Deep Dive: Scorpio Tankers Inc. (Ticker symbol: STNG)

(published on Substack on 05 May 2026)

Dear fellow value investors,

Today’s company has a net cash position of USD 152 million and USD 767 million in available revolving credit facilities. From a financial health perspective, disciplined capital allocation and strategic pool ventures have created a fortress within the tanker segment of the shipping industry that can survive any downturn or crisis.

Let’s dive in.

Business overview

Scorpio Tankers Inc. was established in 2009 and became a publicly listed company on the NYSE in 2010 under the ticker symbol: STNG.

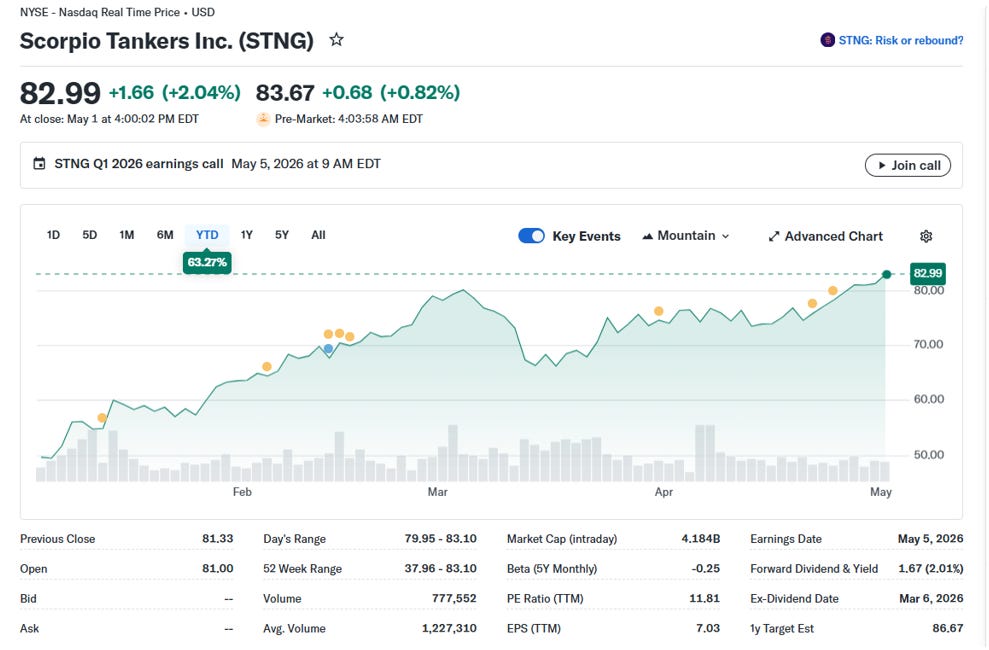

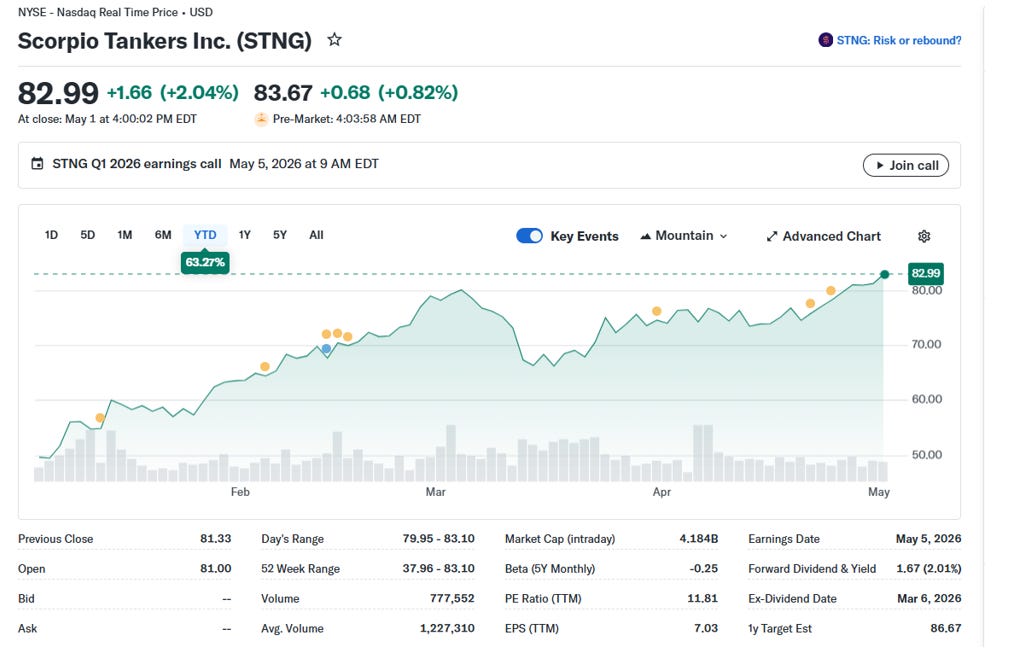

The company’s current capitalisation is 4.184 billion, and its current PE ratio is 11.81:

Source: Yahoo Finance

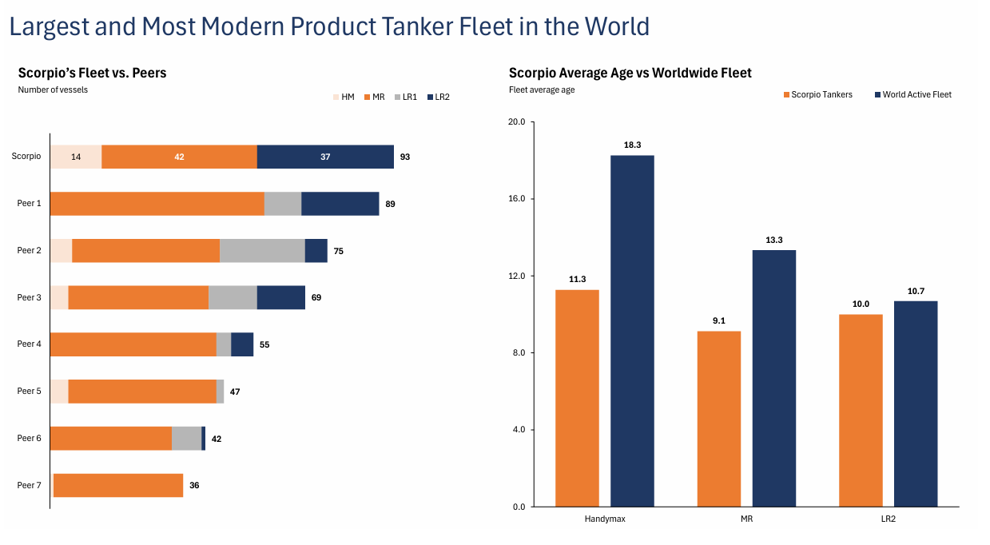

The company provides transportation of crude oil and clean petroleum products (CPP) globally and has, as of today, has 93 product tankers (1):

Source: Internal analysis based on STNG 2025 annual report

Scorpio Tankers Inc. operates in three major product tanker sub-segments:

· LR2 (Long Range 2) tankers that are similar to Aframax with a deadweight of 80,000-120,000 mt, but thanks to internal tank coating, can load crude oil cargoes. Aframax tankers usually have uncoated or partially coated internal tanks. As per the usual industry standards, Aframax tankers cannot load CPP, whereas LR2 can load both CPP and crude oil cargoes. In other words, LR2 tankers have an advantage over Aframax tankers due to the “switchover” ability of the former. This sub-segment usually trades in the Arabian Gulf, Mediterranean region, Europe and Asia. Primary cargoes of these tankers are diesel and naphtha (CPP).

· MR (Medium Range) tankers with 40,000-60,000 mt deadweight and their trading regions are the USG, Europe, the Arabian Gulf and Asia. This sub-segment transports diesel and gasoline cargoes. It is important to mention that 6 out of 42 MR tankers are 1B ice-class tankers.

· As mentioned above, the company has Handymax ice-class (1A and AB) tankers that usually trade in the Baltic and North Sea trading regions. Usual cargoes are diesel and fuel oil.

The weighted average of their fleet is 9.8 years.

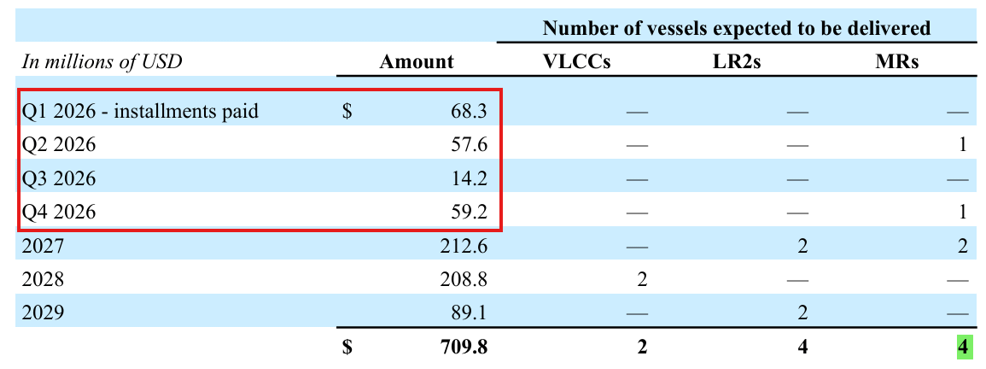

Apart from the current fleet, STNG also expects delivery of new tankers: 4 MRs, 4 LR2s and 2 VLCCs. The delivery of two MRs is scheduled for 1Q 2027 and two for 2Q 2027. Two LR2s are slated to be delivered in 3Q 2027, one in 3Q 2029 and one in 4Q 2029. The VLCCs are expected to be delivered in 3Q 2028 and 4Q 2028.

Recently, they closed the sales of older units at reasonable prices. In 2026, STNG sold three LR2 tankers, STI Lavender (2019 built), STI Goal (2016 built) and STI Gallantry (2016 built). In addition, the company closed this year, the sales of two 2015-built MR tankers (STI Seneca and STI Osceola) and one 2015-built LR2 (STI Solidarity). The closure of the sale deals is expected to be within the 1Q and 2Q 2026.

The company’s business model entails commercial pools, time and bareboat charters and spot market.

The commercial pools line of business implies that the company participates with other shipowners to operate and manage a large number of tankers, which provide customers with flexibility and a higher level of service. Apart from that, STNG and the trading company Mercuria Shipping (a shipping arm of Mercuria Energy) established in 2023 a pool called Mercury Pool (2), which enables STNG to also have access to the CPP cargoes of Mercuria Energy, thereby making the global utilisation of the STNG fleet higher. It is worth noting that the revenue from Commercial Pools is the biggest contributor to the company’s total revenue.

The company also uses the strategy of time and bareboat charters, which provides a steady cash flow. Usually, the timeframe of time charters is two to five years. It is worth noting that one MR tanker (STI Bosphorus, 2017-built) is on bareboat charter since Aug 2025 to August 2037.

And of course, they are present in the spot market to enhance the financial metrics by capturing the upside trends of the tanker market.

According to STNG (3), 72 vessels operate in Scorpio Pools, 14 tankers are on time charter, one tanker is on bareboat charter (as per above), and the rest of the fleet is engaged in spot market activities.

Their clients are top-tier players in the crude and refined petroleum products industry (1):

Source: Scorpio Tankers Inc., Capital Link Presentation, January 14, 2026

In conclusion, according to STNG (1), they have the largest and most modern product tanker fleet in the world:

Source: Scorpio Tankers Inc., Capital Link Presentation, January 14, 2026

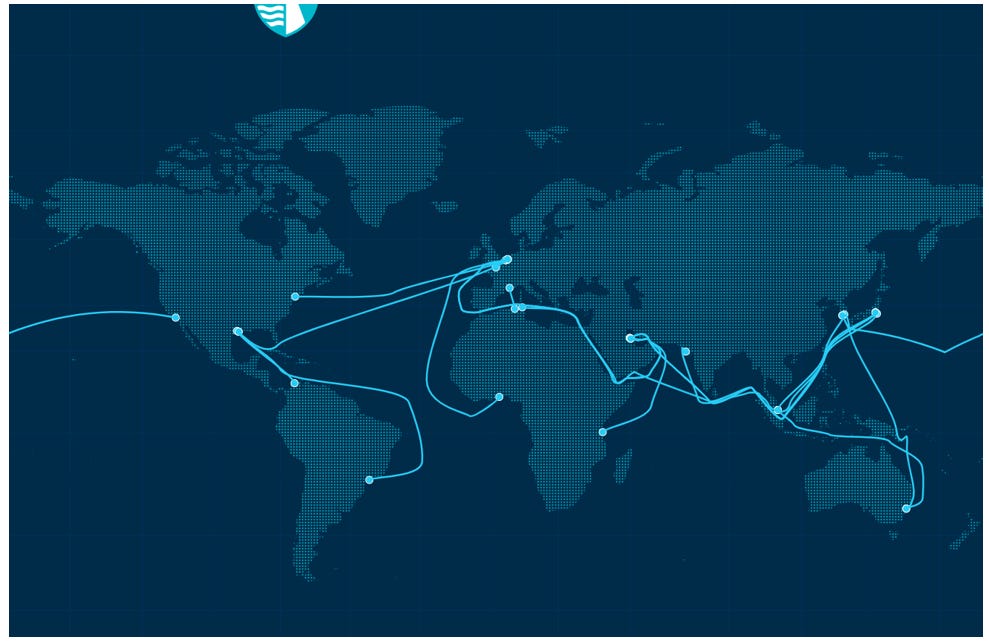

Please see below the global shipping routes of CPP petroleum products (LR2, Panamax, MR, Handymax (4)):

Source: Baltic Exchange

The company also likes to invest in other publicly listed shipping companies. For example, in 2024-2025, the company bought 12,277,698 common shares of DHT and exited the position by 31 December 2025, which led a profit of USD 20 million.

Now, let’s dive into the financial results.

Financials

Please see below the financials for the 2021-2025 period:

Internal analysis based on STNG reports

As you can see, apart from 2021, when the global tanker segment was still in a downturn due to the COVID-19 pandemic, the company has been overall profitable. Revenue, net income and FCF were positive. The capital expenditures will be related to the payments for vessels under construction:

Source: Scorpio Tankers Inc., Annual Report 2025

In addition to the above instalments in 2026, the company might also incur capital expenditures related to the drydocking. According to the company’s Q4 2025 Earnings Call (4), for the past 2 years, around 70 per cent of the STNG fleet has undergone drydocking, and the guidance is that the drydocking schedule in 2026 should be light.

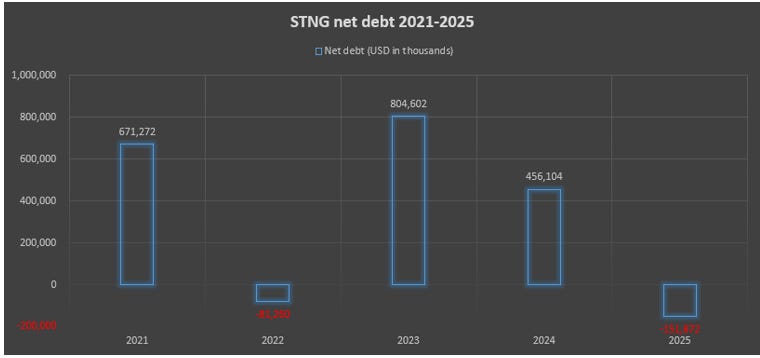

Let’s have a look at the net debt as of 31 December 2025:

Source: Internal analysis based on STNG annual reports

As you can see, the net debt is positive USD 152 million. It means that the company, as of 31 Dec 2025, holds USD 752 million in cash, while having a total debt of USD 600 million. In other words, the company can pay all its debt and still have a cash balance of USD 152 million. Effectively, we have a business that is in a net cash position and has a very low leverage.

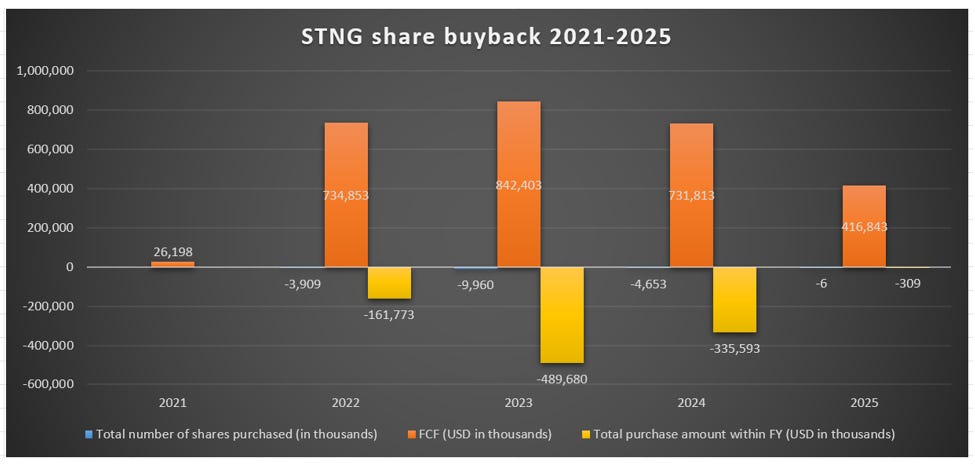

They have been implementing share buyback programs for the past few years:

Source: Internal analysis based on STNG annual reports

They also reward shareholders via dividend payouts. For instance, the company paid USD 1.67 per share for the FY2025.

Let’s look at the company’s cash and cash equivalents as of 31 Dec 2025:

Source: Scorpio Tankers Inc., Annual Report 2025

As mentioned above, the company is a financial fortress. Apart from that, according to the company’s Q4 FY2025 earnings call (5), the company has additional USD 767 million in revolving credit facilities. If we add both numbers, we get around USD 1.52 billion of cash.

Let’s have a look at shareholders’ equity:

Source: Scorpio Tankers Inc., Annual Report 2025

So, overall, we have a very strong business with the cash in hand and available credit facilities, which will help the company to weather the downturn and allocate capital properly, as they have been doing for the past few years.

What to expect in 2026?

As STNG is engaged in transporting mostly clean petroleum products (CPP) such as jet, naphtha, diesel and gasoline, we will focus on the fundamental factors related to these commodities and the CPP fleet. As mentioned, the company’s fleet does sometimes trade crude oil cargoes, but the company’s business model is primarily focused on the transportation of CPP cargoes.

Global refinery landscape

The CPP commodities are derived from the refining of crude oil. As of today, global refining is severely affected by the current events in the Middle East and the effective closure of the Strait of Hormuz.

We can see the trend of refinery closures in developed economies and the expansion of refining capacity in developing economies, such as in the Middle East, West Africa and Asian regions. The major reason for the closure lies in the economic aspects of running the refinery. It is either related to the financial losses, operational inefficiencies, investments to modernise it, etc.

Now, it is worth noting that according to S&P Global (6), the European refinery capacity has been reduced by approximately 2.9 million barrels per day since 2007. In 2025 alone, around 890kbd of refining capacity was closed around the world (7):

Source: Kpler

Since 2022, European countries have reduced the import of CPP from Russia and started to source clean petroleum products from export points where there is spare volume.

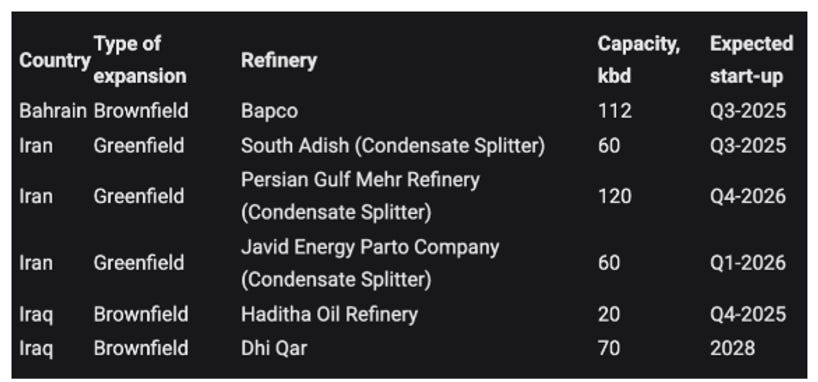

Please see the tables below with the expansion of oil refining capacity (7):

Middle East

Source: Kpler

Asia

Source: Kpler

Now, we also have Dos Bocas (Mexico) and Dangote (Nigeria) refineries that are slated to ramp up their throughput.

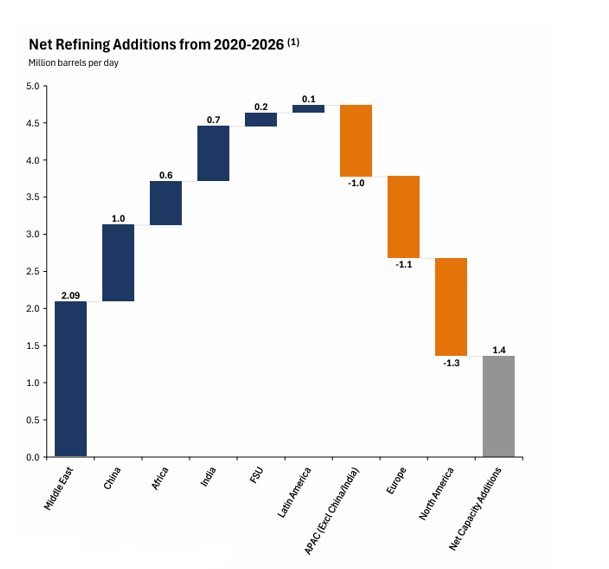

As per STNG (1), the net capacity addition is estimated to be around 1.4 mbd:

Source: Scorpio Tankers Inc., Capital Link Presentation, January 14, 2026

As you can see from the tables above, the distances to deliver petroleum products from points of expansion to points of consumption are lengthening, which increases the ton-mileage of transporting CPP. This, in turn, increases the timeframe of utilising the CPP tanker as voyages become longer. Let’s not forget that the current events in the Middle East have put on hold the safe passage via the Suez Canal and the Red Sea (from West of Suez to East of Suez and vice versa). Which in turn, also adds to the length of the voyage.

So, as you can see, we have a fundamental shift in the distances between the point of production of CPP and its consumption. Now, let’s have a look at the global CPP demand.

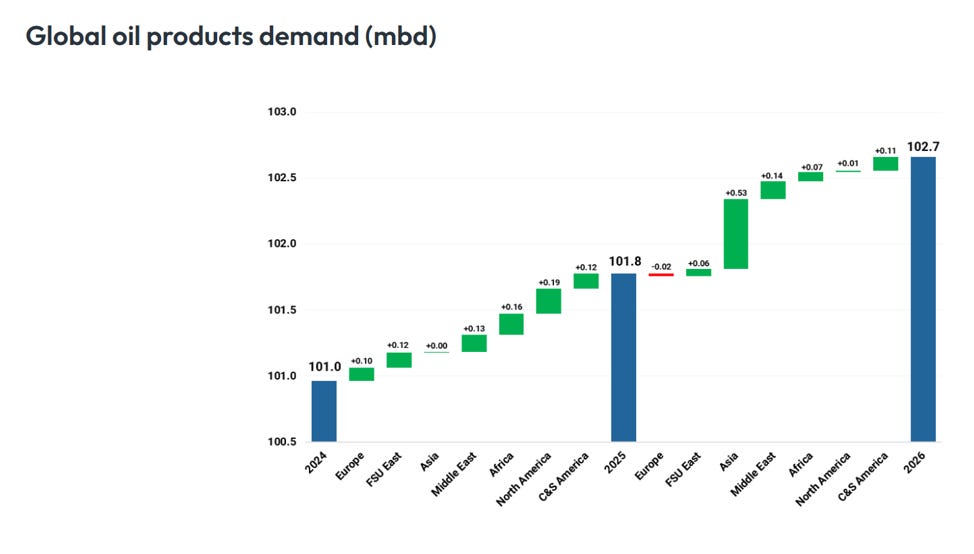

Global oil products demand

The global oil products demand is directly correlated with global crude oil demand.

According to Kpler (8), global oil products demand in 2026 is projected to grow by 0.8-0.9k mbd (million barrels per day) and reach 102.7 mbd versus 101.8 mbd in 2025:

Source: Kpler

As you can see, the demand in Asia, the Middle East, etc. are on a constructive trajectory, whereas the demand in Europe is expected to decrease by 0.02 mbd.

According to the STNG (1), we should expect the global CPP demand to increase in 2026:

Source: Scorpio Tankers Inc., Capital Link Presentation, January 14, 2026

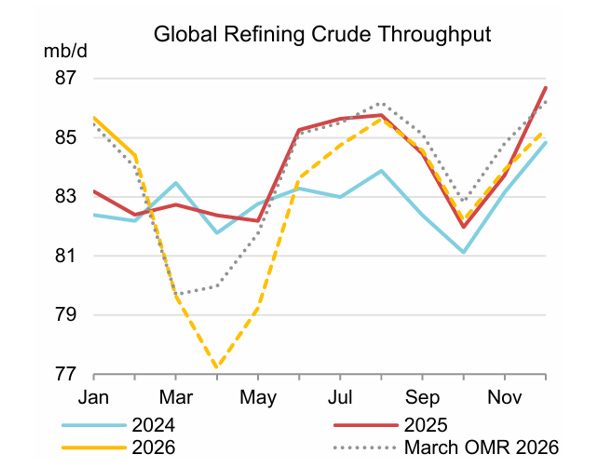

However, as mentioned above, the current situation in the Middle East and the effective closure of the Strait of Hormuz lowered the global throughput in 2026 (9):

Source: IEA

As you can see, the global crude oil refining throughput in Q2 2026 is slated to be around 79.5 mbd and is slated to return to pre-conflict levels.

We shall see how things evolve as a lot of puzzle pieces are currently moving.

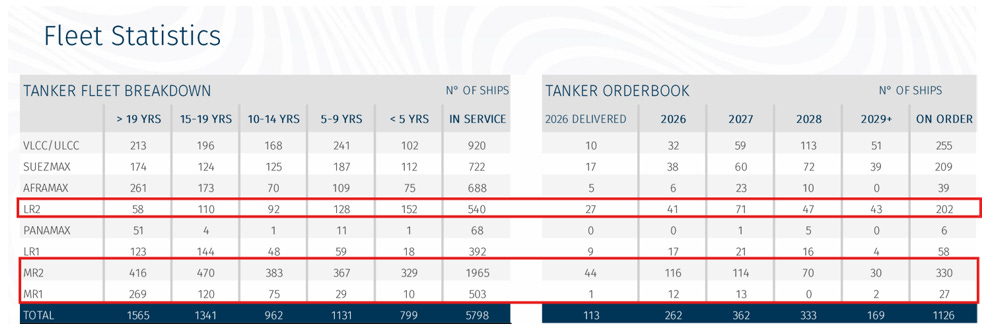

Global product tanker fleet

Let’s have a look at the current global product tanker fleet.

As per BRS (10), we have around 540 LR2s, 1,965 MR2s (in the fleet of STNG as MR) and 503 MR1s (in the fleet of STNG as Handymax) that are in service:

Source: BRS

Now, out of the mentioned numbers, around 168 LR2, 886 MR2 and 389 MR1 tankers are 15-19+ years old. And in 2026, we should expect 41 LR2 (27 have already been delivered), 116 MR2 (44 have already been delivered), and 12 Handymax (1 has already been delivered) tankers to be delivered.

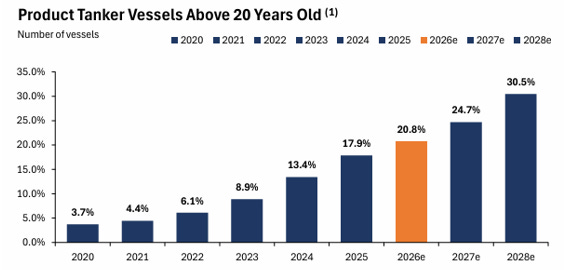

According to STNG (1), the global product tanker fleet that is above 20 years old in 2026 will reach 20.8 per cent, and this trend is slated to continue due to limited growth in the fleet:

Source: Scorpio Tankers Inc., Capital Link Presentation, January 14, 2026

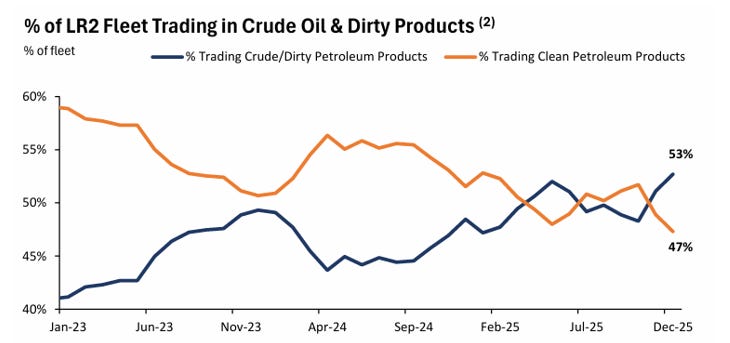

Also, it is worth noting that around 53 per cent of total LR2 tankers trade crude oil or DPP cargoes (1):

Source: Scorpio Tankers Inc., Capital Link Presentation, January 14, 2026

By looking at the current and delivery of the new product tankers, we can conclude that we have an ageing fleet and the limited product tanker fleet growth is one of the fundamental factors that should be beneficial to shipping companies that are engaged in CPP transportation business.

Risks

One of the major risks is related to the demand for clean petroleum products that STNG is engaged in. As these types of commodities are directly related to the GDP growth and are price sensitive, we, as value investors, shall bear in mind the risk associated with the slowdown in or lowered demand for CPP commodities. This will have a direct impact on STNG’s financial performance due to lowered daily earnings/TCE.

Another important risk is related to the price of CPP commodities. If the prices for CPP commodities are high, there might be a demand destruction, which may lead to lowered demand.

Stock valuation

Let’s work out the intrinsic value of STNG. We have the current fleet, and we have ordered vessels, which are slated to be delivered as per the above-mentioned timeframes. We should add them to the current fleet:

Source: Internal analysis

We get NAV per share USD 86.98. The NAV inputs are conservative in these terms in order to reduce the probability of error and apply the principle of a margin of safety. As Warren Buffett wrote in his 1993 shareholder letter: “It is better to be approximately right than precisely wrong”. And that’s why we use conservative inputs.

Let’s compare it to the current stock price of the company:

Source: Yahoo Finance

At the time of writing (May 4, 2026), the price was at USD 82.99 per share, and our NAV per share is USD 86.98. If we look at the upside of the share price versus the NAV per share, we have only 4.81 per cent of potential upside. From the value investing perspective, we are at the point where the risk increases and the reward dwindles.

According to various analysts, STNG’s 12-month target price is forecasted around USD 86.67-87.00 per share. So, we can conclude that the STNG business is fairly valued with limited upside.

However, one should definitely include the current company in its watchlist, as it’s a financial fortress and has a proven record of disciplined capital allocation. In addition, the fundamental factors laid out above should positively affect the company’s profitability. However, as of now, the company will be put on a waiting list until it offers a low-risk/high-reward option.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, don’t hesitate to get in touch with me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 Scorpio Tankers Inc., Capital Link Presentation, January 14, 2026

3 Scorpio Tankers Inc., Annual Report 2025

4 https://www.balticexchange.com/en/data-services/routes.html

5 Scorpio Tankers Inc., Q4 FY2025 Earnings Presentation Conference Call

7 https://www.kpler.com/blog/refinery-status-monthly---september

8 https://www.kpler.com/blog/oil-products-demand-outlook-for-2025-and-2026-update-0plke

10 BRS Weekly Tanker Newsletter, Apr 27, 2026