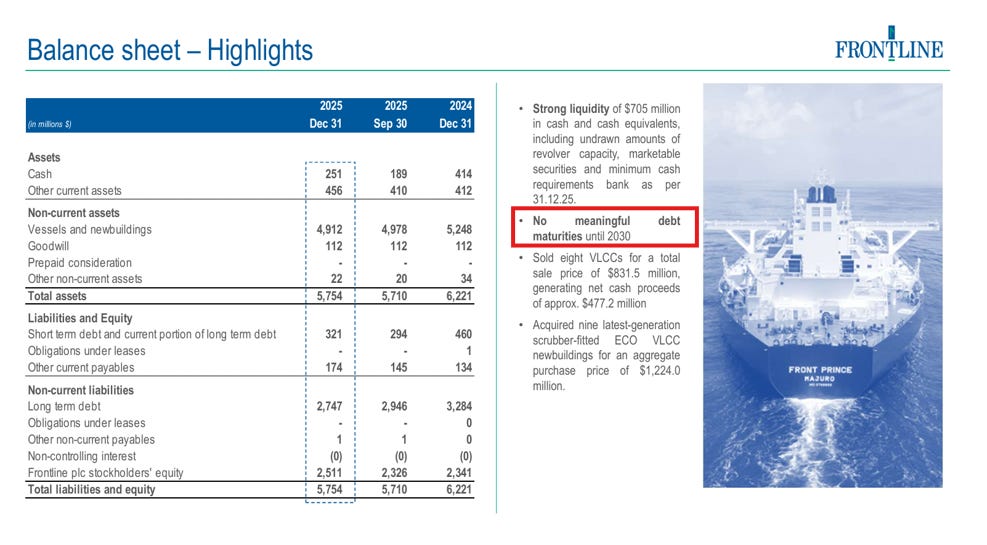

It is worth noting that they have been repaying debt as well:

Source: Frontline plc, Annual Report 2024

Source: Frontline plc, Annual Report 2025

In 2025, they repaid USD 2 billion in debt, thereby enhancing the company’s financial health.

FRO has no meaningful debt maturity until 2030 (6):

Source: Frontline plc, Fourth Quarter Presentation, Feb 2026

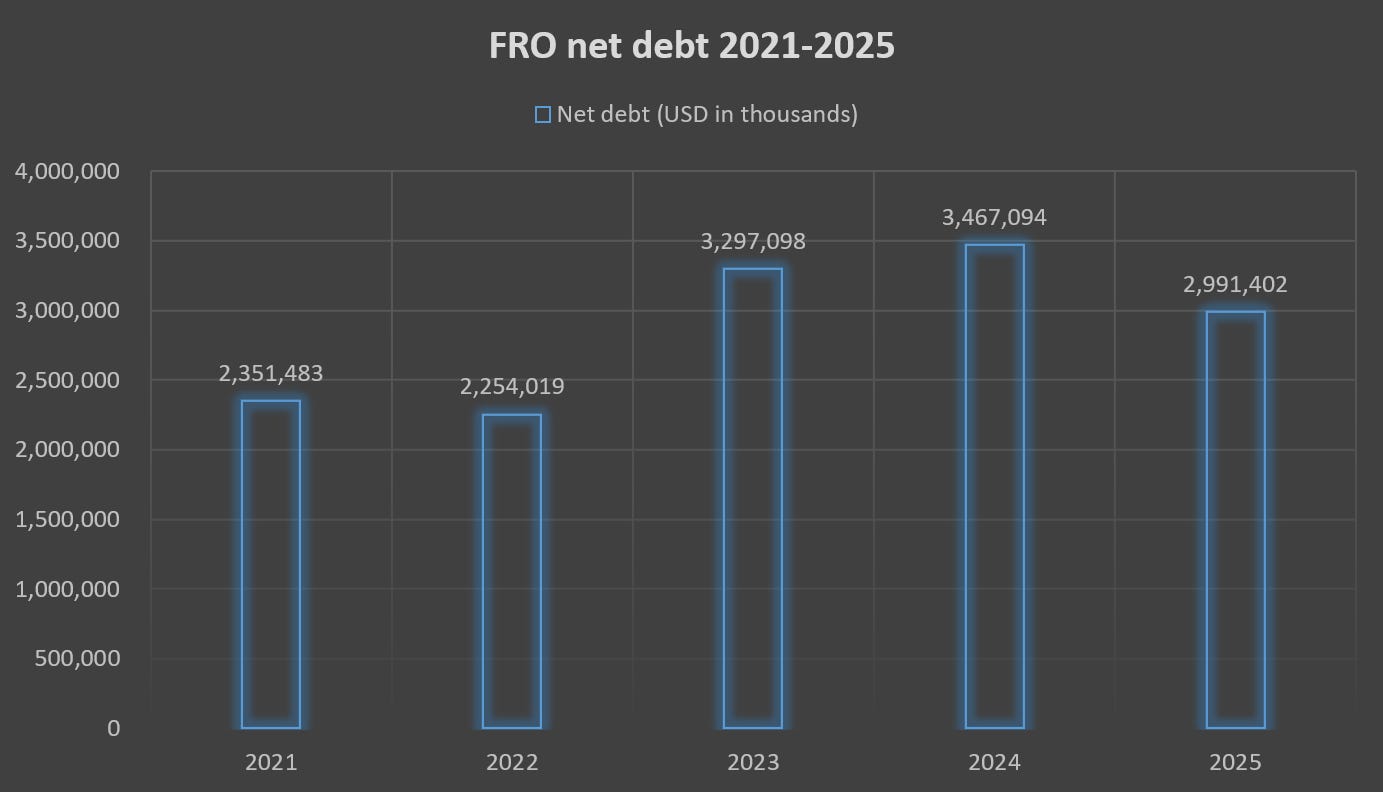

Let’s have a look at the Net Debt.

The company’s net debt has been increasing since 2023, but this is solely attributable to the renewal of its fleet (as mentioned above). The management is allocating capital to reduce it (as mentioned above):

Source: Internal analysis based on FRO annual reports

Let’s dive into what to expect in 2026.

What to expect in 2026?

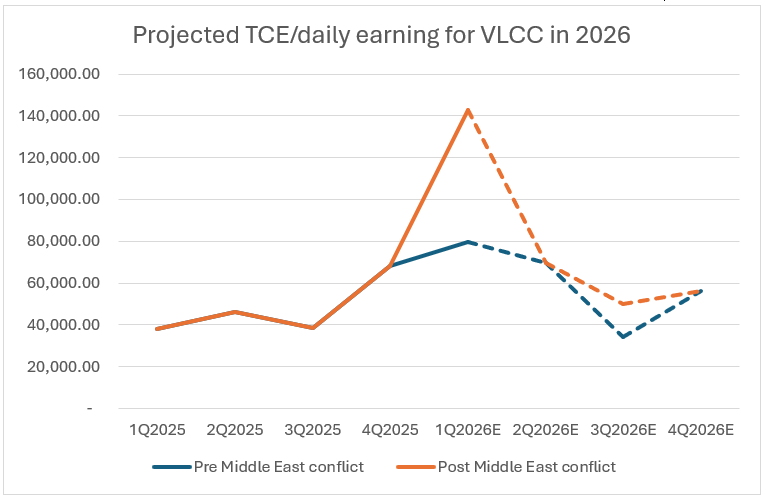

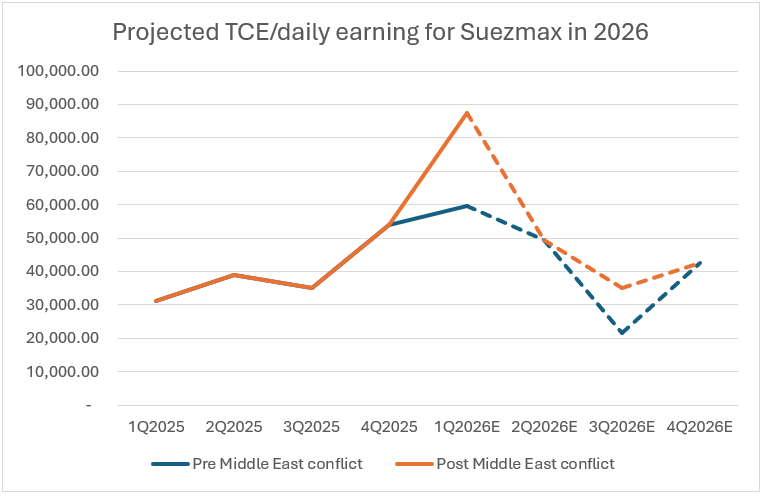

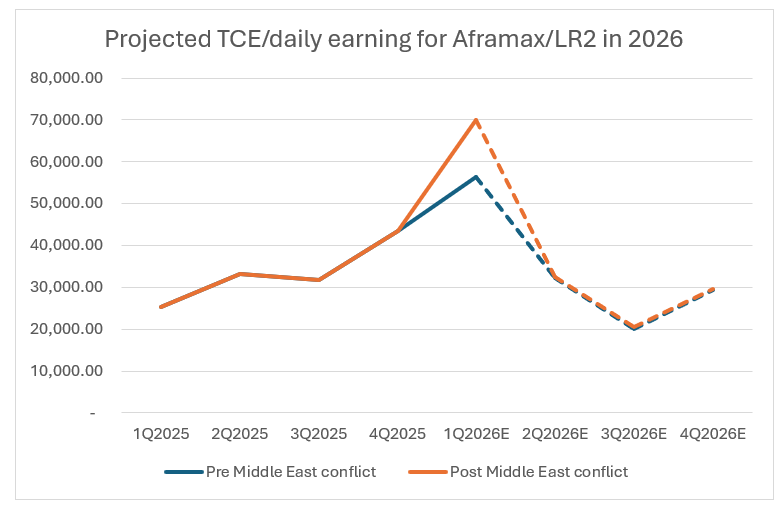

The year 2026 started as a volatile one. The effective closure of the Strait of Hormuz and the conflict in the Middle East are affecting the flow of crude oil and petroleum products. The recent events pushed the daily earnings/TCE for VLCC, Suezmax and Aframax segments to USD 143,300 per day, USD 87,300 per day and USD 82,000 per day, respectively, compared to the pre-conflict scenario (which is shown below with regards to my analysis conducted in Dec 2025 (blue line)):

Source: Internal analysis

Now, if you look at the above charts with pre- and post-conflict projections of daily earnings/TCE, you can see the stark differences, especially the VLCC segment. It is worth noting that the average QTD (quarter to date) of VLCC, Suezmax and Aframax/LR2 made up USD 143,000 per day, USD 87,000 per day and USD 69,950 per day, respectively.

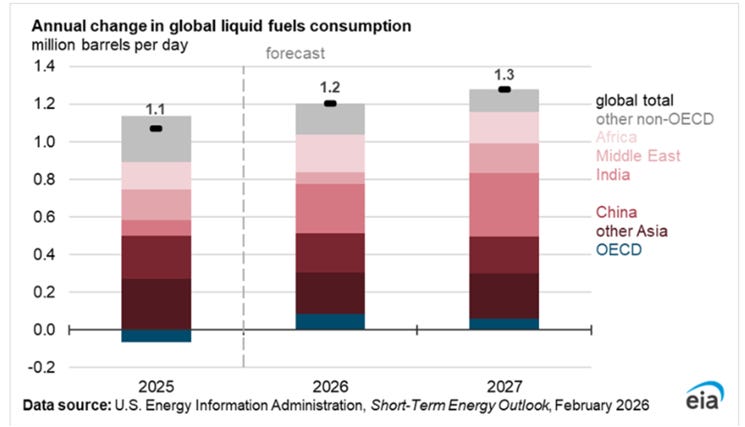

If you read the post “Outlook on tankers market in 2026” dated 13 February 2026, the major driver of the higher daily earnings/TCE in all three segments will be the high projected demand for crude oil (3,4):

Source: EIA

Source: IEA

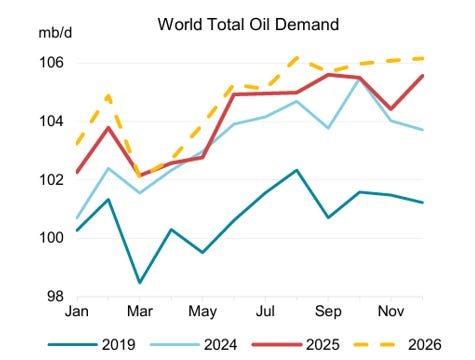

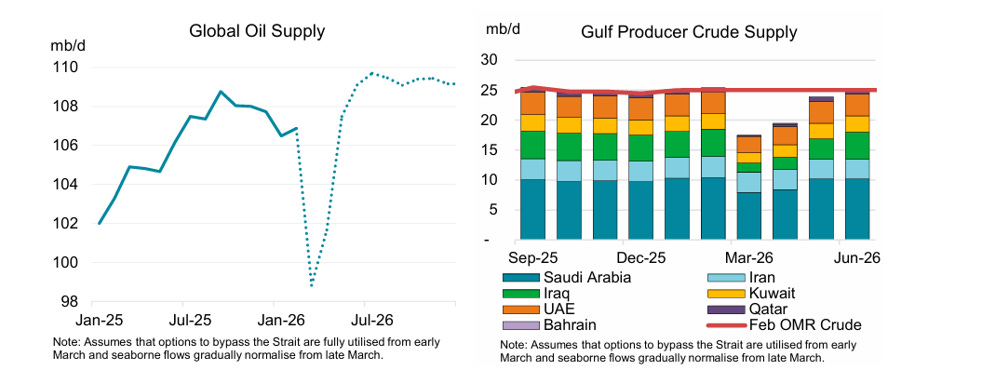

As you can see, the global demand for crude oil in 2026 should be around 106 million barrels per day. However, the supply side of crude oil has been curbed due to the current situation in the Middle East and the Strait of Hormuz:

Source: IEA

Please be aware that Saudi Arabia diverted its export volumes to Yanbu via the Abqaiq-Yanbu pipeline (5). The country can export 5 million barrels per day, out of the 7 million barrels delivered by the pipeline. So, in terms of the export blockade via the Strait of Hormuz, Saudi Arabia is in a better position compared to its neighbouring countries.

It is evident from the above charts that the supply side of crude oil is projected to recover. But again, we simply don’t know how long the current situation will last. There are too many moving parts and news (i.e. noise) that come in. But by looking at fundamental factors, we as value investors have to just take a wait-and-see stance to better understand the risks versus rewards and make an informed decision.

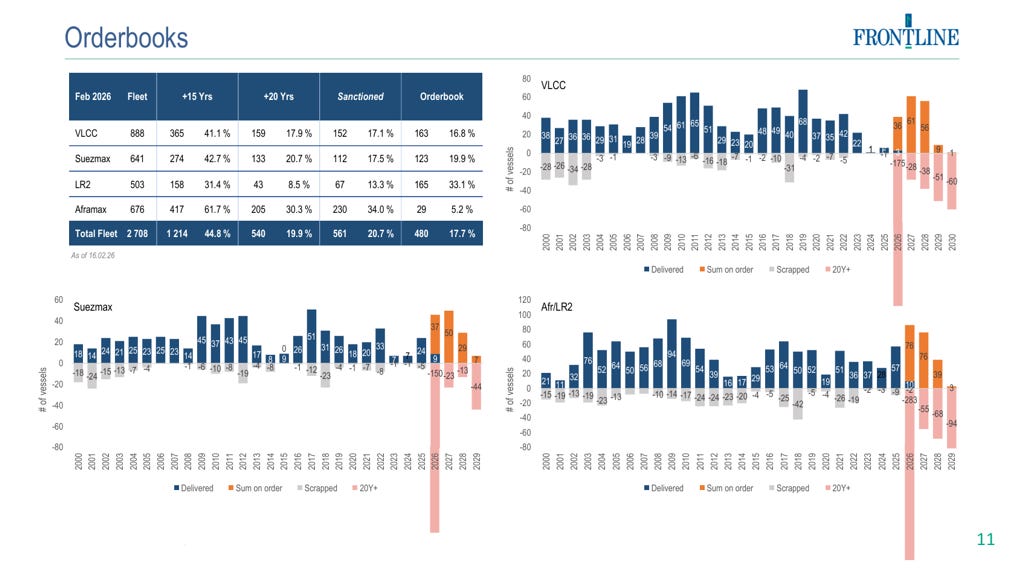

Now, by looking at the current fleet of the global tanker sector (VLCC, Suezmax, Aframax and LR2) and the delivery of new tankers, we have the following picture (6):

Source: Frontline plc, Fourth Quarter Presentation, Feb 2026

As you can see, we have globally 39 VLCC, 46 Suezmax and 86 Aframax/LR2 to be delivered in 2026. But, it is important to underline that out of the current fleet of the above segments, 540 vessels are over 20 years old, and 1,214 vessels are over 15 years old. Thereby, we have an ageing fleet, especially in the VLCC segment.

So, as of today, we have a projected healthy supply and demand for crude oil in 2026, and an ageing fleet of VLCC, Suezmax and Aframax/LR2 segments of the tanker sector.

Now, let’s look at the potential risks.

Risks

The major risk is related to the prolonged conflict in the Middle East and the effective closure of the Strait of Hormuz, where around 25 per cent of global seaborne oil trade transits, out of which 80 per cent are being delivered to Asia (7). Due to Asian importing countries’ dependence on crude oil and LNG imports and being price sensitive, the prolonged conflict and, hence, the elevated prices of commodities that are imported from the Middle East can hurt the regions’ economies. This can lead to financial recession and to curbed demand.

Another potential scenario of the elevated crude oil and LNG prices might be a shift to import coal or alternative commodities instead of crude oil and LNG.

The above two risks might lead to lower imports and lower daily earnings/TCE of the company’s fleet portfolio, thereby affecting the company’s revenue, net income and free cash flow.

What does the current stock price tell us?

The stock is up 47 per cent YTD:

Source: Frontline plc

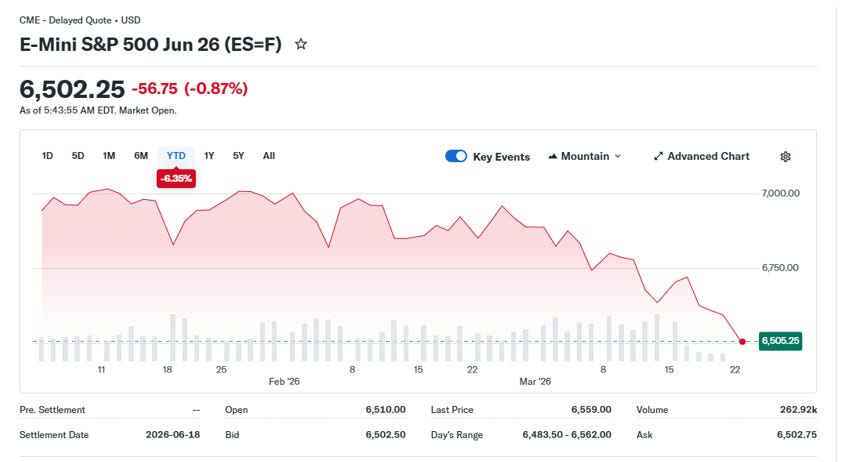

If you compare the above YTD return with the S&P 500 index, the index is (6.35) per cent (yes, negative!):

Source: Yahoo Finance

The reason lies in the various factors (geopolitical and fundamental) mentioned above that drove the stock price of FRO up. All aspects of the current situation have already been priced in by the market participants, and we have to see how things will evolve going forward. The most difficult questions to be answered are the following:

1) How long will the current situation in the Middle East and the Strait of Hormuz last?;

2) What are the repercussions of the current conflict?; and

3) What will happen with the Strait of Hormuz once the conflict is resolved? Will the passage be a safe one?

A lot of questions but no answers. And therefore, it is difficult to assess and make a well-informed decision, as there are too many moving parts of the puzzle. And from a value investing perspective, the current price of FRO seems to offer more risk than reward, although the price might even go to USD 45-50 per share. But it might drop to USD 20-25 per share, too. That’s why the stock, considering its current level, relevant uncertainties and geopolitical situation, should be considered as a bet from a value investor’s point of view.

In this case, we have to be patient and try to understand if the current price offers us more risk or more reward. We like low-risk/high-reward options. According to Peter Lynch (8), we have to invest in cyclical stocks (which is the case of the shipping industry) when earnings are the weakest, and the public sentiment is at its worst. We do not try to time the market here, as it is a fool’s errand approach. We try to decide whether to buy the stock by applying a bottom-up approach, by looking at the variables that can affect the fundamental factors and building a thesis accordingly.

From a value investing point of view, the stock is on the waiting list for a low-risk/high-reward offer. The company is very solid, but the price is a bit pricey.

But as I mentioned before, it is up to you, my fellow value investors, to decide how the position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 https://www.frontlineplc.cy/history/

2 https://www.frontlineplc.cy/fro-strategic-fleet-renewal-and-expansion/

3 https://www.eia.gov/outlooks/steo/report/global_oil.php

4 https://iea.blob.core.windows.net/assets/a25ddf53-cd6c-4910-ac90-16bfd28399e7/-12MAR2026_OilMarketReport.pdf

5 https://en.mercopress.com/2026/03/17/saudi-arabia-diverts-more-crude-to-the-red-sea-to-bypass-hormuz-but-alternative-capacity-remains-limited

6 https://ml-eu.globenewswire.com/Resource/Download/a963a87d-88e0-48ea-ac19-04d5183cb3e1

7 https://www.iea.org/about/oil-security-and-emergency-response/strait-of-hormuz

8 https://finance.yahoo.com/news/peter-lynch-invest-cyclical-stocks-225357637.html