Deep Dive: Tsakos Energy Navigation Limited (Ticker symbol: TEN)

(published on Substack on 21 Apr 2026)

Business overview

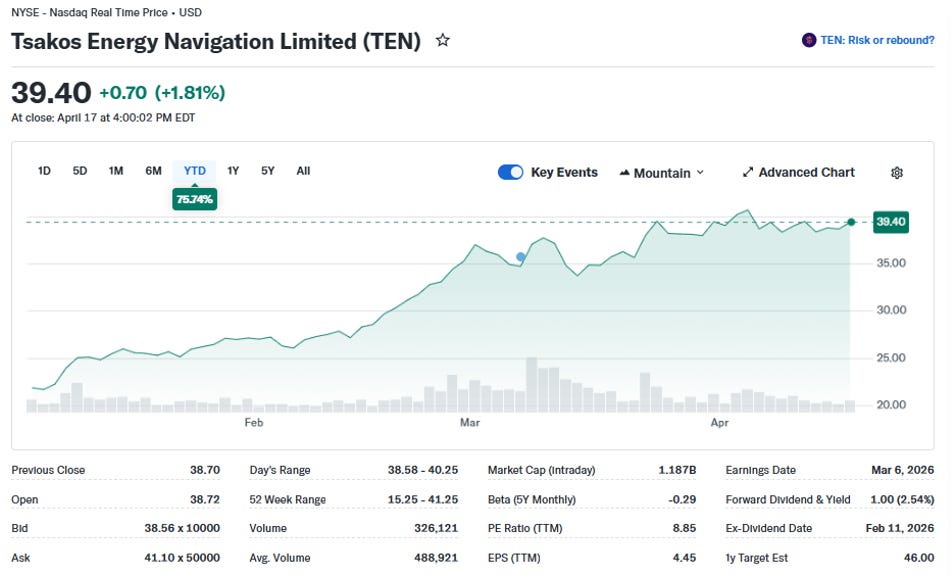

The company’s current market capitalisation is USD 1.187 billion, and the P/E ratio is 8.85:

Source: Yahoo Finance

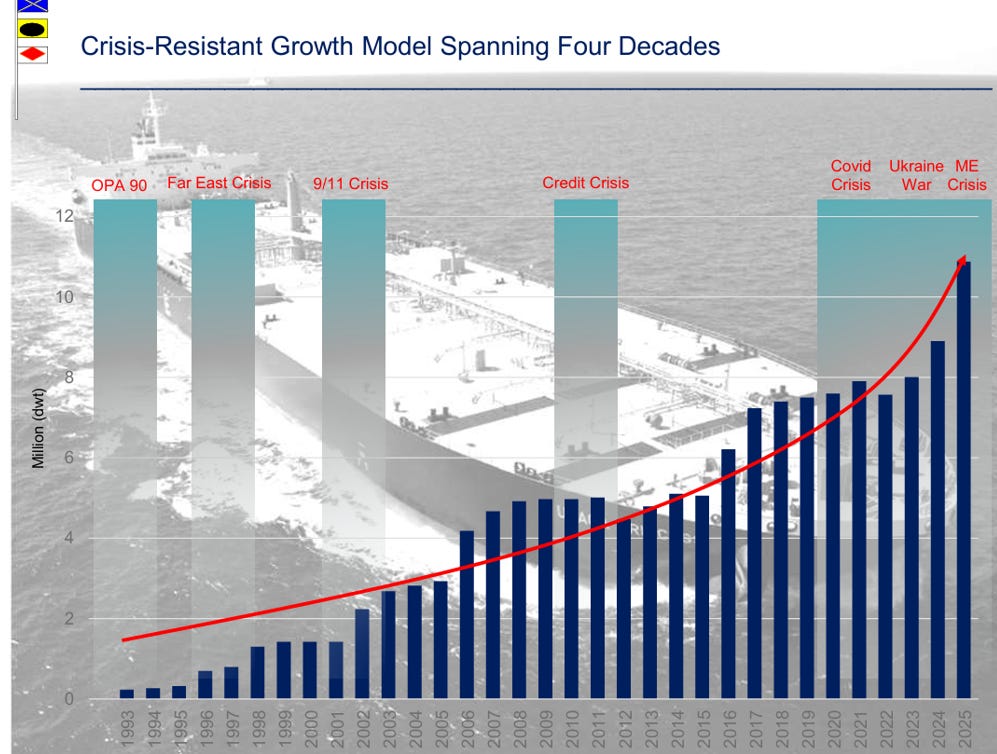

The company was established in 1993 and became publicly listed on the NYSE in 2002. So, the company has seen various crises along the way and survived, which is a good sign.

Source: Tsakos Energy Navigation Limited

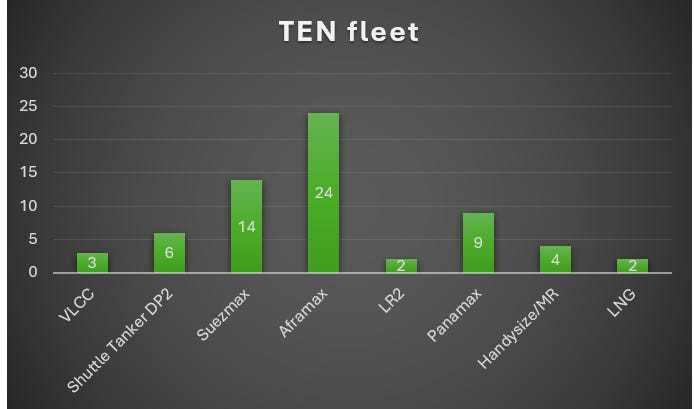

The company has a very diversified portfolio of tankers and LNG carriers. In total, the company operates 62 tankers and 2 LNG carriers:

Source: Internal analysis based on TEN reports

It is worth noting that out of the total fleet, 4 vessels have sale and leaseback financial arrangements.

The company expects deliveries of 3 new VLCCs, 5 new Panamax vessels and 1 LNG carrier.

The model for the company’s business strategy is to fix most of its vessels on time charters at a fixed rate or on profit-sharing arrangements. They have little exposure to the spot market, thereby creating a steady cash flow. The downside is that they might miss the market’s potential upside, but they are also hedged against the downside. This approach shows a conservative business model.

Their major clients are top-tier blue-chip companies/customers that operate in the crude oil and LNG commodity industries. Their biggest client is Exxon Mobil (1).

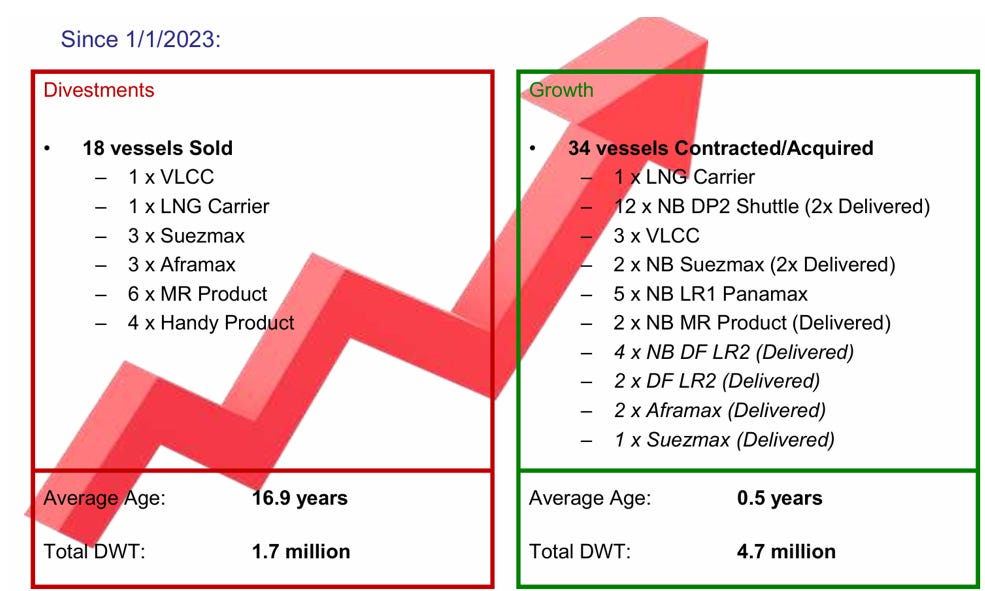

Since 2023, the company has been divesting older units and adding new vessels to its portfolio (1):

Source: Internal analysis based on TEN reports

The company’s average fleet age is 10.1 years as of 31 December 2025.

Let’s have a look at how they are doing financially.

Financials

The company, as mentioned above, has been resilient since its inception and enlistment. For the last 5 years, the company has been profitable (except for the 2020-2021 COVID-19 pandemic period):

Source: Internal analysis based on TEN reports

The company has been investing in the acquisition of new vessels and updating its fleet, hence the negative FCF. The stockholders’ equity stands as of 31 December 2025 at USD 1.8 billion, which is good for shareholders.

The company has not made any share buybacks but instead has been returning dividends to its shareholders as a reward.

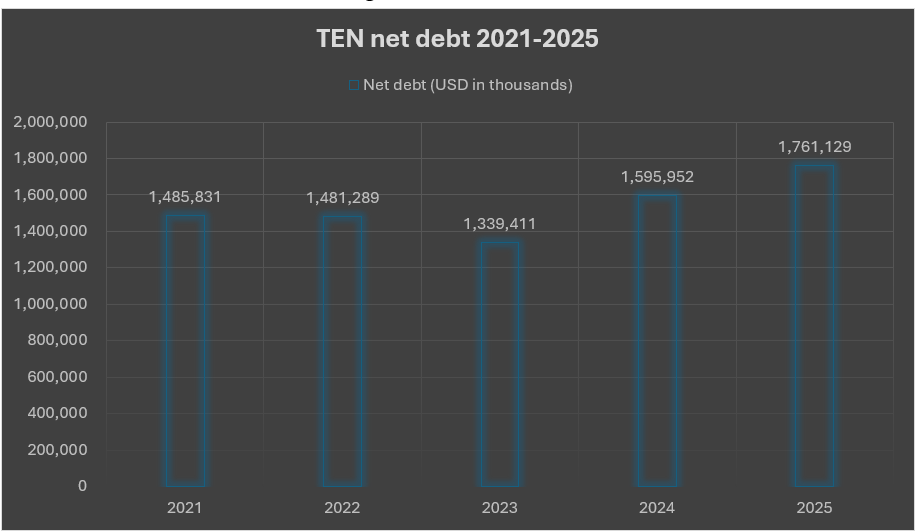

Now, the net debt has been increasing since 2023:

Source: Internal analysis based on TEN reports

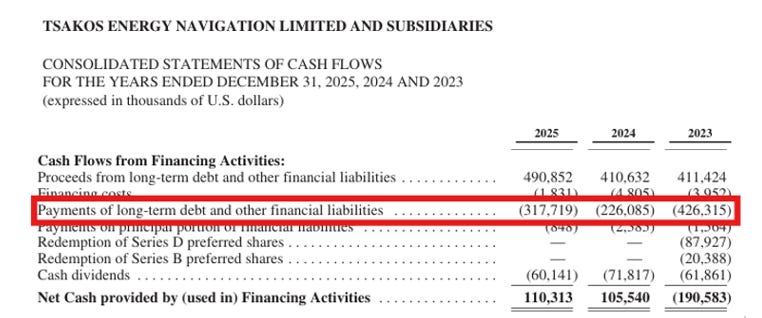

But the above shouldn’t be a big concern as this net debt is secured against the assets (i.e. the vessels), so it is manageable. The management has been repaying the debt too:

Source: Tsakos Energy Navigation Limited

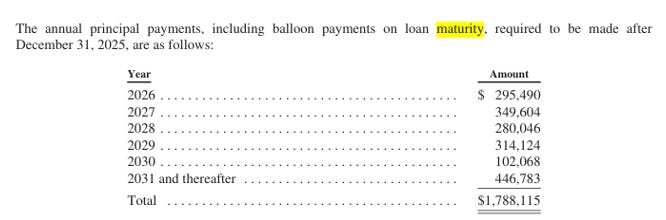

They have maturing loans in the upcoming years:

Source: Tsakos Energy Navigation Limited

Overall, the company has a strong balance sheet and manageable debt.

What to expect in 2026?

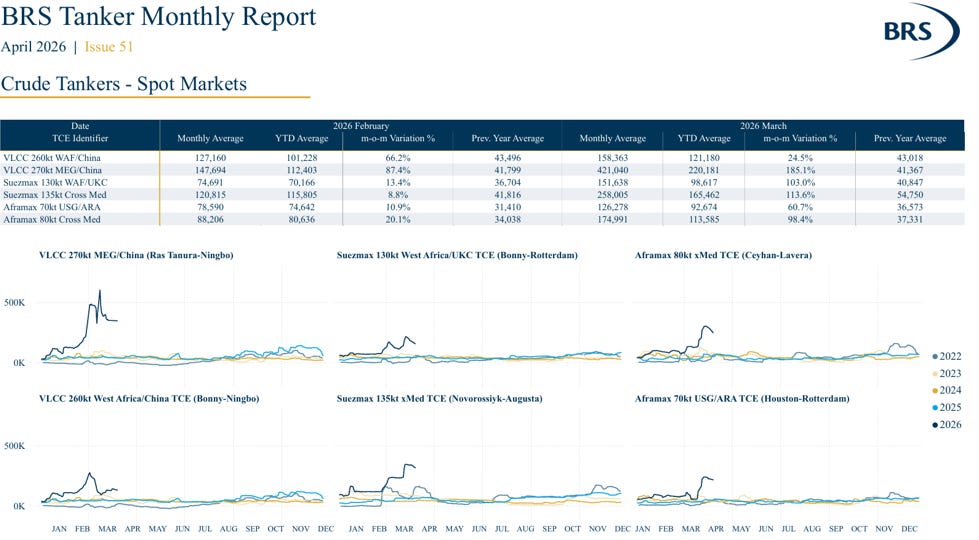

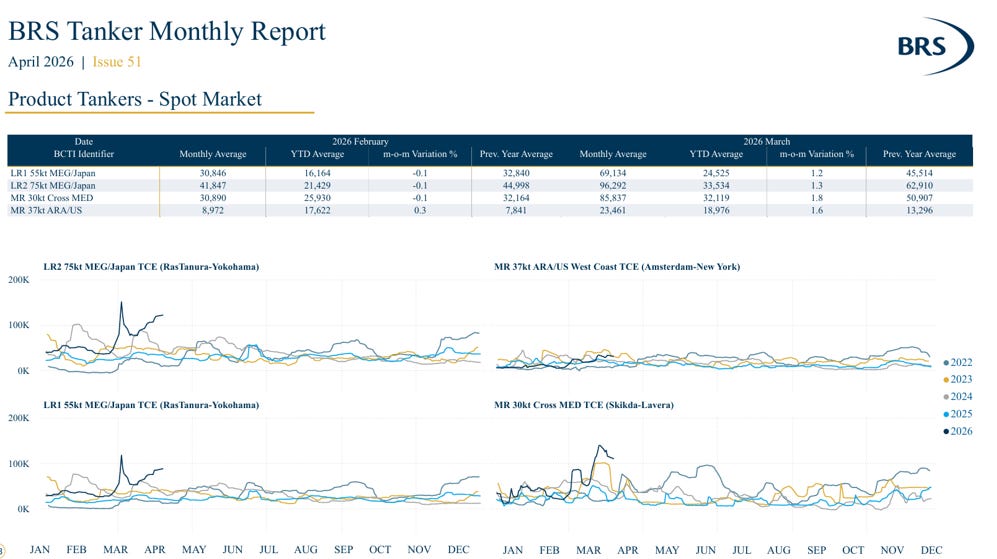

The year 2026 started very bullish for the tanker markets due to recent events in Venezuela and the Middle East. The TCE of VLCC, Suezmax, Aframax and Handysize/MR segments soared (2):

Source: BRS Tanker Monthly Report

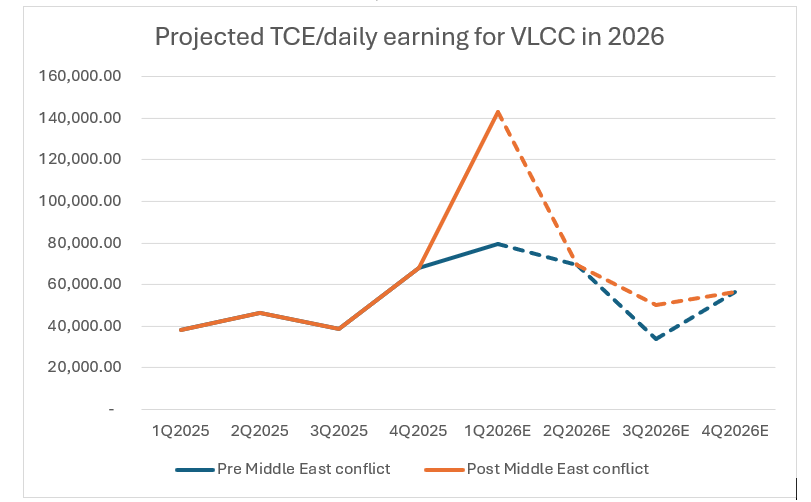

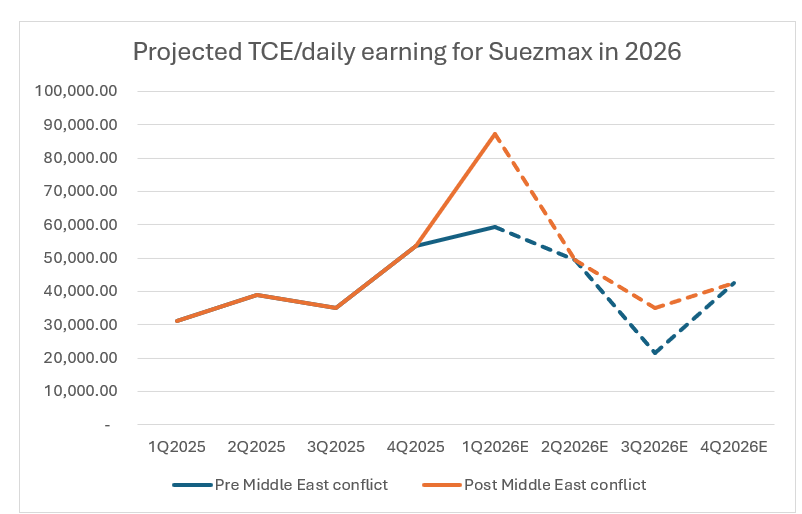

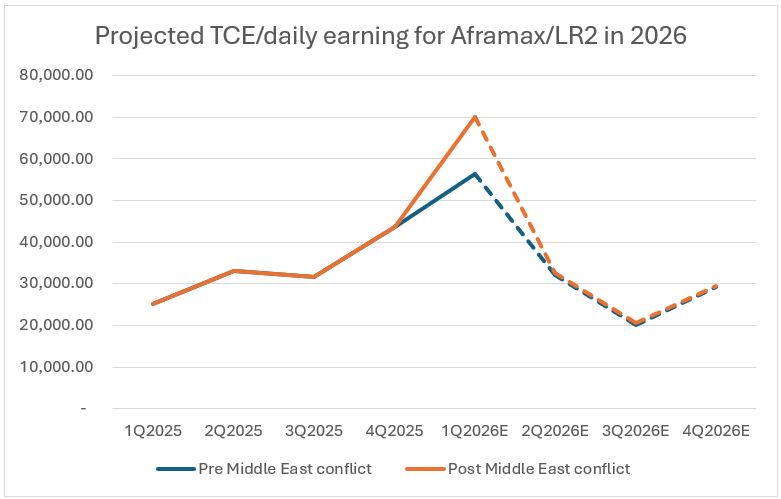

However, according to BRS, the TCE is slated to fall by 3Q 2026 based on the forward curve (FFA – Freight Forward Agreement). If we look at the estimations of internal analysis, we can see that the earnings are projected to decline by 3Q 2026 (for a deeper analysis, please read the post “Outlook on the tanker market in 2026” dated 13 Feb 2026):

Source: Internal analysis

We shall see how things evolve going forward.

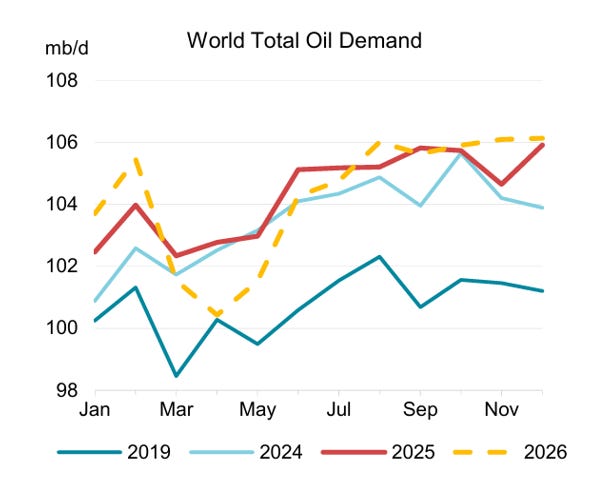

According to TEN (1), the demand for crude oil is slated to stay strong, especially in Asian regions. IEA (3) projects that the global oil demand in 2026 should be around 104-105 million barrels per day:

Source: IEA, Oil Market Report – April 2026

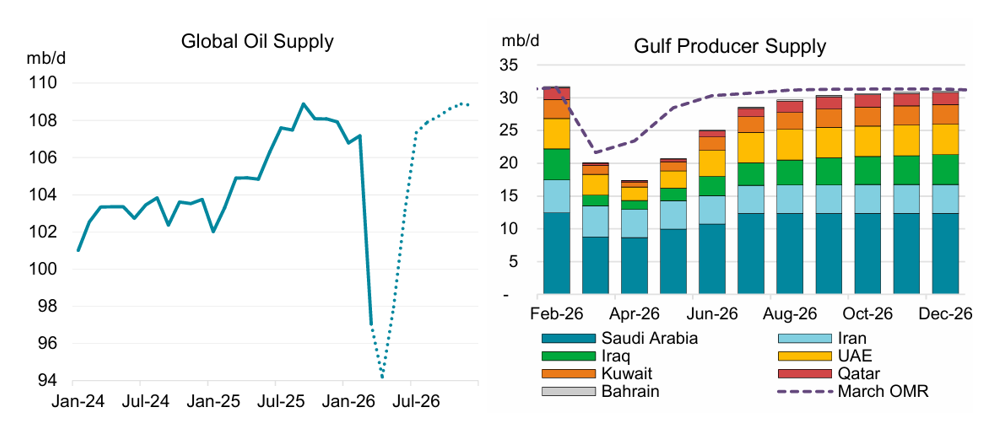

If we look at the global oil supply, the market lost 10.1 million barrels per day in March 2026 and made up 97 million barrels per day. However, the volumes are slated to return to 106-107 million barrels per day by May-Jun 2026 (3):

Source: IEA, Oil Market Report – April 2026

As of now, it is very difficult to pinpoint and estimate when the missing volumes are going to return to the market due to many moving parts and news that comes in. As of now, we have to take a wait-and-see stance to better evaluate the risks versus the rewards and make a better decision on the basis of fundamental factors.

Let’s have a look at the global GDP forecast, as it’s an important aspect of the global economy, which affects the tanker sector of the shipping industry. According to the IMF (4), the global GDP in 2026 is projected at 3.2 per cent, which is the same as in 2025 (5).

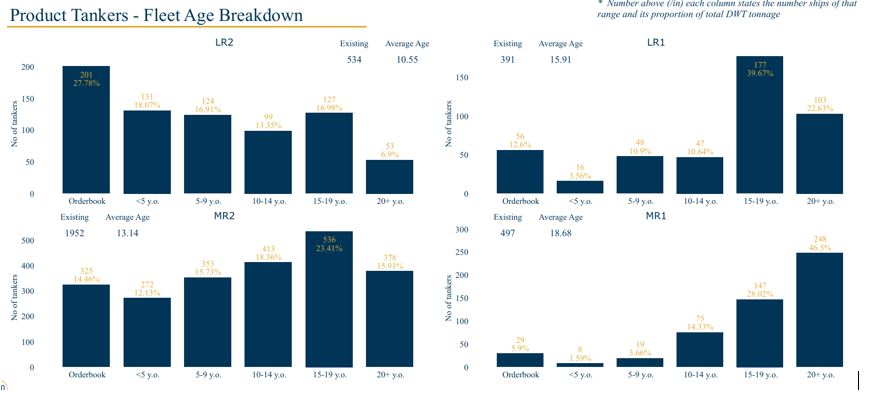

In terms of the current global tanker fleet, we have the following picture (2):

Source: BRS Tanker Monthly Report

The ageing fleet is evident in the VLCC, Suezmax and Aframax segments of the global tanker fleet. Namely, around 16.43 per cent and 20.40 per cent of VLCC are 20+ and 15-19 years old, respectively. The Suezmax segment has the following picture: 17.54 per cent and 17.68 per cent are 20+ and 15-19 years old, respectively. The Aframax segment has an even higher rate of older units: 32.35 per cent and 29.59 per cent are 20+ and 15-19 years old, respectively.

In terms of the delivery of new vessels, we should expect 10 new VLCC, 12 new Suezmax and 5 new Aframax vessels in 2026, and as of today, we have 13 vessels demolished in 2026. So, the growth rate of the delivery of the new units is limited.

So, we have a constructive picture in terms of the demand for and supply of crude oil, the ageing tanker fleet and the limited delivery of new vessels.

Now, let’s have a look at the risks.

Risks

The obvious risk is related to the current situation in the Middle East and the effective closure of the Strait of Hormuz. As Asia is the major consumer and locomotive of the global crude oil demand, the prolonged level of high crude oil prices might have a detrimental effect on its economy. In 2025, Asia’s demand was at 39 million barrels per day, and most of its imports came from the Middle East. So, one shall bear in mind this important risk.

Another risk is related to a possible shift of crude oil-importing countries to the consumption of coal instead of crude oil. There is a relationship between the high crude oil prices, and countries which are sensitive to prices start looking for a cheaper alternative. According to the paper of N. Zamani called “The Relationship between Crude Oil and Coal Markets: A New Approach” (6), the coal consumption is increasing when the crude oil prices become high and expensive for crude oil-importing countries.

The above two major risks can lead to lower imports of crude oil and lower daily earnings/TCE, thereby affecting the subject company’s revenue, net income and FCF.

Stock valuation

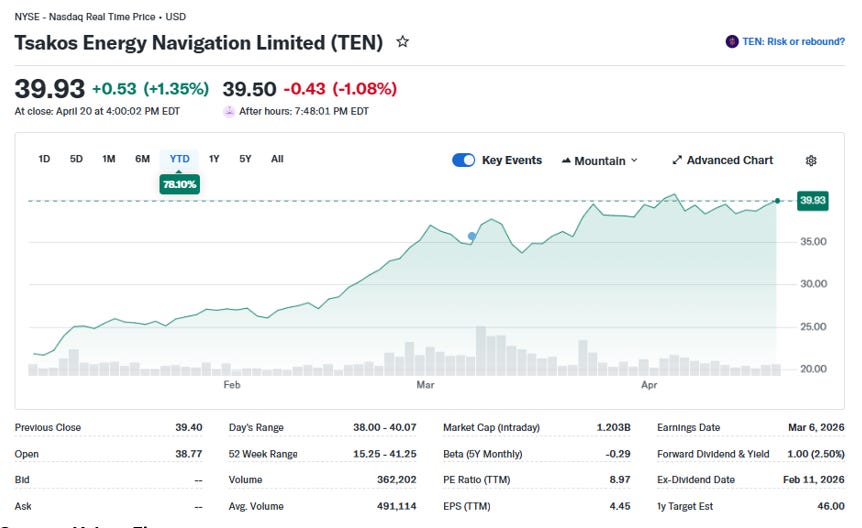

Now, let’s have a look at the stock valuation. At the time of writing, the stock closed on 20 Apr 2026 at USD 39.93 per share:

Source: Yahoo Finance

The stock is up 78.10 per cent YTD due to the recent and current developments in the Middle East and the Strait of Hormuz.

Let’s evaluate if the current price is high, fairly valued or undervalued. First, we shall calculate the NAV (net asset value):

Source: Internal analysis

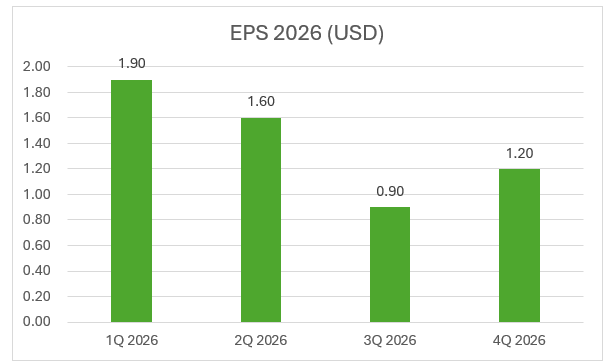

The next step will be to estimate the EPS for 2026. As per the below internal analysis, the EPS for 2026 shall be around USD 5.60:

Source: Internal analysis

If we take the above projected conservative EPS and multiply it by the P/E ratio of 7.50, we get around USD 42.00 per share. If we look at analysts’ 12-month price targets, they range from USD 42 to USD 45 per share. Now, based on the current price of USD 39.93 (as of COB 20 Apr 2026), we have an upside in the range of 5.18-12.70 per cent.

However, if we want to play it a bit more conservatively with a margin of safety, we should put the P/E ratio at 6.5 (average P/E ratio of 2025) and multiply it by the EPS of USD 5.60, we shall come to USD 36.40 per share, thereby increasing our reward and reducing our risk.

For value investors, as of today, the stock price offers limited upside in terms of rewards, despite strong fundamental factors such as the crude oil demand and the ageing fleet. This, however, has already been priced in, which leads to increased risk and reduced reward. We, as value investors, like low-risk / high-reward options.

Hence, as of now, from a value perspective, we shall put it in the list of potential purchases once the rewards outweigh the risks.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 TEN, Ltd Q4 & 12mo 2025 Earnings Presentation, March 6, 2026

2 BRS, Monthly Tanker Report, April 2026, Issue 51

3 IEA, Oil Market Report – April 2026

4 International Monetary Fund, Global Economy in the Shadow of War, April 2026

5 https://www.statista.com/statistics/273951/growth-of-the-global-gross-domestic-product-gdp/

6https://www.researchgate.net/publication/309670991_The_Relationship_between_Crude_Oil_and_Coal_Markets_A_New_Approach