Outlook on the tanker market in 2026

(published on Substack on 13 Feb 2026)

As mentioned in one of my previous posts, there are a few sectors in the shipping industry. In today’s post, we will focus on tankers and their outlook for 2026.

It is very important to stress that the subject sector is sensitive to geopolitical factors and news headlines, especially any news related to the Middle East.

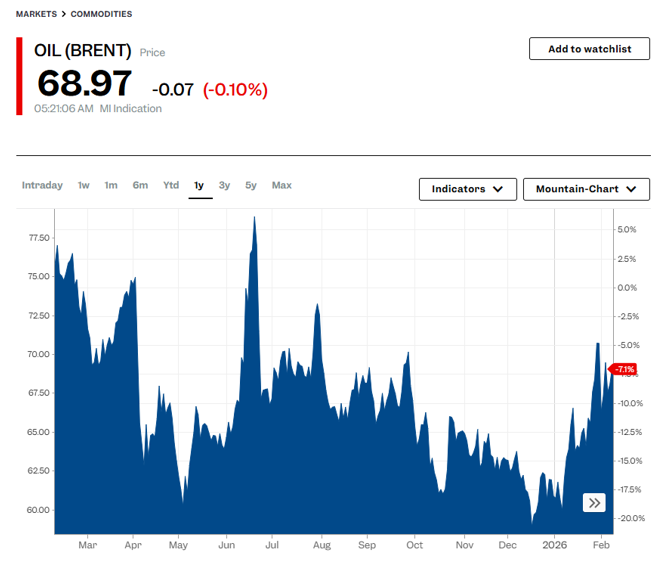

This year started very bullish for tankers due to US-Venezuela news reports and the looming potential US-Iran conflict. The above news pushed both crude oil prices and tanker markets’ daily earnings up (VLCC – Very Large Crude Carriers, used especially in loadings ex Middle East):

Source: Business Insider (https://markets.businessinsider.com/commodities/oil-price)

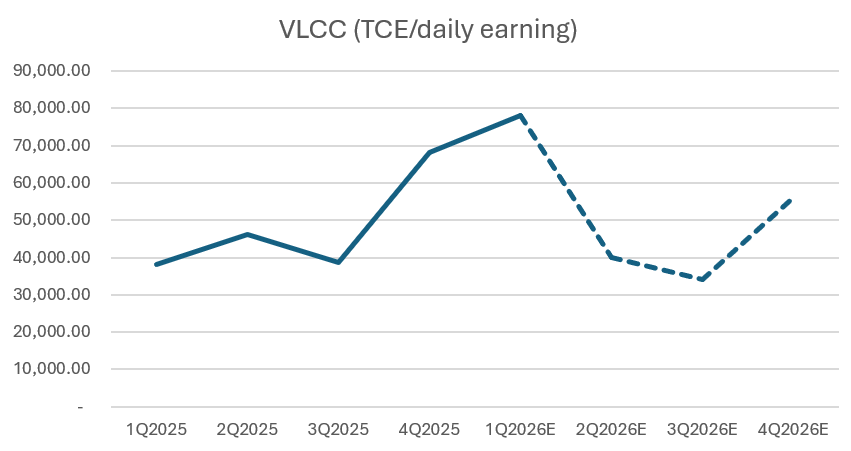

Source: Internal analysis

The average daily earnings/TCE for 2025 were at USD 47,833, and for 2026, as per my calculations and analysis, at USD 52,000.

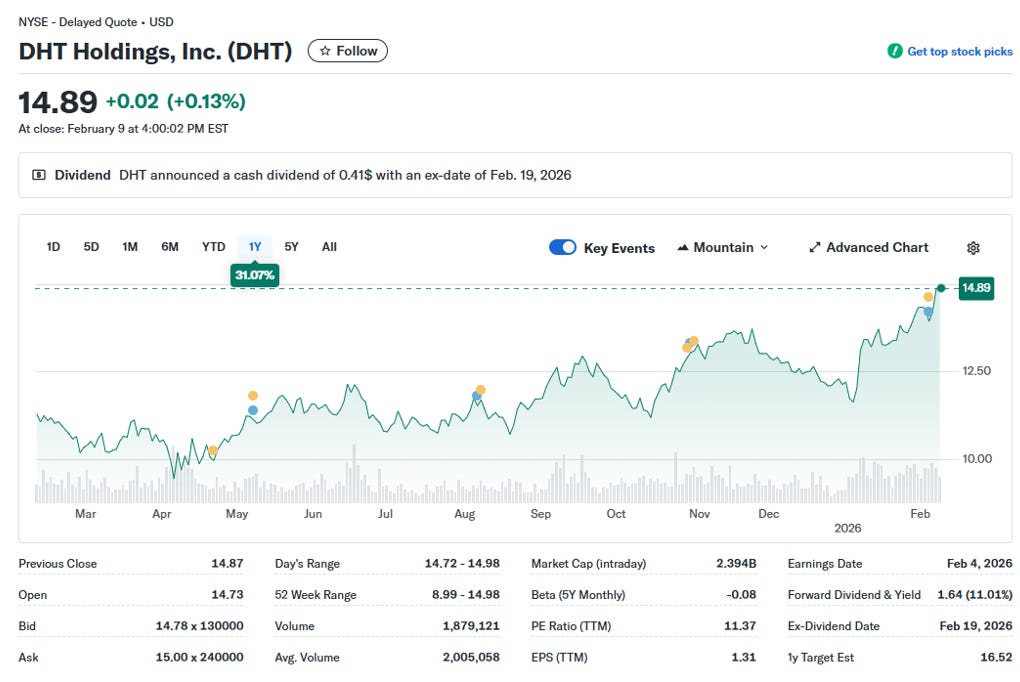

Below you will find the development of the DHT Holdings Inc. (ticker: DHT) stock, which is a pure VLCC player (they have 26 VLCCs in their fleet), operating globally and especially in the Middle East, reflecting the above events:

Source: Yahoo! Finance (https://finance.yahoo.com/quote/DHT)

Now, if you have a look at all three examples, you notice some similarities in terms of trend. However, we cannot expect one trend to affect the other totally, i.e., crude oil price to affect DHT equity directly (i.e. correlation). It will be a fool’s errand to act on it, as crude oil prices and DHT stock are affected by other important factors. But the company’s TCE or daily earnings do affect the shipping company’s stock performance, as the more the company earns, the higher the chance that its stock can potentially catch up with fundamental factors and post results of EPS.

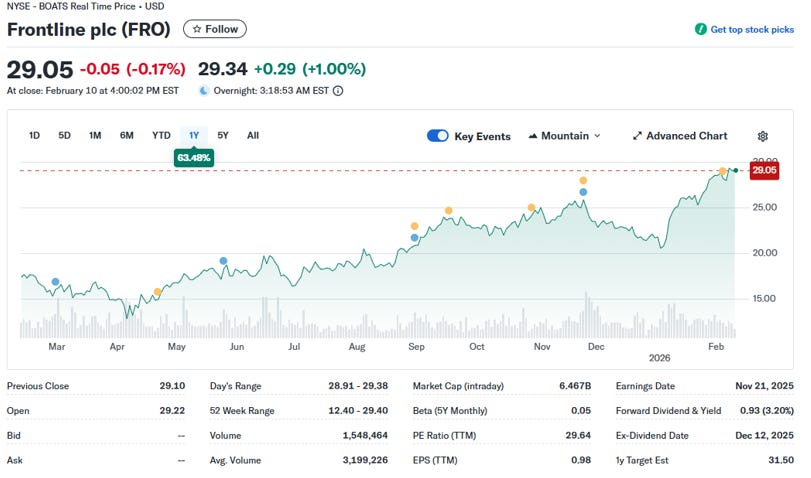

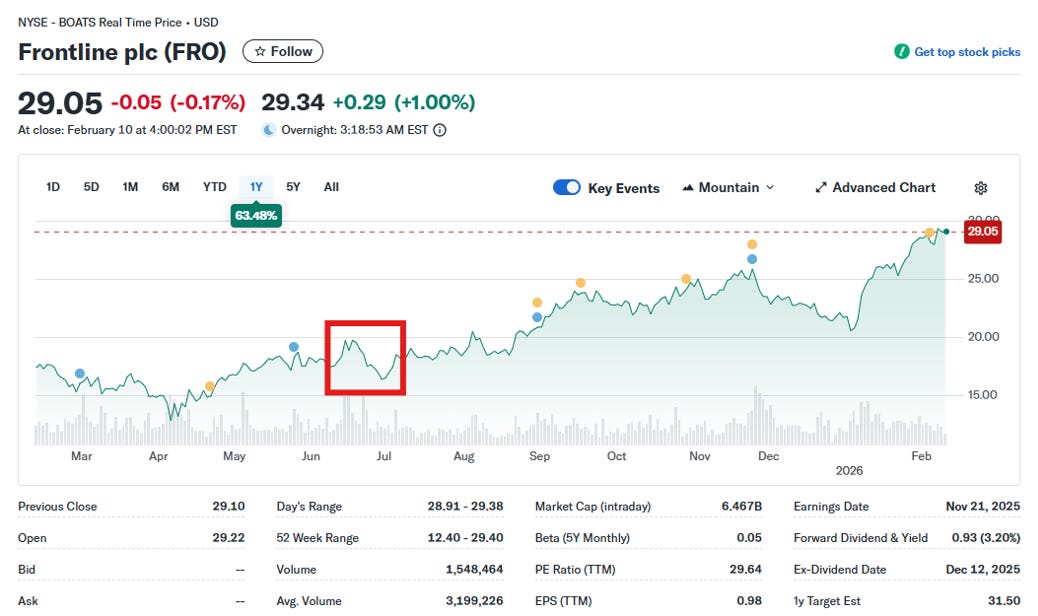

Let’s throw in an example of another tanker player, Frontline plc (ticker: FRO), showcasing this thesis:

Source: Yahoo Finance (https://finance.yahoo.com/quote/FRO)

Now, the tanker sector is very cyclical as it has the aspect of seasonality. Namely, the Q1 and Q4 quarters are usually the highest in terms of TCE/daily earnings as the weather at ports of loading and discharge deteriorates, vessels are delayed, and hence the need to hire another vessel to lift the crude oil.

During Q2 and Q3, the rates are usually lower due to lower probabilities of the factors mentioned above. I do not take into account the geopolitical factors as predicting them will be a waste of your and my time. It could push the stock price up, if and when it materialises. But my approach is based on fundamental factors, i.e. outlook and demand of the sector.

So if we look at the current prices of the stocks mentioned above, they seem overvalued. If the situation around Iran resolves, the stock prices will adjust back and notably go down, as we saw in June 2025:

Source: Yahoo Finance (https://finance.yahoo.com/quote/FRO)

You will find the stock plummeting from USD 19.77 per share to USD 16.50 per share within two weeks. Therefore, buying at this level does not promise a huge upside.

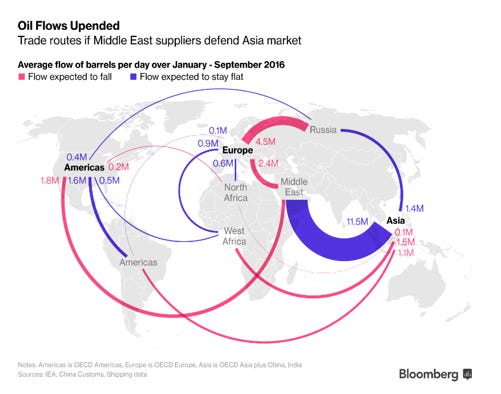

Now, why is the Middle East so important for crude oil prices, tanker rates and daily earnings/TCE?

The answer lies in the flow of export of the crude oil:

Source: Bloomberg

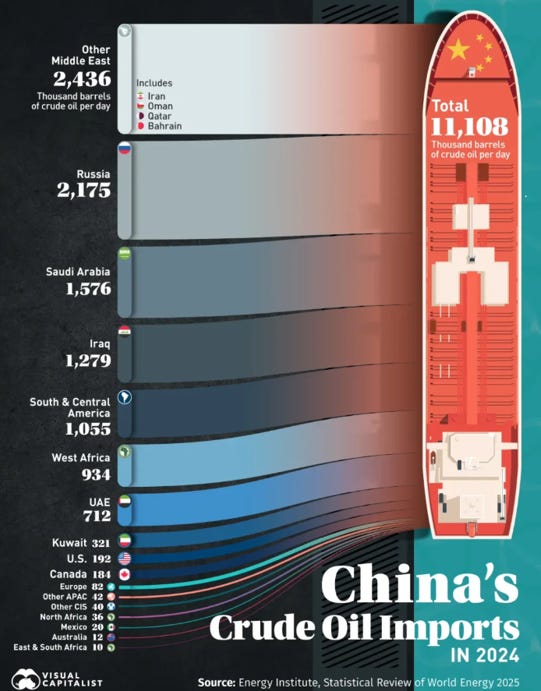

In 2024, China imported 6,324 thousand barrels per day of crude oil from the Middle East compared to imports from the rest of the world (3,442 thousand barrels per day of crude oil):

Source: Visual Capitalist (https://www.visualcapitalist.com/chinas-crude-oil-imports-by-country/)

Now, if I look at the above companies’ stock prices and look at my projections of daily earnings/TCE (please see above, dashed line for 2026), they pose high risk and low reward if the crude oil flow between the Middle East and Asia remains.

If I look at fundamental factors (daily earnings/TCE), the prices of FRO and DHT have already included the daily earnings and on top of that, priced in the premium of potential escalation. I strongly believe they are overvalued, and the risk of permanent loss of invested capital is high. In this case, we have to be patient and look at them when the right time comes.

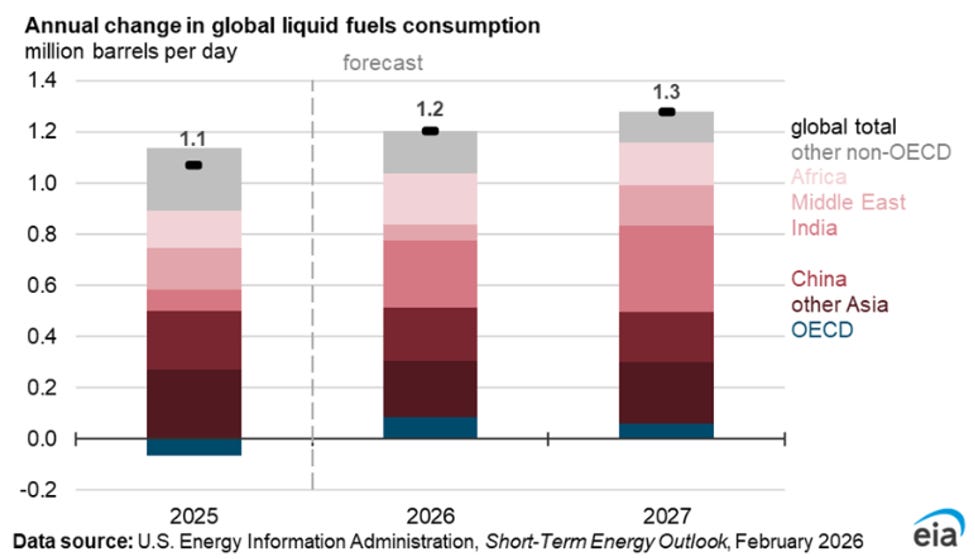

On another note, the overall outlook on the tanker sector for 2026 looks good in terms of crude oil consumption. And where the consumption is, there is crude oil import.

Source: EIA (https://www.eia.gov/outlooks/steo/report/global_oil.php)

Namely, in 2026 and 2027, the global oil consumption is slated to be 1.2 mbd and 1.3 mbd more than in 2025. Which is a good sign for the tanker sector as most of the consumption is concentrated in Asia (incl. China).

Now, regarding the fleet supply for the VLCC segment of the tanker sector. According to Gibsons, 32 and then 41 new vessels will be delivered to the market in 2026 and 2027, respectively (source: https://www.gibsons.co.uk/report/vlccs-in- vogue/#:~:text=The%20orderbook%20for%202026%20and%20beyond%20has%20grown%2C,10%20years.%20Meanwhile%2C%20the%20fleet%20is%20rapidly%20aging).

Also, the existing VLCC fleet within the market is ageing rapidly. 35 per cent of the current VLCC fleet is 15 years old (built before 2010), and 16 per cent is over 20 years old (built before 2005) (source: https://www.breakwaveadvisors.com/insights/2025/2/2/vlccs-in-vogue).

In terms of supply of newly built VLCCs, we are at a very low rate, and, in conjunction with the ageing fleet, the VLCC market’s daily earnings/TCE shall be healthy in 2026 as the demand for vessels outperforms the supply (please see above the chart with my projections).

If we have three fundamental ingredients (crude oil consumption, ageing fleet and low delivery of the newly built vessels), we get a very constructive picture of daily earnings/TCE for 2026 projected to be higher than in 2025. Based on the current prices of FRO and DHT, there is a high risk/low reward, and the stocks are overpriced. However, as we mentioned, the overall positive outlook for 2026 and the cyclicality, it is worth noting that I will monitor the development of daily earnings/TCE and write deep dive posts about the companies FRO and DHT in due time.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com