Outlook on the LNG sector in 2026

How shall we, as value investors, navigate these uncharted waters?

(published on Substack on 13 Mar 2026)

Dear Value Investors,

Today’s topic will be devoted to the LNG sector of the shipping industry. It is worth noting that since the recent events in the Middle East, tanker, LPG and LNG sectors of the shipping industry have been exuberant (I will write updated posts for tanker and LPG sectors once we have a better and clearer picture), and it has been reflected in the stock prices of the publicly listed companies that are engaged in the mentioned sectors and have operational fleets.

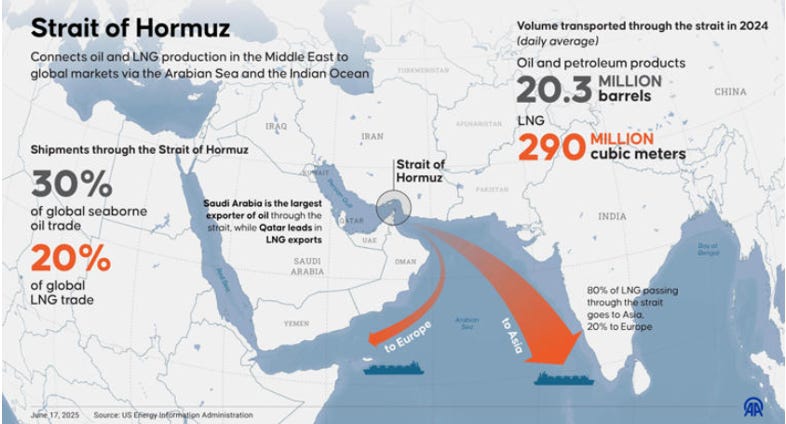

The key to the above lies in the fact that 30 per cent of the global seaborne oil trade and 20 per cent of global LNG trade pass through the Hormuz Strait:

Source: MSN

On a sidenote: LNG (liquefied natural gas) is one of the important commodities that support the economy of the importing countries. Namely, LNG is used to generate electricity, for heating of industrial and residential sectors, and for industrial production. LNG as a commodity is being carried on an LNG carrier and is cooled to -162°C to condense the gas into a liquid.

Supply and demand of LNG

There are three major supplying countries of LNG in the world: the USA, Qatar and Australia and recently Qatar announced that it will halt the output of LNG due to the shipping passage halt in the Hormuz Strait (1). By declaring force majeure, Qatar removed around 20 per cent of its LNG supply to Europe and predominantly to Asia.

So we have the following major trading routes of LNG:

1. US – Asia (via the Panama Canal);

2. US – Asia (via the Cape of Good Hope);

3. US – Europe;

4. Australia – Asia; and

5. Middle East – Asia.

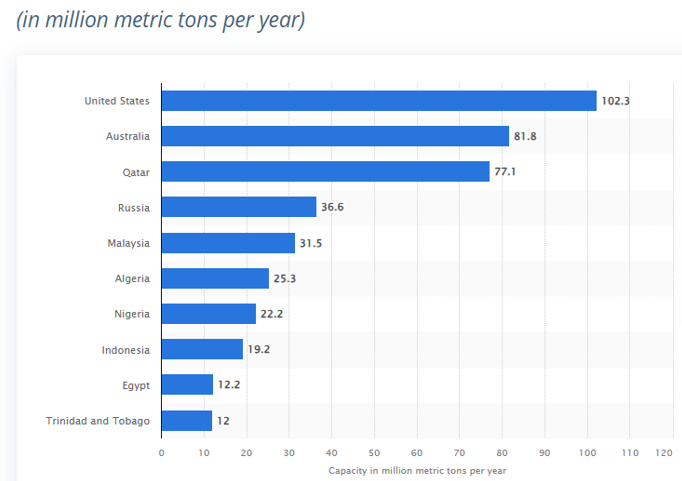

According to Statista (2), the top 3 leading countries in the world to supply LNG are the United States, Australia and Qatar:

Source: Statista

With Qatar currently being off the list and as per their information, it will take weeks (8) to restore the production, other suppliers will have to increase their production and export capacity. As of now, we have to wait for a clearer picture as there are too many moving parts.

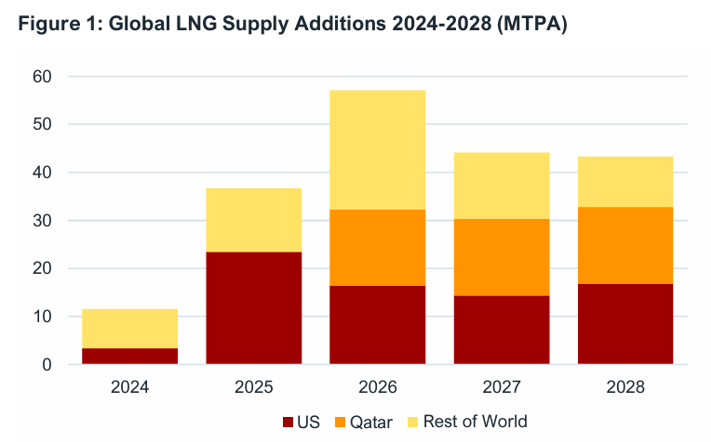

Before the events in the Middle East, the IEEFA (Institute for Energy Economics and Financial Analysis) predicted that the biggest additions to LNG supply would come from the rest of the world, along with the USA and Qatar (3):

Source: IEEFA

In 2025, the LNG supply capacities rose the most in North America, and the global LNG supply rose by almost 7 per cent (4). However, regarding the increase in supply capacity from Qatar, we have to see how the situation evolves in the Middle East. With 77 million tons per annum of supply being out, we have to see what their plans will be once the production at Ras Lafan facilities is operational again. It is worth noting that Qatar was planning (pre-outage) to expand the North Field East and North Field South by 32 mtpa and 16 mtpa (5).

For now, the expected additions of the LNG supply shall come from Canada (Canada West), USA (Golden Pass T1 and T2, Corpus Christi T5 and T7, Louisiana), Australia North (Darwin and Ichthys), Australia West (Pluto T3), Qatar (to be advised), Russia (Yamal East), Congo and Mexico (6).

Now, if we look at the demand, there is a projection that the global demand for LNG should be higher in 2026 than in 2025. And the major drivers of this demand in Asia will be China and India. Namely, Asian demand for LNG will be 10 per cent higher in 2026 than in 2025 (7). According to ADI Analytics (7), Asian importers are investing in the expansion of their import facilities. For instance, Vietnam is investing in the FSRUs (floating storage and regasification units) to store offshore the imported LNG volumes.

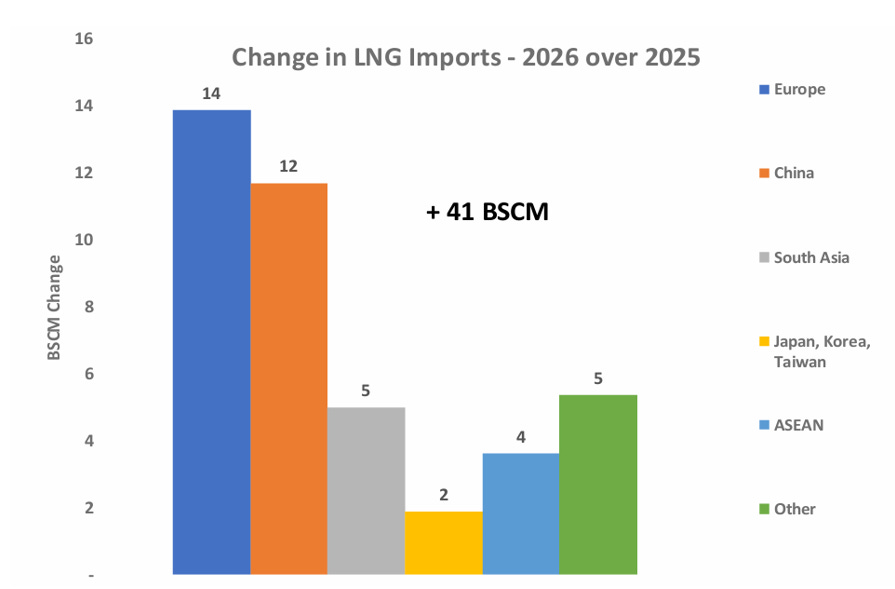

Europe will also be an important importer of LNG, with demand projected to grow by around 5 per cent (vs 2025), especially to refill the storage and replace gas supplied by Russia via pipelines. According to the Oxford Institute for Energy Studies (6), the increase in LNG imports in 2026 versus 2025 shall be by 41 bscm (billion standard cubic metres), and the major drivers will be Europe and Asia:

Source: Oxford Institute for Energy Studies

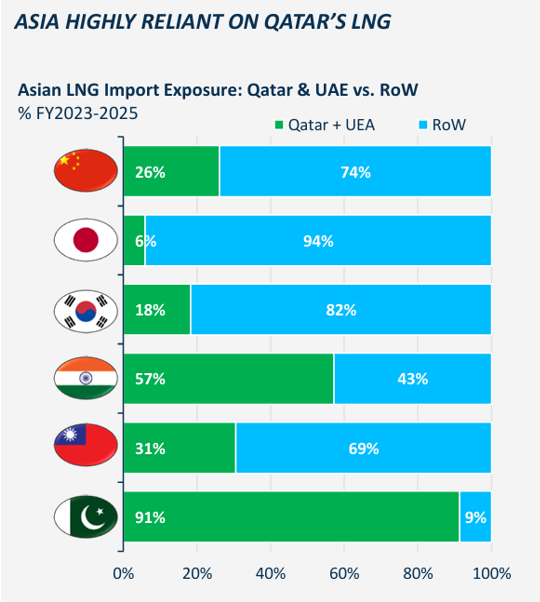

The chart below shows how heavily Asia is reliant on Qatari LNG supplies:

Source: Flex LNG

With Qatari supplies being out of the picture as of now, we shall see more inquiries coming from Asia and Europe for the same available volume.

So, we have a demand picture which is very solid, and we have the supply picture with an increase in additional export facilities. But the prolonged situation in the Middle East and the closure of the Strait of Hormuz should have a negative impact on the tanker, LPG and LNG sectors due to higher costs of both the commodities and the shipping expenses. So one should bear in mind this scenario too. However, if the situation is resolved within the upcoming few weeks, the revived demand for the mentioned commodities shall be positive for the tanker, LPG and LNG sectors. We shall see how things evolve.

LNG carriers’ current fleet and the outlook

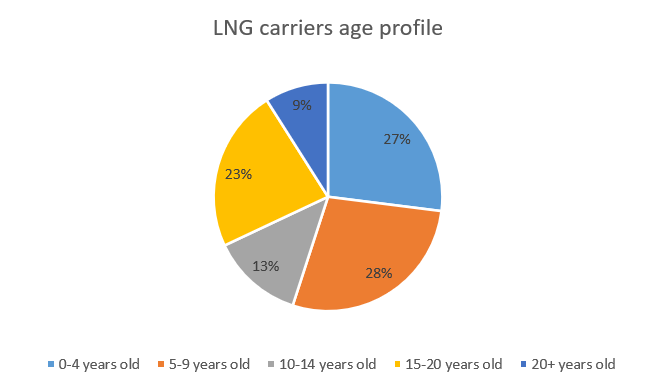

As of today, according to the analysis, we have the following picture of the LNG carriers’ age profile:

Source: Internal analysis

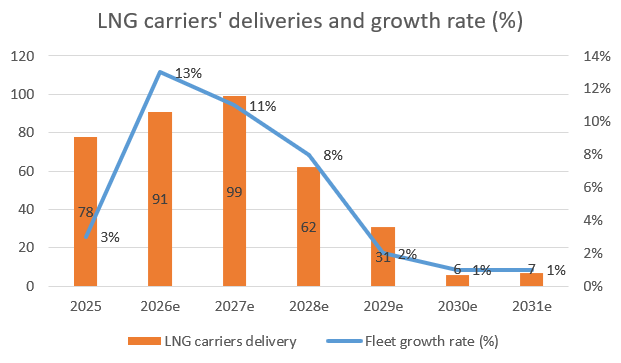

Due to increased demand for LNG since 2020, the LNG shipping companies had already started to order a lot of vessels from shipyards.

As per my analysis, we shall see the following picture of the fleet growth and number of vessels delivered in 2026 and onwards:

Source: Internal analysis

As you can see, the delivery growth rate is slowing down towards 2029-2030.

So, the fleet growth rate from 2025 towards 2028 looks solid, but we shall discuss whether the above delivery growth rate of LNG carriers will be absorbed by the growth of export volumes.

What to expect from the LNG sector in 2026?

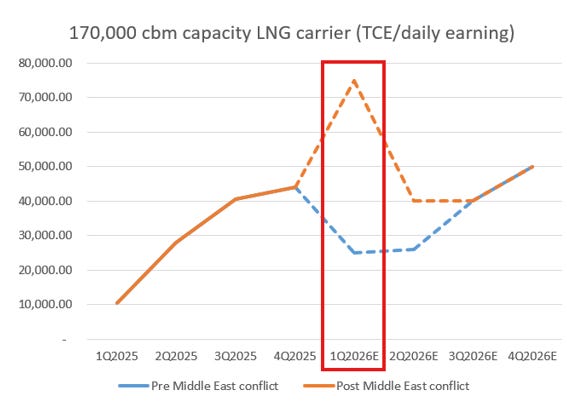

By projecting the global daily earnings/TCE of LNG carriers for 2026 and taking into account both the supply and demand of LNG and the supply of the new LNG deliveries, I get the following picture:

Source: Internal analysis

As you can see, my pre-conflict scenario was much more bearish in 1Q2026 vs the post-conflict earnings. My analysis will remain bearish for 2Q2026 and 3Q2026, due to the new deliveries of LNG carriers, but bullish for 4Q2026 due to seasonality and longer voyages from the port of loading to the port of discharge.

Now, let’s discuss the risks posed for LNG carriers.

Risks

One of the major risks I see is the potential recession due to prolonged conflict in the Middle East. Namely, if we continue to see high LNG, LPG and crude oil prices that affect the global demand for the mentioned commodities, there might be a potential economic recession in Asia and Europe, whose countries (especially in Asia) heavily rely on LNG from Qatar.

The second risk I would like to emphasise is related to the outage of LNG production in Qatar, which should have a huge negative impact on the LNG shipping rates (around 77 mtpa are off the market). According to Qatari officials, the restoration of the Ras Lafan infrastructure will take at least two weeks, if not months, to restore (8).

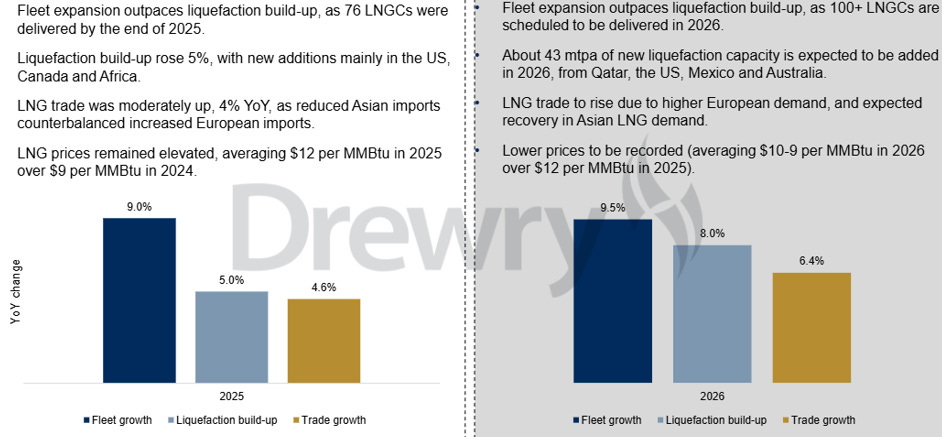

The third important risk is the delivery of around 91 new LNG carriers in 2026, and there is a high probability that the growth rate in production and export of LNG will not be able to absorb the growth rate of the new LNG carriers’ deliveries, which will lead to lower daily earnings/TCE. A very good illustration was provided by Drewry (9):

Source: Drewry

As you can see in 2026, the fleet growth exceeds the infrastructure addition by 1.5 per cent. And with the Qatari expansion of North Field East and North Field South being under question, we might expect the commissioning of the mentioned fields to be delayed.

Conclusion

The current situation in the Middle East and its effect on the LNG carriers’ rates will depend on how long the conflict lasts and how long it will take for the damaged LNG infrastructure to restart. In addition, we have to bear in mind how the Middle Eastern LNG companies might decide on the expansion of the existing infrastructure.

Furthermore, despite the expansion of the LNG export capacity in major loading areas (as of now, we have to exclude Qatar), there is a huge risk that the new LNG carriers’ capacity will not be absorbed by the growth rate of the LNG export. This might pose a huge risk to the LNG shipping rates.

My personal take is to take a wait-and-see stance and see how events will develop. As of now, the risks outweigh the rewards due to fundamental factors laid out above and uncertainties related to the Middle East conflict. From a value investing perspective, the LNG shipping sector is exposed to a lot of uncertainties, and we shall wait for a better and clearer picture to assess the risk vs reward. I.e., we as value investors shall look at low-risk/high-reward options.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 https://www.reuters.com/business/energy/qatarenergy-declares-force-majeure-lng-shipments-2026-03-04/

2 https://www.statista.com/statistics/1262074/global-lng-export-capacity-by-country/

5 https://discoveryalert.com.au/qatar-lng-production-model-2026-supply-dependencies/

6 https://www.oxfordenergy.org/wpcms/wp-content/uploads/2026/02/Comment-LNG-Wave.pdf

7 https://adi-analytics.com/2026/01/13/2026-adi-global-natural-gas-lng-outlook/

8 https://www.reuters.com/business/energy/qatarenergy-declares-force-majeure-lng-shipments-2026-03-04/