Deep Dive: Höegh Autoliners ASA (Ticker symbol: HAUTO)

Dear fellow value investors,

Today, we are going to dive into a company operating in the RoRo (Roll-on/Roll-off) segment of the shipping industry. This company owns and manages PCTC (pure car and truck carrier) vessels. In other words, Höegh Autoliners ASA transports cars, trucks, breakbulk, and heavy and high (H&H) machinery from exporters to consumers.

Let’s analyse the business.

Business overview

HAUTO was founded in 1927 and became publicly listed in 2021 (1). The primary business of the company is deep-sea transportation of cars, trucks, etc., on its PCTC vessels. The company operates globally and is very active in the global export trading routes, such as Europe – Middle East, East Asia to Europe, etc.

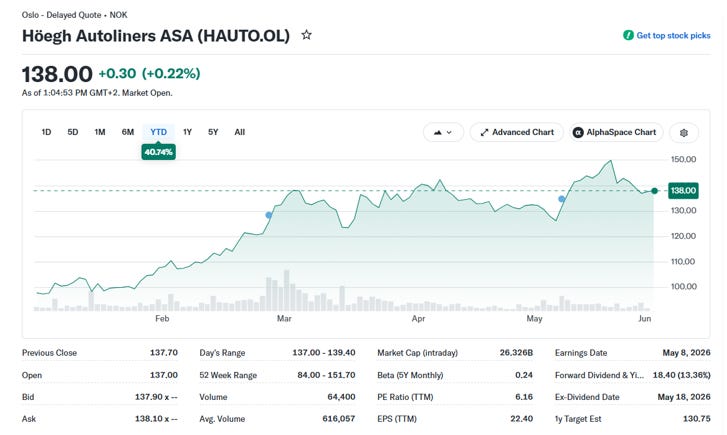

The market capitalisation is around NOK 26 billion (USD 2.6 billion), and its P/E ratio is 6.13:

Source: Yahoo Finance

According to the company’s website (1), its fleet consists of 38 PCTCs with cargo capacity ranging from 2,000 to 9,100 CEU (car equivalent unit). Out of 38 vessels, two are chartered in, and the rest belong to HAUTO. In 2025, they sold two of their older units. The average age of the fleet is 16 years.

It is worth noting that HAUTO’s business is heavily dependent on the export volumes of cars, trucks, etc. and more interestingly, on the import volumes, which are directly linked to the sale volumes.

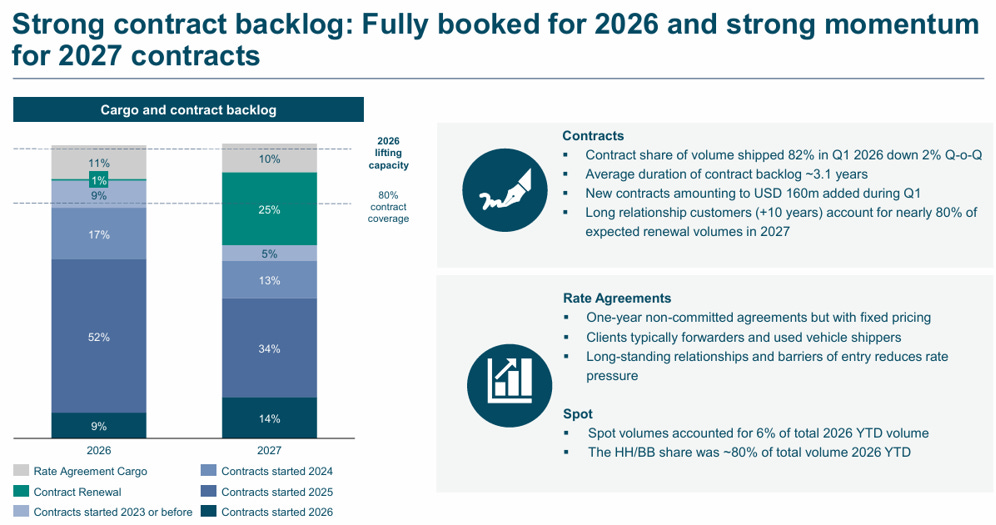

HAUTO’s business model is straightforward. They contract slots for their PCTC vessels on average for 3 to 3.1 years and have long-term relationships with their customers (10+ years). So, the business is predictable in terms of revenue. For instance, the contract slots for 2026 are fully booked and 80 per cent booked for 2027:

Source: HAUTO, Q1 2026 Quarterly Presentation, May 8, 2026

As you can see, the contract renewal was only 1 and 25 per cent in 2026 and 2027, respectively. Only 6 per cent of slots accounted for spot bookings.

However, it is worth noting that despite having a predictable revenue and contracted volumes for 2026 and 2027, the stock of HAUTO is not immune to the price fluctuations, which stem from the market sentiment and news reports, such as the 1-year time charter rates for PCTC vessels, etc.

HAUTO initiated to start reducing emissions by ordering 12 Aurora-class vessels, whose deliveries started in Q2 2024. Their estimation is that these vessels will reduce the carbon emissions up to 58 per cent compared to the current shipping industry’s average (1). The first 8 eight carriers will be run on LNG (liquefied natural gas) and low-sulphur fuel oil, and these vessels will be later converted to run on ammonia. Out of 12 vessels, 8 PCTCs were already delivered during the 2024-2026 period (5 carriers in 2024, 2 carriers in 2025 and 1 carrier in Q1 2026). The last 4 carriers will be delivered in 2027-2028. In other words, they intend to be greener and net-zero by 2040 (zero emissions).

Financials

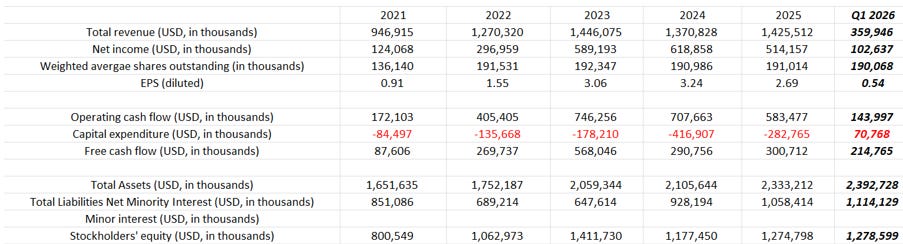

Now, the Q1 2026 results were reported recently:

Source: Internal analysis based on HAUTO reports

FCF is still positive as the only capital expenditures (USD 71 million) the company had in Q1 2026 were related to the instalments of vessels under construction, dry dock expenses and vessel upgrades.

Source: HAUTO, Q1 2026 Quarterly Report

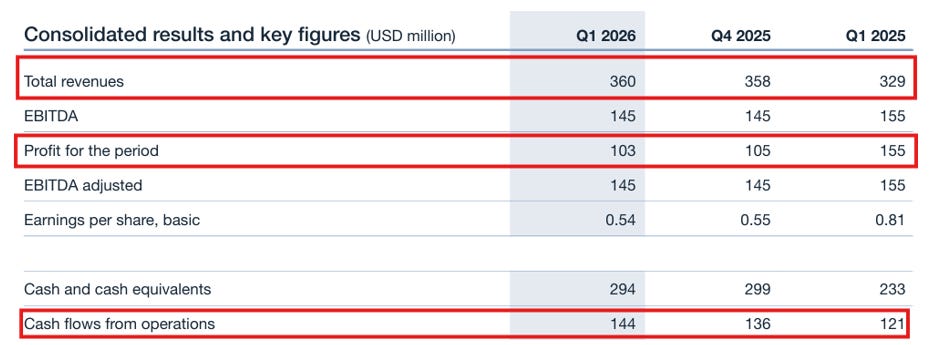

So, if we compare the Q1 2026 results to Q4 2025 and Q1 2025, we can notice the revenue stayed on par with Q4 2025 but was higher than Q1 2025. The net income is similar to Q4 2025 but lower than Q1 2025.

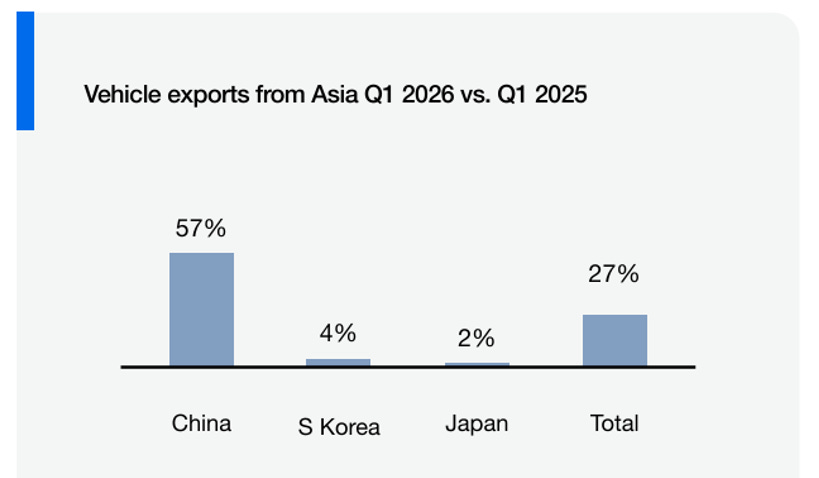

Despite firming PCTCs’ freight rates, increased exports from the Asian region (27 per cent higher in Q1 2026 versus Q1 2025) and particularly from China (57 per cent higher in Q1 2026 versus Q1 2025) and limited available PCTC capacity, the major financial metrics remained stable. The major reason for the metaphorical ceiling lies in the geopolitical disruptions and higher operating costs that absorbed any upside.

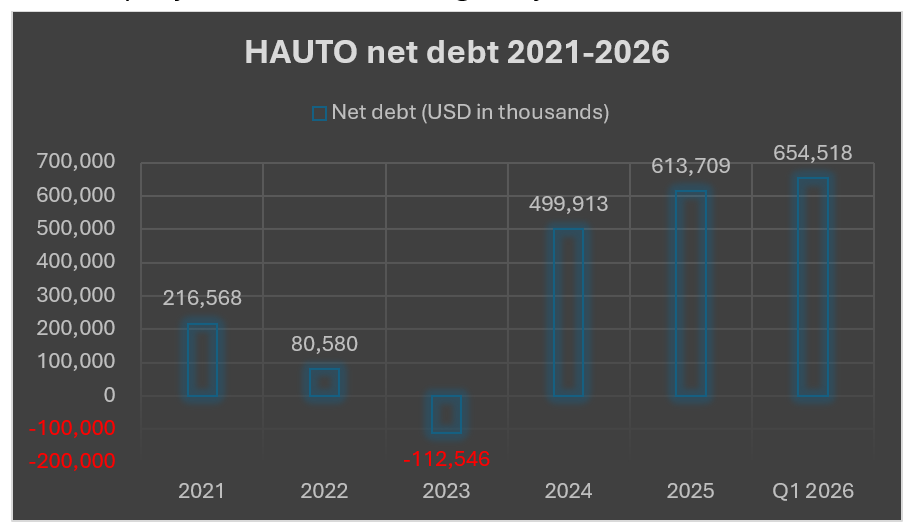

The company’s net debt is climbing bit by bit:

Source: Internal analysis based on HAUTO reports

The reason lies in more borrowings related to ordering new PCTC vessels (i.e. 12 Aurora-class vessels). But the question that remains open for investors is: will these vessels generate enough cash flow despite the potential downturn in the RoRo segment of the shipping industry? We shall discuss it in the next section.

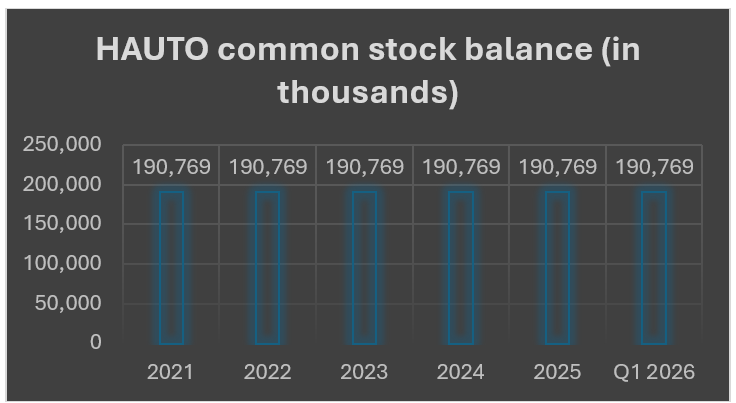

The number of outstanding shares issued in 2021 has been the same, as there have not been any buyback programs applied:

Source: Internal analysis based on HAUTO reports

Cash and cash equivalents as of 31 Mar 2026 stand at USD 294 million, and total shareholders’ equity is as follows:

Source: HAUTO, Q1 2026 Quarterly Report

Their Q2 2026 guidance is that the financial results will be similar to Q1 2026 or a bit lower, due to increased bunker expenses.

Overall, good financial metrics, but let’s analyse the fundamental factors and outlook of HAUTO’s core business.

What to expect in 2026?

As mentioned, the company’s financial performance and PCTCs freight rates depend on export volumes, sales volumes and the global fleet of PCTCs.

Let’s have a look at each realm.

Export volumes

The Asian region is expected to be a driver of global car export volumes, with China being the leading country. As per Reuters (3), Chinese export levels are set to cool in 2026. It is worth mentioning that it is still a growth export, but analysts do not think it will be at staggering numbers as in previous years. One of the reasons is cited as external uncertainties, such as tariffs. For instance, exports of automobiles from South Korea fell by 5.9 per cent (y/y), and the main reasons are the supply disruptions in the Middle East and the impact of the US tariffs (4).

However, despite the gloomy news above, if we look at the export volumes of Q1 2026 versus Q1 2025, there is an increase of 27 per cent (y/y):

Source: HAUTO, Q1 2026 Quarterly Report

The car export volumes from China are 57 per cent higher. So, despite the supply chain disruptions in the Middle East and imposed tariffs (by the EU and US), Chinese exports remain resilient. Japanese export volumes also remained resilient despite the US tariffs of 15 per cent.

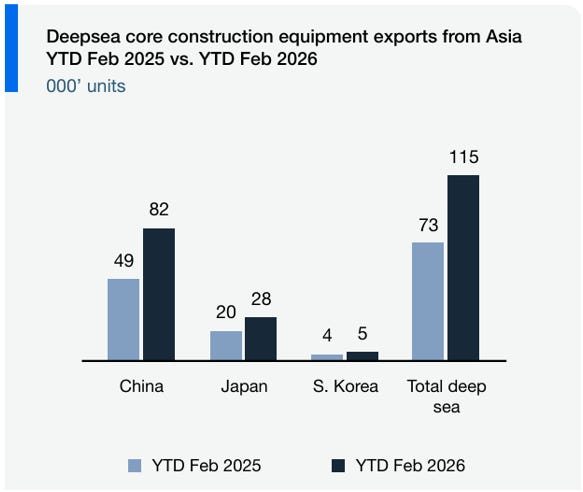

If we look at the H&H (high and heavy) or core construction equipment exports, the picture here is also positive. The export of Chinese construction machinery has surged by 33.4 per cent in early 2026 (5). The above is supported by the following chart:

Source: HAUTO, Q1 2026 Quarterly Report

The above positive Q1 2026 results related to the export volumes of both vehicles and H&H equipment are being confirmed by other RoRo shipping companies such as Wallenius Wilhelmsen ASA (WAWI).

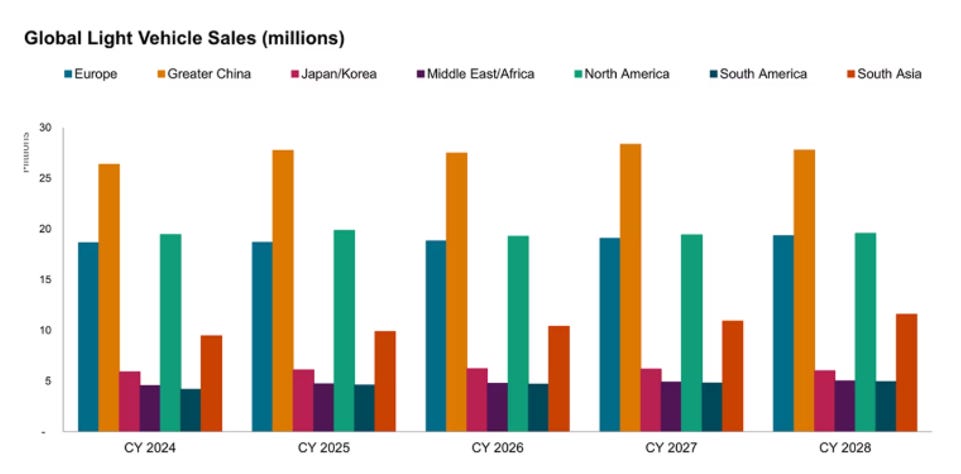

Global sale volumes

In 2025, the global light vehicle sales were about 91.7 million vehicles (6), which, by the way, was the first year exceeding the 2019 figures of 89.9 million cars. The analysts and industry experts project a modest or stable growth in 2026. The expected global sales are forecasted at 91.8 million units, which is essentially a flat sales volume:

Source: S&P Global

Now, the major hurdles to the limited growth of the global sales are related to the ongoing tariff policies, paired with high energy prices, which directly impact the inflation rates and hence interest rates, etc.

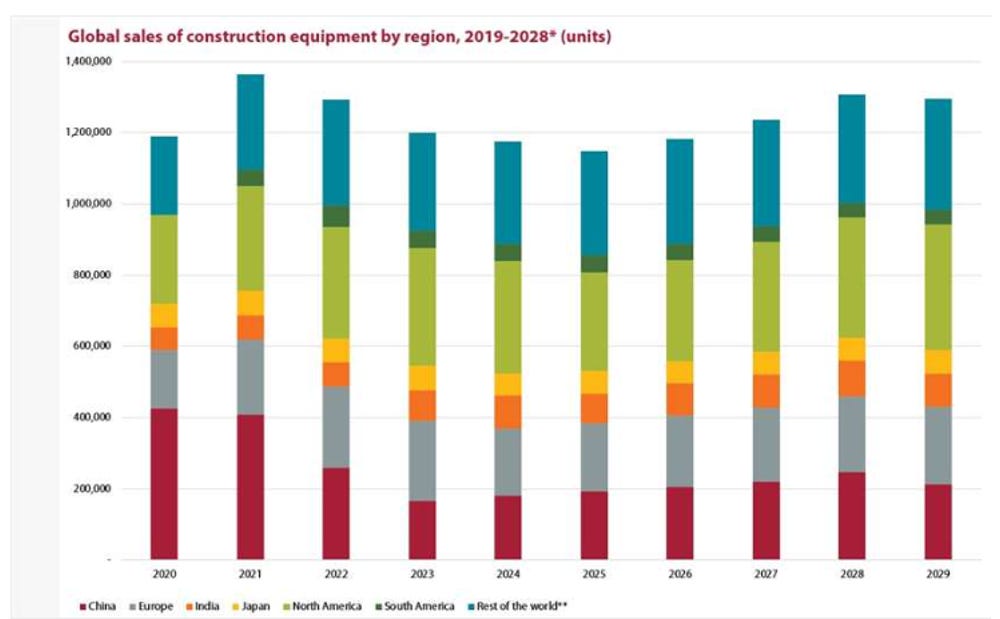

In relation to the H&H global sales volumes, it is estimated to have a modest growth too. In 2025, the global construction equipment sales hit their lowest since 2021 (the peak). Namely, a decline of 7 per cent (y/y) was expected in 2025 and made up 1.30-1.35 million units (7):

Source: Construction Briefing

Nevertheless, the same source projects a recovery in 2026 and forecasts that the global sales units will be around 1.35-1.45 million units. But let’s not forget about the interest rates that are still high and elevated energy prices, which still do not allow the central banks around the world to reduce the rates due to the inflation rate.

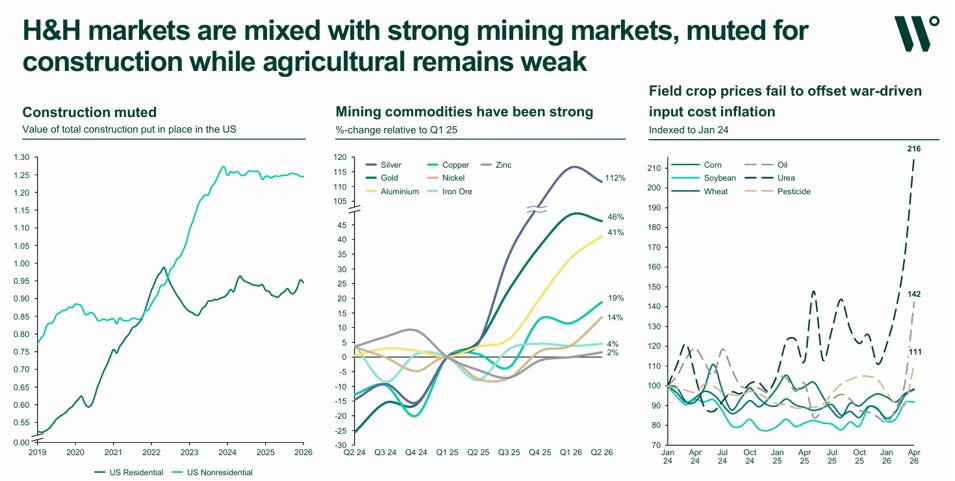

According to Wallenius Wilhelmsen ASA (WAWI), the only driver of the H&H market in 2026 was the mining sector:

Source: WAWI, Q1 2026

As you can see, the construction and agricultural spheres remained muted or weak.

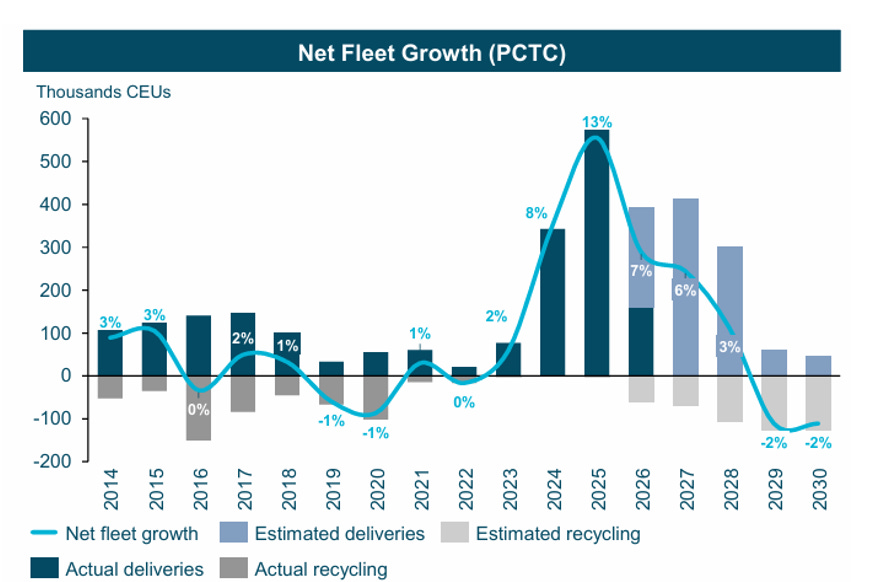

Global PCTC fleet

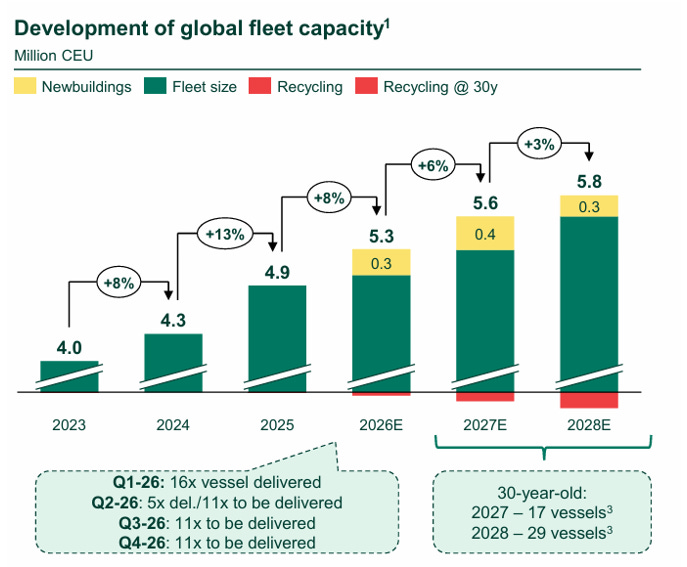

The global deep sea PCTC fleet as of 31 Dec 2025 stood at 773 vessels (8). In Q1 2026, around 16 vessels were delivered, and an additional 38 carriers are to be delivered in the current and subsequent quarters (9). So, as of today, we expect the fleet of the PCTC vessels to grow in 2026 to 827 carriers with limited recycling. It is worth noting that in 2027 and 2028, only 17 and 29 vessels, respectively, will be 30 years old:

Source: WAWI, Q1 2026

Source: HAUTO, Q1 2026 Quarterly Report

Now, if we look at the above two graphs from HAUTO and WAWI, we can see that there is an expectation of overcapacity in the PCTC fleet. Which means that the global export volumes growth will not be able to absorb the delivered growth of the PCTC fleet. However, as of today, due to the closure of the Strait of Hormuz and the Red Sea passages, there is an inefficiency in the supply chains. Namely, due to the closure of the mentioned routes, the voyage from Asia to the Middle East lasts now 44 days (via the Cape of Good Hope), the Mediterranean Sea and then directly to the Red Sea ports of Saudi Arabia instead of the usual 16.4 days. This dislocation of the trade route led to the longer voyages and hence, longer utilisation of the PCTC vessels, which in turn, led to the firming of time charter rates. Hence, any overcapacity of the delivered new PCTC has been absorbed by the longer trade routes and voyages.

Risks

The major risk is the slowdown of the global GDP. China, being the driver of the global export growth, absorbed in 2025 most of the excessive growth of the new PCTC deliveries, which resulted in firming freight pricing (8). According to the IMF (10), Chinese real GDP growth in 2025 was 5 per cent, and for 2026 the forecast is slightly lower and is pinned at 4.4 per cent (11). The global GDP growth was pinned at 3.1 per cent, which was downgraded from 3.3 per cent (12), due to the Middle East conflict and high energy prices. Which means that if there is a slower GDP growth, there will be fewer car imports, which in turn would potentially lead to softer RoRo freight rates. That should pose a risk of softening HAUTO’s stock price, even though HAUTO has already chartered out all available slots for 2026 and partially for 2027. Furthermore, in our opinion, the growth of the delivery of new PCTC vessels won’t be absorbed by the global car imports growth.

In addition to the above, if there is a resolution of the Middle East conflict and the Strait of Hormuz is open again, the fleet utilisation inefficiency will be gone, and the voyage from Asia to the Middle East customers will take 16.4 days instead of 44 days. This might lead to softer car transporting freight rates, which have the potential to affect the HAUTO’s stock price negatively.

Stock valuation

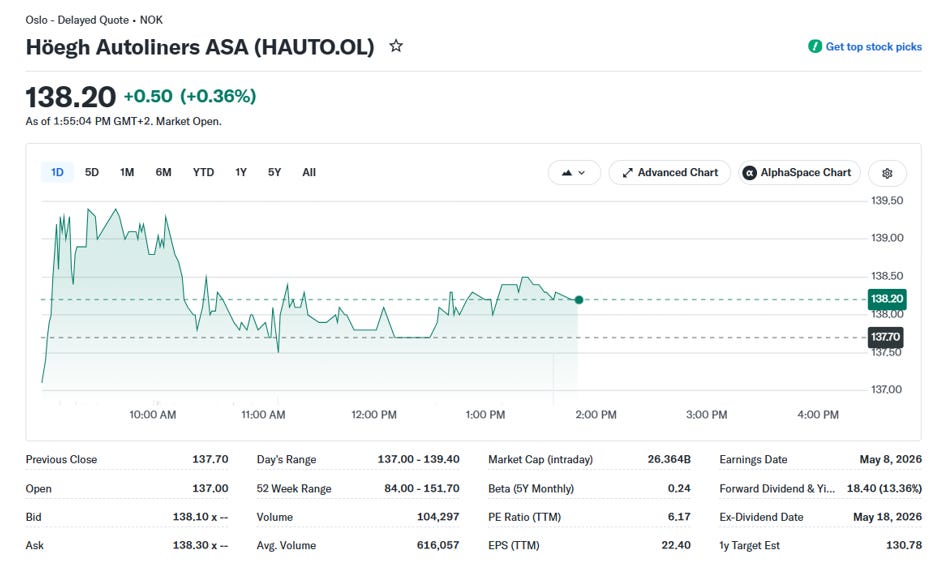

Now, let’s have a look at the stock valuation. At the time of writing (02 June 2026), HAUTO was trading at NOK 138.20:

Source: Yahoo Finance

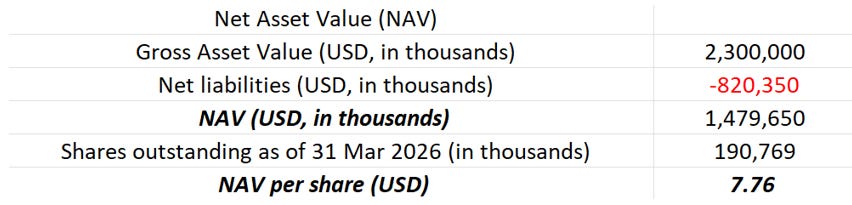

NAV per share is USD 7.76:

Source: Internal analysis

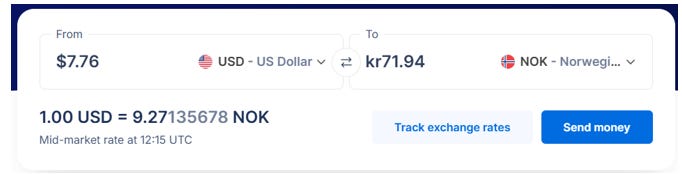

Now, USD 7.76 per share makes NOK 71.94 per share (at the time of writing on 02 Jun 2026):

Source: xe.com

The analysts pin the 12-month target price at NOK 130-136 (USD 14.02-14.66). Now, if we compare the NAV per share, the analysts’ price target and the current level of HAUTO stock price, we can see that it’s overvalued versus our NAV per share and fairly valued/a bit overvalued versus the analysts’ price target.

Now, if we look at the fundamental factors such as Asian car and H&H exports, global car sale units and PCTC global fleet, we can conclude that the risks of overcapacity of new deliveries of PCTC vessels might push the stock of HAUTO down, even though the company has already contracted its spots in 2026 and 80 per cent in 2027 at firm rates. However, as mentioned above, despite the above revenue visibility, the company’s stock is not immune to the market sentiment, both in the shipping and equity markets. Namely, if for some reason the time charter rates soften, it will immediately have an effect on the company’s stock price.

What is interesting is that the analysts in Jan-Feb 2026 were downgrading the 12-month target price to NOK 75-80, which is approximately where our NAV per share is (USD 7.76 = NOK 72.00). The only thing that changed is the dislocation of the supply chain, which is not a fundamental shift.

As of now, due to risks outweighing rewards, we shall wait till the stock price offers a low-risk/high-reward option.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, don’t hesitate to get in touch with me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Please find us on: https://valueinvestinginshipping@substack.com

Sources:

1 Höegh Autoliners ASA

2 HAUTO, Q1 2026 Quarterly Presentation, May 8, 2026

5 https://china-insights.org/chinas-construction-machinery-exports-surge-33-4-in-early-2026/

8 HAUTO, Annual Report 2025

9 WAWI, Q1 2026

10 https://www.elibrary.imf.org/view/journals/002/2026/044/article-A001-en.xml?utm

12 https://www.imf.org/en/publications/weo/issues/2026/04/14/world-economic-outlook-april-2026