Deep Dive: Himalaya Shipping Ltd.

Ticker symbols: HSHP and HSHP.OL

(published on Substack on 31 Mar 2026)

Business overview

Himalaya Shipping Ltd. was established in 2021 and became a publicly listed company, first enlisting in 2022 on Euronext Growth Oslo and Euronext Expand. In 2023, the company conducted an IPO in the U.S. and started to trade on the New York Stock Exchange (NYSE). The company’s ticker symbols are HSHP (NYSE) and HSHP.OL (Euronext Oslo Bors).

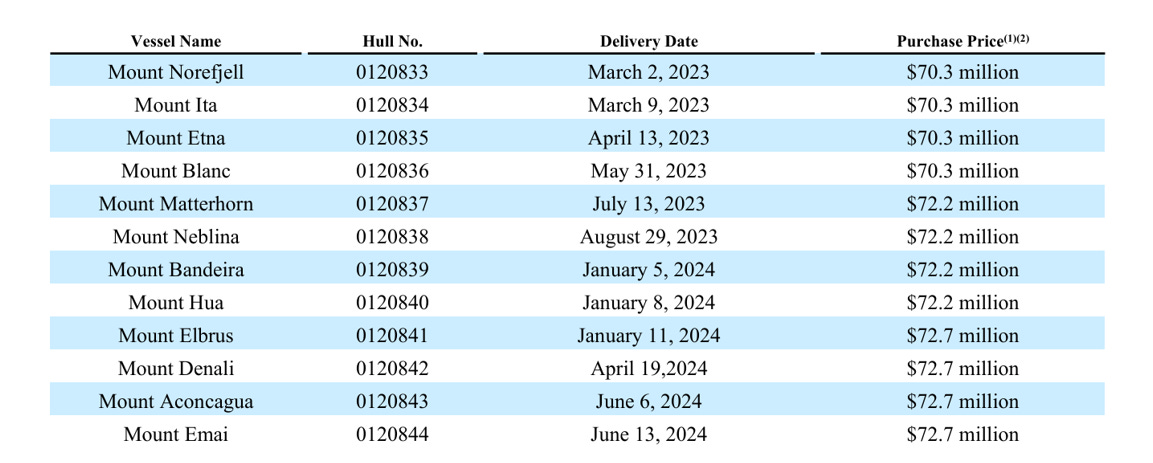

The company is operating solely in the transportation of dry bulk commodities and has a focused portfolio of 12 modern Newcastlemax dry bulk carriers (with a deadweight of 210,000 mt) with an average age of 2.5 years:

Source: Himalaya Shipping Ltd.

So, the company is young, and its fleet is one of the youngest in the shipping industry. Its dry bulk carriers operate globally, namely, the key routes are Brazil to China and Australia to China.

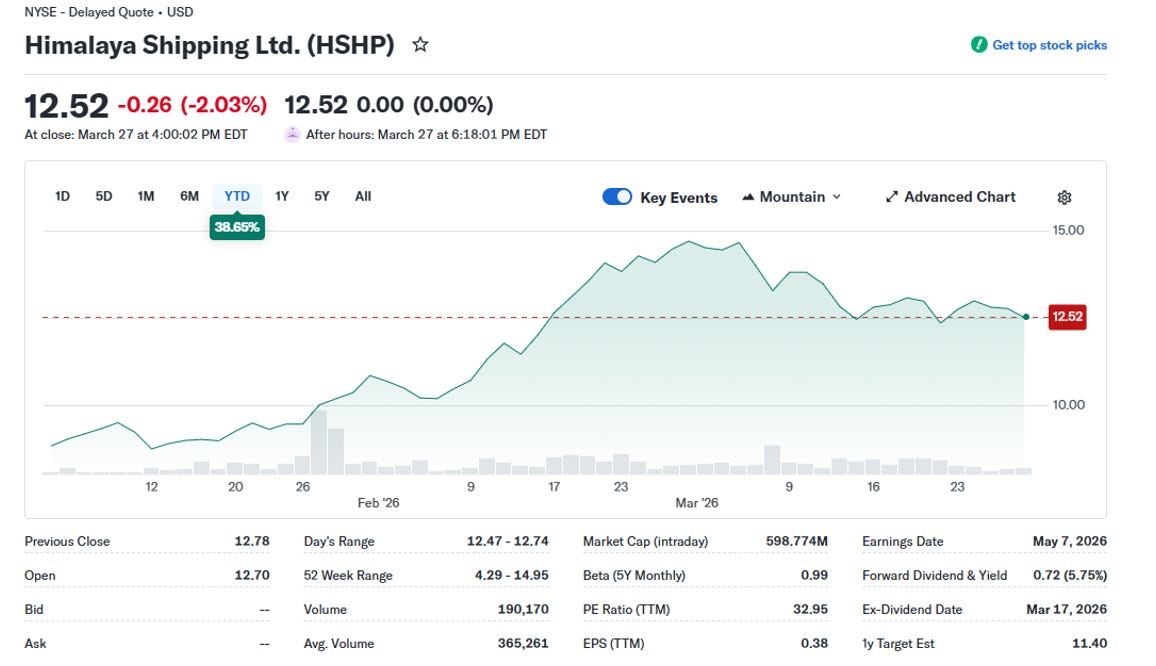

The market capitalisation is USD 599M with a PE ratio of 32.95:

Source: Yahoo Finance

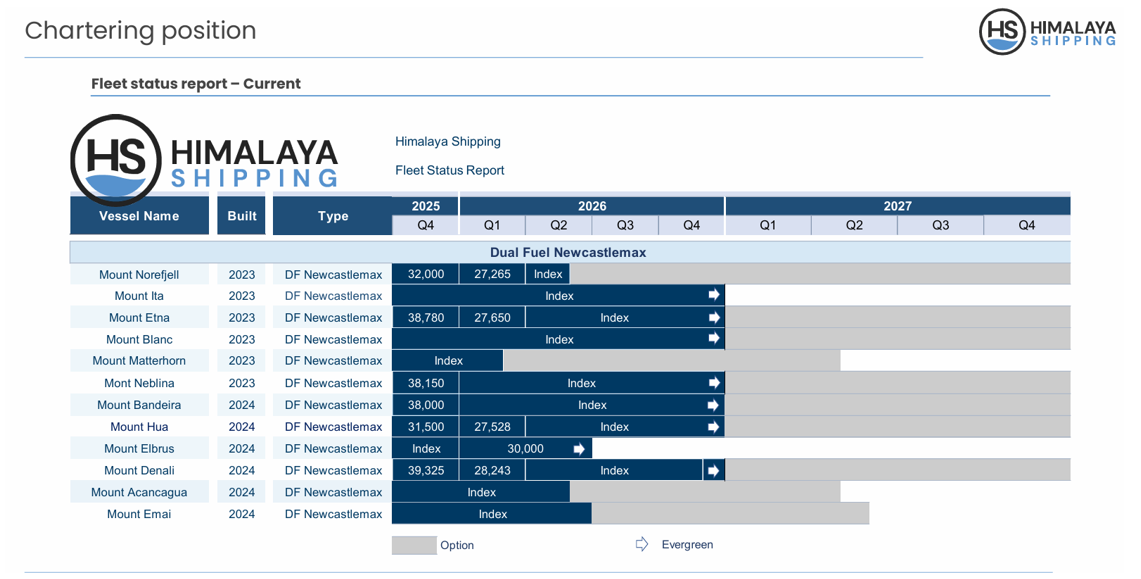

The company’s strategy in terms of the employment of the fleet is to lease its carriers on index-linked time charters (1):

Source: Himalaya Shipping Ltd.

It is worth noting that the index-linked time charters are linked to the Baltic Dry Index (BDI) benchmark instead of the usual time charter rates, which are fixed within the agreed time frame. I.e., if the BDI fluctuates, so does the revenue of the company. The company’s index-linked time charters are linked to the Baltic Capesize Index (BCI), which is a sub-index of BDI.

Below is the interactive map of BCI routes globally (2):

Source: Baltic Exchange

Now, as the company has a modern fleet and all expenses related to the acquisition of new dry bulk carriers have been booked, we should expect lower capital expenditures (in the Cashflow Statement) going forward and an improvement in free cash flow.

The structure of the management is a bit peculiar, namely, the CEO (Chief Executive Officer) and CFO (Chief Financial Officer) are contracted from another publicly listed dry bulk company. We will discuss this subject in more detail in the Risk section of this post.

Let’s dig into financial results.

Financials

So, the company had a very good year in terms of revenue, net income and FCF:

Source: Internal analysis based on HSHP reports

As you can see from the above table, the FCF from 2021 to 2024 was negative due to the acquisitions of Newcastlemax dry bulk carriers.

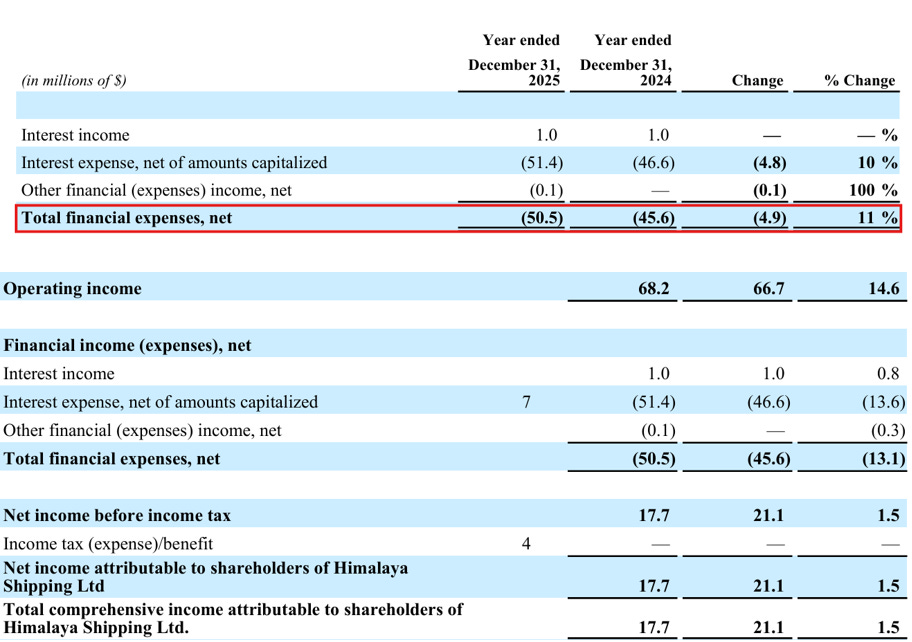

The year 2025 ended slightly lower in terms of net income due to increased interest:

Source: Himalaya Shipping Ltd.

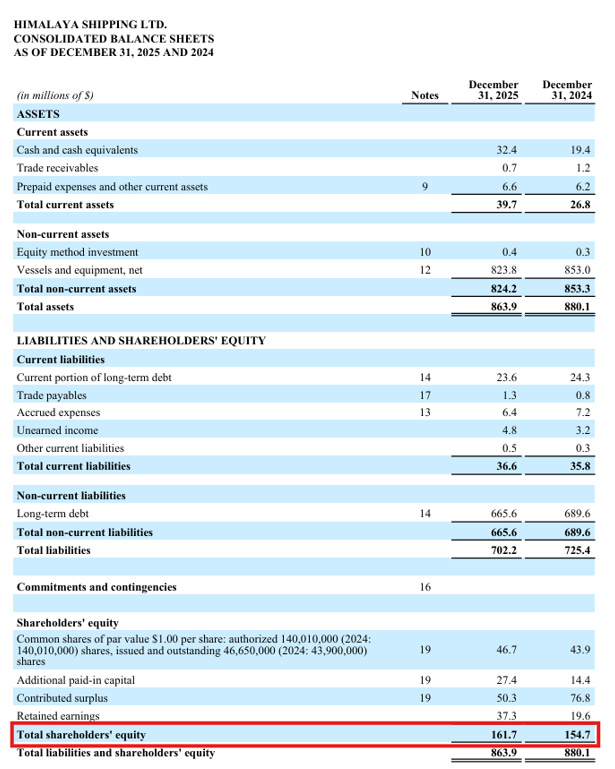

The stockholders’ equity is very low at USD 162 million:

Source: Himalaya Shipping Ltd.

The reason lies simply in the structure of HSHP’s financing model. It is worth noting that the company uses sale-leaseback (SLB), which means that the company is effectively financed by external lessors, leading to huge liabilities and a lower equity portion in the balance sheet. HSHP has 3 sale-leaseback financing agreements for all its carriers of the fleet:

1. AVIC International Leasing Co., Ltd.

2. CCB Financial Leasing Co., Ltd.

3. Jiangsu Financial Leasing Co., Ltd.

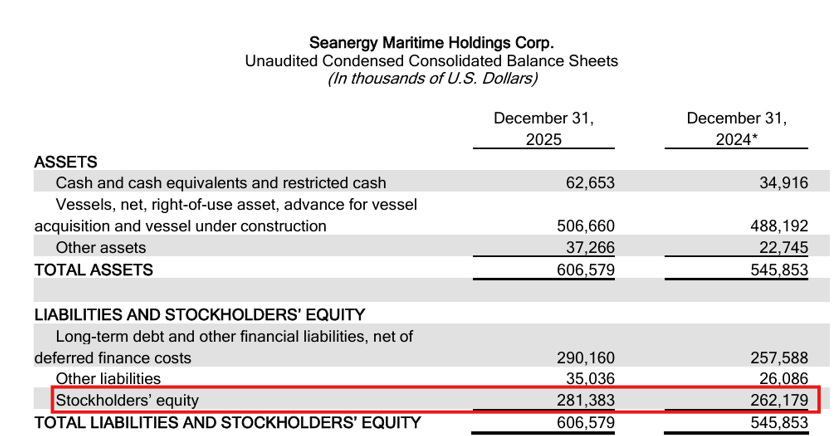

Recently, we discussed another company called Seanergy Maritime Holdings Corp. (ticker symbol: SHIP), which is a pure Capesize player, and its shareholders’ equity stood at USD 281 million (for a deep dive research, please check my posts related to SHIP dated 10 Feb 2026 and 10 Mar 2026):

Source: Seanergy Maritime Holdings Corp.

In the case of SHIP, the company owns most of its dry bulk carriers and, of course, uses bank debt, but keeps meaningful equity in ships.

The company has USD 32.4 million of cash and cash equivalents:

Source: Himalaya Shipping Ltd.

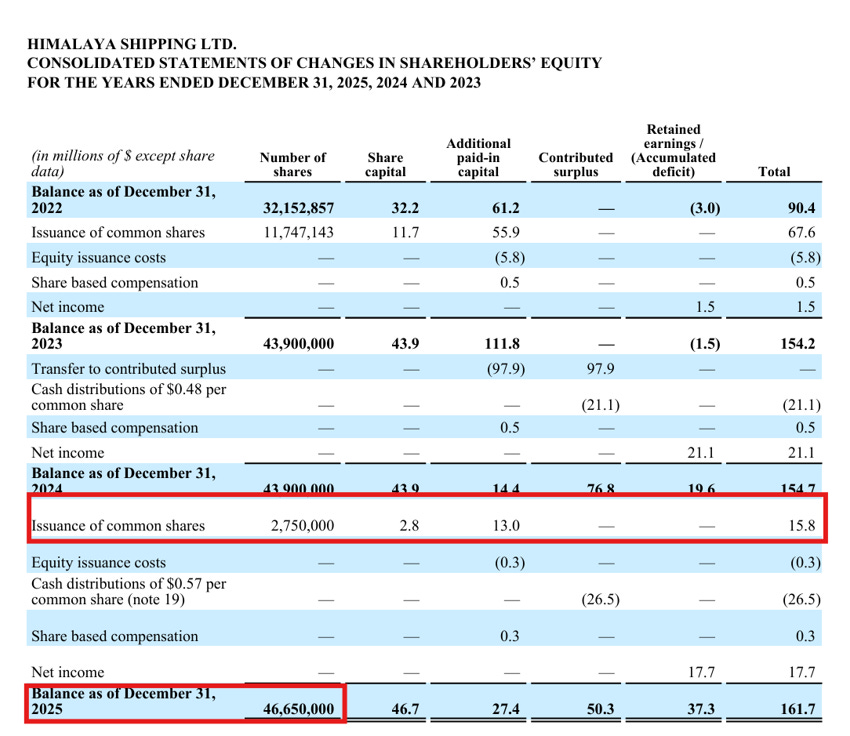

In 2025, HSHP issued an additional 2,750,000 shares and increased the number of shares outstanding to 46,650,000 and raised additional USD 15.8 million:

Source: Himalaya Shipping Ltd.

The company is repaying the long- and short-term debt:

Source: Himalaya Shipping Ltd.

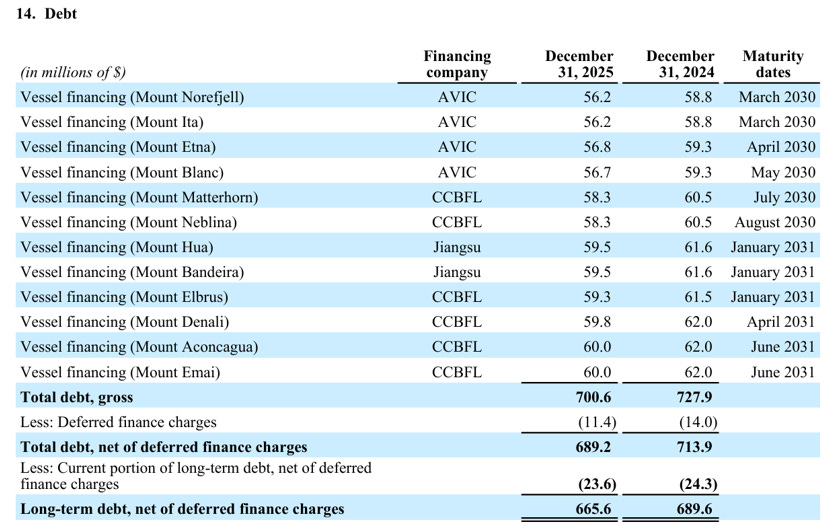

Most of HSHP’s debt matures in 2030-2031:

Source: Himalaya Shipping Ltd.

So, as we analyse the above data, what can we expect for 2026? Is this a company to be considered as a value investment?

What to expect in 2026?

The company’s fleet, as mentioned above, operates globally, and its main trading routes are Brazil to China and Australia to China. Hence, the company’s employment of its fleet is heavily dependent on China’s imports of iron ore and bauxite. However, as mentioned in my post “Bullet points on the trends in the Dry Bulk Shipping Sector for 2026” dated 06 Feb 2026, there is an addition to the trading routes. The Simandou mine (Guinea, West Africa) has one of the largest iron ore deposits and has already shipped its first cargo to China (3).

In addition to the above, Brazil’s export of iron ore is expected to remain strong in 2026 after record export volumes in 2025 (4). In 2025, Brazil exported 416.4 million tons of iron ore, and Vale expects its iron ore output to rise by 3 per cent in 2026 (5).

China’s import of iron ore is slated to grow by 2.6 per cent, with 36-38 million tons more compared to 2025 (6). It is worth noting that, in 2025, China imported 1.26 billion tons of iron ore. The market already sees the above projections, as China’s iron ore imports for the first two months of 2026 are 10 per cent higher compared to the same period of 2025 and made up 210.02 million metric tons (8).

So, we have a strong supply and demand related to iron ore projections in 2026, which should be beneficial for Capesize and Newcastlemax segments due to long distances between the ports of loading and discharge.

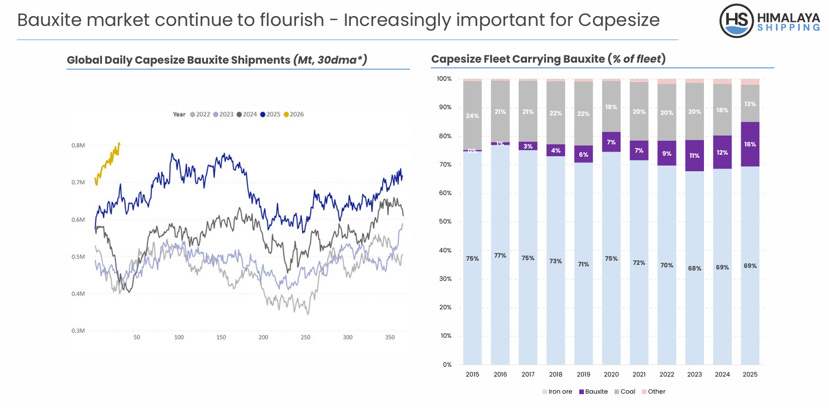

Below are the charts of global daily bauxite exports and the percentage of iron ore, bauxite and coal that were transported on Capesize carriers (1):

Source: Himalaya Shipping Ltd.

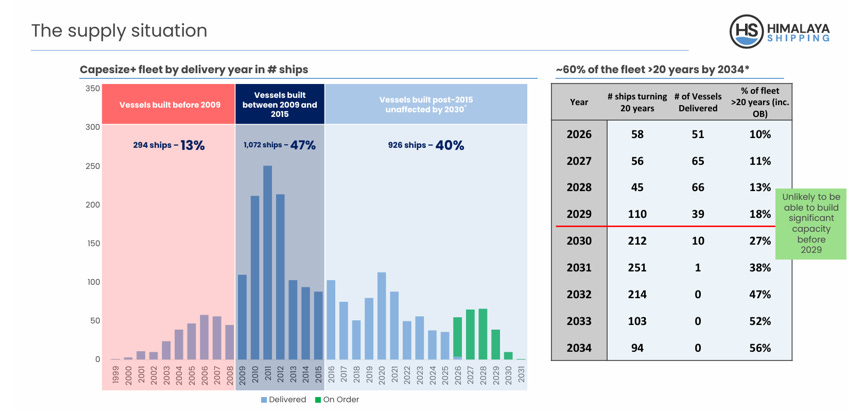

If we look at the current fleet of Capesize and Newcastlemax and deliveries of new carriers, we have the following situation (1):

Source: Himalaya Shipping Ltd.

Namely, due to the low supply of Capesize carriers and the ageing fleet, around 60 per cent of the fleet will be over 20 years old by 2034.

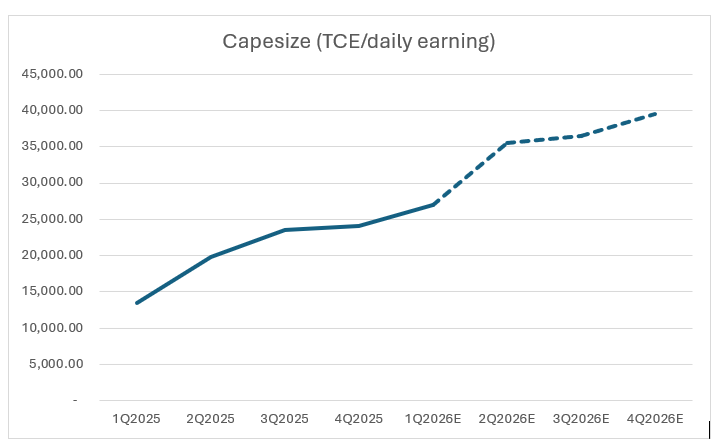

The above fundamental factors should be beneficial to Newcastlemax and Capesize daily earnings/TCE. Please see below the projections for 2026:

Source: Internal analysis

Now, let’s look at one of the most important aspects of value investing.

Risks

Please see below the elaborations of risks related to the HSHP stock:

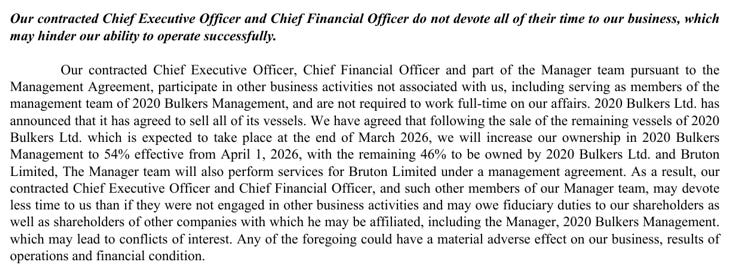

1. A distinct red flag that is important to mention relates to the contracted CEO and CFO of HSHP. It is worth noting that the contracted CEO and CFO of HSHP are also the CEO and CFO of the publicly listed company called 2020 Bulkers Ltd. (ticker symbol: 2020.OL), which is also engaged in the dry bulk commodities transportation.

Both Mr Lars-Christian Svensen (CEO) and Mr Vidar Hasund (CFO) assumed their respective contracted roles of HSHP on Apr 1, 2025.

Now, it is important to note that HSHP has signed with 2020 Bulkers Management, “The Management Agreement”. This agreement outlines that the manager will provide commercial management for the HSHP fleet, technical/operational/newbuilding oversight, etc. Now, in the shipping industry, it is quite common to assign the technical/operational aspects of the business to professionals who are also operating other businesses in the same industry. However, as mentioned in the excerpt below, having the commercial management of the HSHP fleet (day-to-day chartering or strategy) also in charge of other companies might cause an adverse effect on the business.

HSHP in their annual report openly advise of risks related to the above matters. Please see below a relevant excerpt:

Source: Himalaya Shipping Ltd.

2. The second risk, which is important to underline, is related to the financial arrangements of HSHP, namely its sale-leaseback (SLB) structure.

If we look at SLB structure, the company HSHP does not own the vessels that are on its balance sheet, but has the right to use the vessels, which means that the assets are owned by a lessor and, in this case, by AVIC International Leasing Co., Ltd., CCB Financial Leasing Co., Ltd., and Jiangsu Financial Leasing Co., Ltd. And that’s why we see such a low level of shareholders’ equity in the balance sheet mentioned above.

Now, is it risky? From a value investing perspective – yes.

Due to the cyclical nature of the shipping business, the revenue, net income and FCF go up and down in waves. If there is a recession or lower demand, it can negatively impact the company’s earnings, especially when the company has such a high ratio of liabilities versus assets. How will they meet their obligations? Because HSHP does not fully own the vessels, the lessor has the right to terminate the lease and take back the vessels, in certain instances, which can lead to loss of revenue, and that imposes a huge risk for the company and shareholders.

3. The last risk that should be considered is associated with the current situation in the Middle East and its effect on the Asian economies, which are heavily dependent on the import of LNG and crude oil from the Middle East producers. With the Strait of Hormuz effectively closed and the prices of the mentioned commodities elevated, we already see the impact. China, being the largest importer of crude oil and LNG in the world, can have an economic slowdown, and that can have a domino effect. Namely, the import of iron ore and bauxite might fall, which could negatively affect the earnings of the company HSHP.

What to do?

The stock of HSHP is up 39 per cent YTD:

Source: Yahoo Finance

Now, we discussed previously that we should have a constructive supply of and demand for iron ore and bauxite, and these fundamental factors should be beneficial to companies that have Newcastlemax and Capesize carriers in their portfolio. We also discussed the potential risk related to the demand from China due to the potentially prolonged situation in the Middle East and its impact on the Chinese economy.

Now, going back to analysing HSHP and evaluating risks and rewards, from a value investing perspective, the risks outweigh the rewards. As value investors, we focus on limiting risks and gaining as much upside as possible.

In the case of HSHP, the risks in the current setup appear too important to ignore (potentially preoccupied management and the highly leveraged SLB structure), which does not fit the philosophy of value investing.

For a deeper understanding of the value investing in shipping philosophy, I would suggest reading the newsletter “Value investing and cyclical stocks” posted on 27 Mar 2026.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 https://storage.mfn.se/f684f250-b622-4aa2-987b-504b9f828a58/himalaya-shipping-ltd-q4-2025-investor-presentation.pdf

2 https://www.balticexchange.com/en/data-services/routes.html

3 https://www.ft.com/content/80f37963-c718-4f8b-8d77-0f0d5b1c99fe

4 https://www.bnamericas.com/en/analysis/after-record-high-brazils-iron-ore-exports-expected-to-remain-strong-in-2026

6 https://skillings.net/chinas-iron-ore-appetite-imports-hit-record-1-26-billion-tons-in-2025/

7 https://storage.mfn.se/19267063-fc0b-4d73-9420-f1c57a5ad26d/2020-bulkers-ltd-annual-report-2025.pdf

8 https://www.reuters.com/markets/commodities/chinas-robust-iron-ore-imports-are-going-into-storage-not-steel-2026-03-19/