Deep Dive: ZIM Integrated Shipping (ticker symbol: ZIM)

(published on Substack on 20 Mar 2026)

Dear fellow value investors,

In this post, we will discuss the company ZIM Integrated Shipping (ticker symbol: ZIM), as it will potentially merge with Hapag-Lloyd Aktiengesellschaft (ticker symbol: HLAG.DE). The proposed cash offer to ZIM shareholders is at USD 35.00 per share (on 18 Mar 2026, the stock of ZIM closed at USD 27.14 per share, which offers around 28.96 per cent upside if the merger goes through). However, apart from the mentioned reward, there might also be risks for value investors that we are going to look into today.

Let’s discuss the company ZIM Integrated Shipping.

Business overview

The company ZIM Integrated Shipping operates in the container shipping business and has 115 container vessels and 13 vehicle transport vessels (in total 128 vessels: 16 fully owned and 112 chartered in) in its fleet. According to the company (1), the average size of their fleet is 6,068 TEUs, and most of the vessels are chartered-in (i.e. they leased the vessels from third parties and manage these vessels on their behalf).

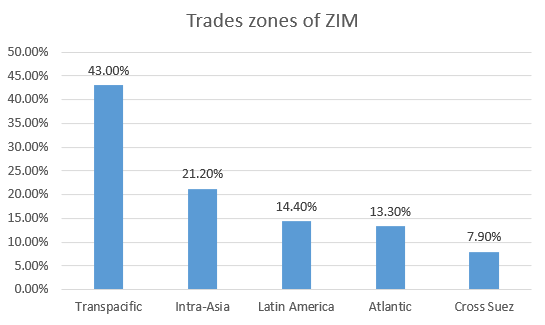

Most of their liners operate in five global trade zones:

Source: Internal analysis based on ZIM reports

The company has an 80-plus-year history and a presence in more than 90 countries.

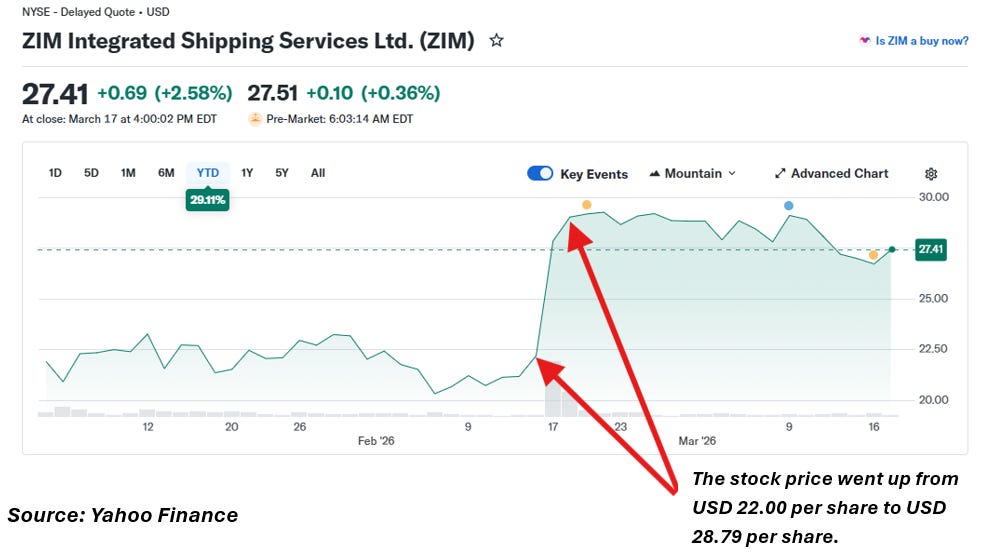

The company’s market capitalisation is around USD 3.302 billion with a P/E ratio of 3.30:

Source: Yahoo Finance

(The arrows above are related to the jump of the stock price of ZIM once the official offer price of USD 35.00 per share that Hapag-Lloyd Aktiengesellschaft proposed became publicly available.

The company became publicly listed in 2021, and before that, the majority (48.6 per cent) was owned by Israel Corporation (i.e., through a spin-off company named Kenon Holdings).

The company has been renewing its fleet by issuing new shares (see the Financial Statements below). It is worth noting that the State of Israel owns one Special State Share, which will be important in the analysis below.

Let’s have a look at the financials.

Financials

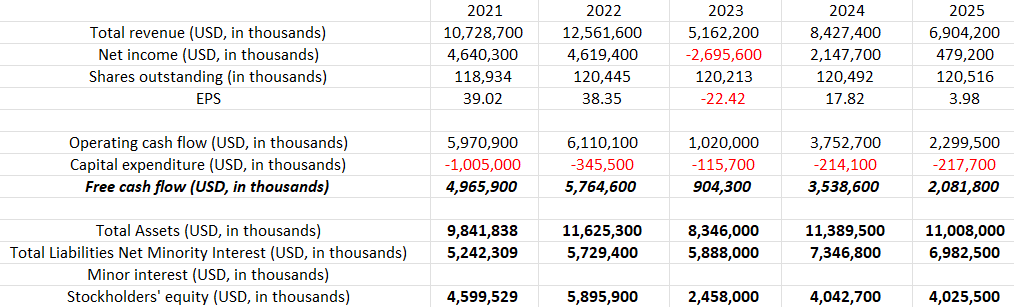

The company has been profitable in terms of revenues, net income and FCF since 2021, with a small bump in net income in 2023:

Source: Internal analysis based on ZIM reports

The capital expenditure (related to the acquisitions of new liners) since 2021 has been under control, enabling the company to renew its fleet.

Revenue, net income and FCF are lower compared to 2024, mostly related to the reduced freight rates and the decline in the carried volume. In 2025, the average container freight rates decreased by 17.80 per cent. The company’s revenue, net income, and TEU transported were 18.10 per cent, 7 per cent, and 2.3 per cent lower than in 2024, respectively. As mentioned in the post “Outlook on container sector in 2026” dated 24 February 2026, the delivery of new container liners has already started to weigh on the container freight rates in 2025. As per the analysis, this trend should continue in 2026 and onwards. However, the prolonged conflict in the Middle East should offset the above trend by keeping container rates upwards. The above is illustrated below:

Source: Trading Economics

As mentioned above, the company has been issuing shares to finance its vessel acquisitions, and the number of outstanding shares increased from 118 million in 2021 to 120 million in 2025.

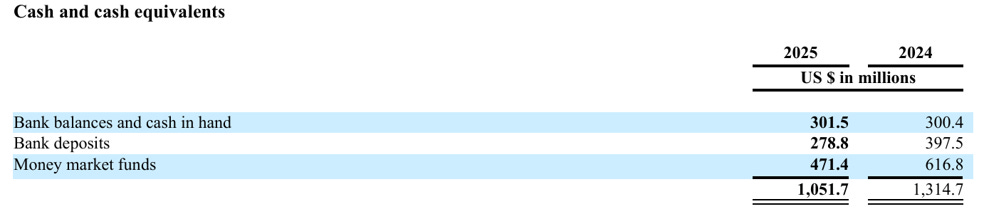

The company has a strong balance sheet with USD 4 billion in stockholders’ equity. As of 31 December 2025, ZIM held USD 1 billion of cash and cash equivalents:

Source: ZIM Integrated Shipping, Annual Report 2025

From a financial perspective, the company can be considered healthy.

Let’s look at what we have as of today related to the merger.

What to expect in 2026?

According to the company’s management, the merger with Hapag-Lloyd Aktiengesellschaft is expected to be completed by the end of 2026.

So, as of today, we have the following picture at hand:

1. Approval of the Board of Directors of Hapag-Lloyd Aktiengesellschaft to offer a cash payment of USD 35.00 per share to shareholders of ZIM Integrated Shipping; and

2. Approval of the Board of Directors of ZIM Integrated Shipping to accept the aforementioned cash offer.

But we have certain procedures that are still outstanding:

1. The approval of the merger and cash offer by the shareholders of ZIM is scheduled for 30th April 2026.

2. The approval of the State of Israel (Special State Share); and

3. The approval of various regulatory institutions.

If the merger does not take place by February 17, 2027, or if it is extended until June 30, 2027, either party may, under certain circumstances, choose not to proceed with the merger.

Let’s dive into the risks as one of the important aspects of value investing.

Risks

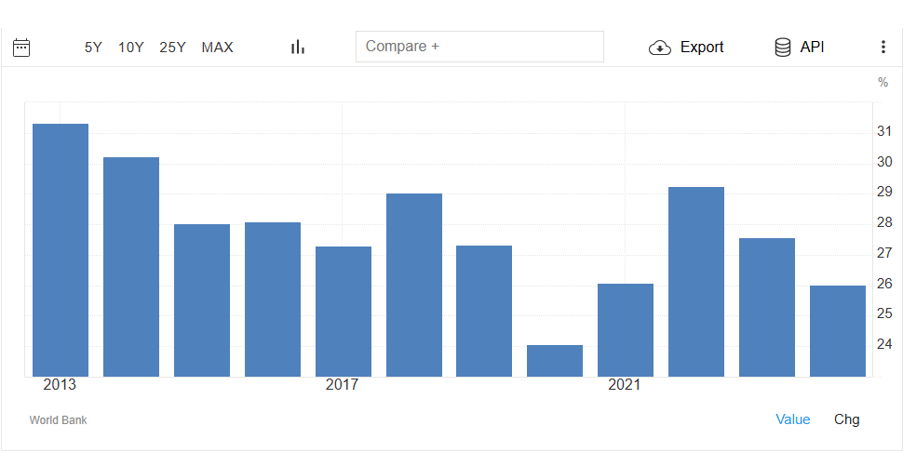

One of the major risks that the current merger is facing is the situation in the Middle East, and it is worth mentioning that ZIM used to be a national liner before becoming a publicly listed company, and Israel’s reliance on imported goods is around 26.02 per cent (1):

Source: Trading Economics

According to the Special Share requirements, the company ZIM is obliged to own a minimum of 11 vessels, not chartered-in (2). Hapag-Lloyd AG announced the allocation of 16 vessels to New Zim (the new entity of Hapag-Lloyd in Israel, if the merger succeeds) to meet this requirement (3). However, it is still at the discretion of the Special State Shareholder (i.e. the State of Israel) to assess if this construction will be acceptable.

The second risk is related to the fact that if the merger does not take place, the stock price of ZIM should go back to the fundamental factors (for a better understanding of the risks, please read the post “Outlook on container sector in 2026” dated 24 February 2026), especially due to the delivery of new container liners, which should put pressure on the container rates. However, as mentioned above, the aforementioned should be offset by the current situation in the Middle East.

To buy or not to buy?

We have a clear price target of USD 35.00 per share for ZIM stock, and it has been approved unanimously by the Board of Directors of both companies. By looking at the price closure as of 18 March 2026 (USD 27.14 per share), there is a potential upside of 28.96 per cent:

Source: ZIM Integrated Shipping

I do strongly believe that both parties (ZIM Integrated Shipping and Hapag-Lloyd AG) have strong intentions to make the merger happen and will do everything in their power to finalise the deal.

And by staying open-minded to various value investing opportunities, like the one discussed in this post, we can compound our assets throughout the year. As our main goal as value investors is to protect and compound our capital by looking at low-risk/high-reward options.

But as I mentioned before, it is up to you, my fellow value investors, to decide how the position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 https://tradingeconomics.com/israel/imports-of-goods-and-services-percent-of-gdp-wb-data.html

2 https://www.zim.com/assets/13ol5cyt/2020-11-30-notice-of-special-general-meeting-of-shareholders-22-december-2020.pdf

3 https://www.hapag-lloyd.com/en/company/press/releases/2026/02/hapag-lloyd-signs-merger-agreement-with-zim.html?msockid=2b1ef5403c5568fe0b80e3fe3d4d69df