Q1 2026 update of DHT Holdings, Inc. (DHT)

Dear fellow value investors,

Today, we will analyse the results of Q1 2026 for DHT Holdings, Inc. (DHT) and apply the NAV valuation. We will examine what the subject business’s stock price offers in comparison to its intrinsic value. In general, this company, along with other companies engaged in the LNG, LPG, and tanker segments of the shipping industry, and their stock prices rallied due to recent geopolitical events (starting from 28 Feb 2026), rather than solely fundamental factors. In our analyses of companies, we discussed that fundamental factors should support the trend upwards (it is, after all, what we like to see), but it is obvious that the current elevated prices are mainly based on sentiment and geopolitical escalation.

Let’s dive in.

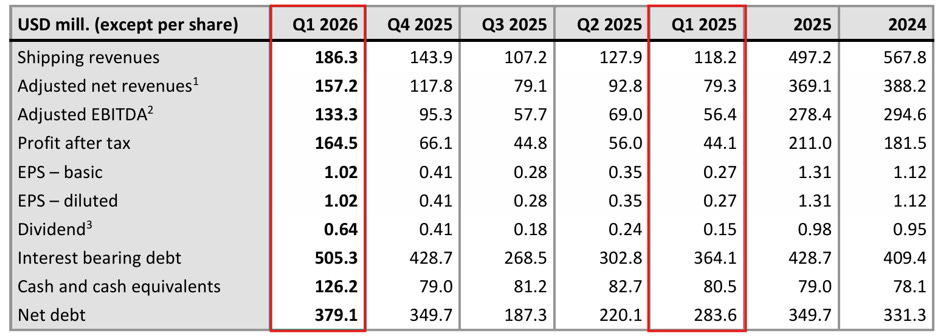

As it was expected, due to the Middle East conflict and the effective closure of the Strait of Hormuz, strong results in the tanker segment during Q1 2026 came as follows:

Source: Internal analysis based on DHT reports

If we compare the results to the same period last year (i.e. 31 Mar), we can see a stark difference (1):

Source: DHT Holdings, Inc. First Quarter 2026 Results

The numbers are good. Only the FCF is negative due to capital expenditures related to investments in vessels that are under construction and dry docking. In Q1 2026, DHT allocated USD 163 million for these types of expenses.

The company’s current fleet consists of 24 tankers (versus our latest analysis of 25). The company sold the vessel DHT China (built in 2007), and the deal was closed on March 30, 2026. In Jan 2026, DHT agreed to sell DHT Bauhinia (2007-built) and the deal is expected to be closed by Jun-Jul 2026. The strategy to sell older units is sound as it allows to divest inefficient vessels at the current high valuations.

Also, they have received three new VLCC tankers in Q1 2026, which puts them in a position to take advantage of the rising freight rates and thereby the ability to enhance their financial performance.

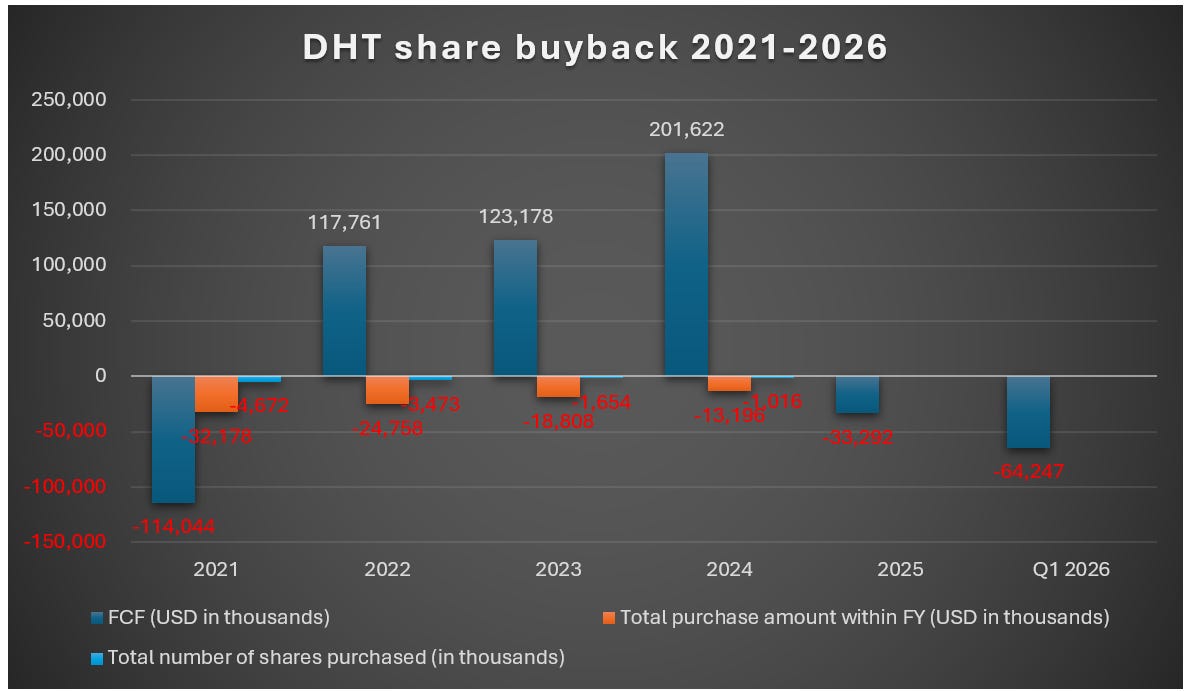

The company has not been repurchasing its shares lately, and the number of shares outstanding has gone up:

Source: Internal analysis based on DHT reports

Source: DHT Holdings, Inc. First Quarter 2026 Results

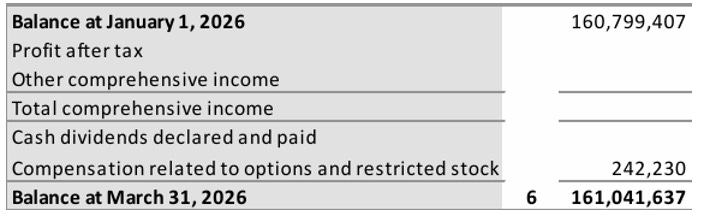

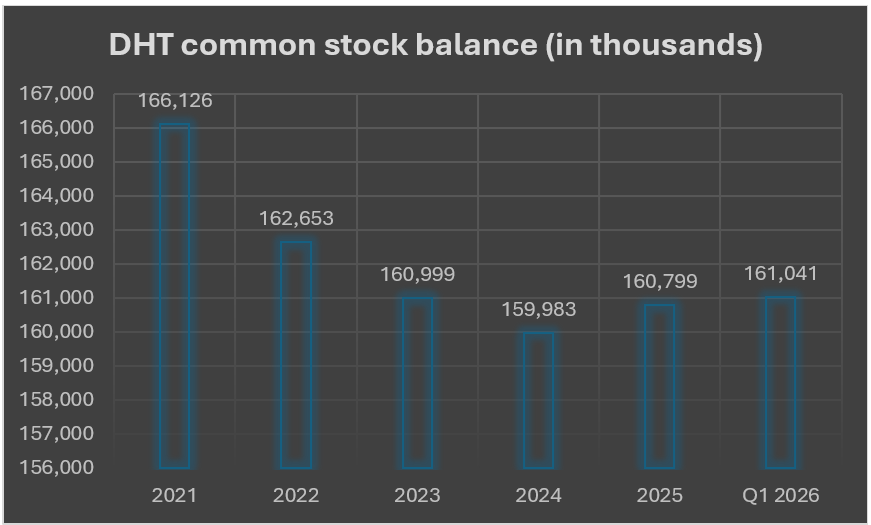

Despite the buybacks in recent years, the number of outstanding common shares has been increasing since 2024:

Source: Internal analysis based on DHT reports

In other words, the share of the total pie for long-term investors is being diluted by an increasing number of outstanding shares via the issuance of either options/restricted stocks or ordinary shares to raise capital. That being said, the management doesn’t engage in share buybacks at high levels, which is a positive. Instead, DHT’s strategy is to compensate investors via dividend payouts of 100 per cent of their ordinary net income. Which would be a nice reward for shareholders.

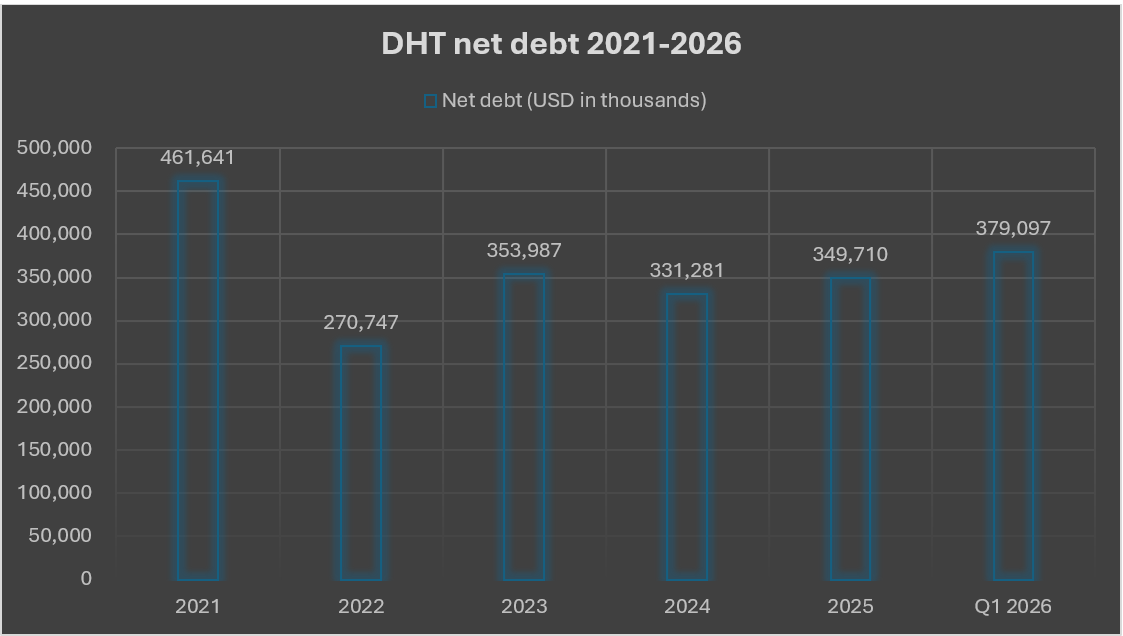

Let’s look at the company’s net debt:

Source: Internal analysis based on DHT reports

It has been climbing up since 2022, but is still lower than in 2021.

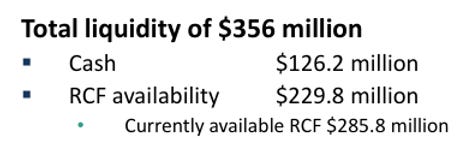

The cash and cash equivalents position stands at USD 126 million compared to the FY ending 31 Dec 2026:

Source: DHT Holdings, Inc. First Quarter 2026 Results

The available revolving credit facility as of 31 Mar 2026 is USD 230 million:

Source: DHT Holdings, Inc. First Quarter 2026 Results

Now, as of 6 May 2026 (the day of the presentation), the company had available RCF worth USD 286 million, and if we add it to the available cash and cash equivalents, we get around USD 412 million.

In 2026, the company expects seven VLCCs to be drydocked (one VLCC has already been completed), which we should count as capital expenditures.

Now, let’s check their guidance.

Guidance

The management has informed the analysts during the earnings call that the company started Q2 2026 with even stronger daily earnings/TCE. They have no further plans to divest any other vessels except the one indicated above.

DHT advises that the distance of crude oil transportation increased versus the pre-Middle East conflict and the effective closure of the Strait of Hormuz. Namely, the majority of crude oil loadings take place in the US, South America and West Africa.

According to shipbroker firms, some volumes are being loaded in Yanbu, Saudi Arabia (36 cargoes in May as of 12 May 2026), but the cargo liftings from the Middle East (as of 12 May 2026) in May 2026 made up only 14 versus 157 in May 2025. In Apr 2026, only 24 cargoes were lifted from the Middle East loading areas versus 155 cargoes in 2025. And it is worth noting that the majority of these cargoes used to head to Asia in 2025. Now, the distance lengthened, leading to higher utilisation of the tankers due to longer voyages between the ports of loading and discharge. In other words, the market has a lower supply (fewer cargoes) but a longer distance to deliver these cargoes.

Also, around 10 per cent of the global VLCC fleet is either waiting with the loaded cargo to exit the conflict area or is unproductive.

All in all, the management has a strong short-term outlook for the VLCC segment.

The fundamental factors related to the supply/demand for crude oil remain unchanged since our last post on DHT. The same is applicable to the global VLCC fleet.

One shall bear in mind that the current elevated daily earnings/TCE rates are not solely based on fundamental factors (hence the current level of the stock price). They are also influenced by sentiment, which stems from the current geopolitical situation.

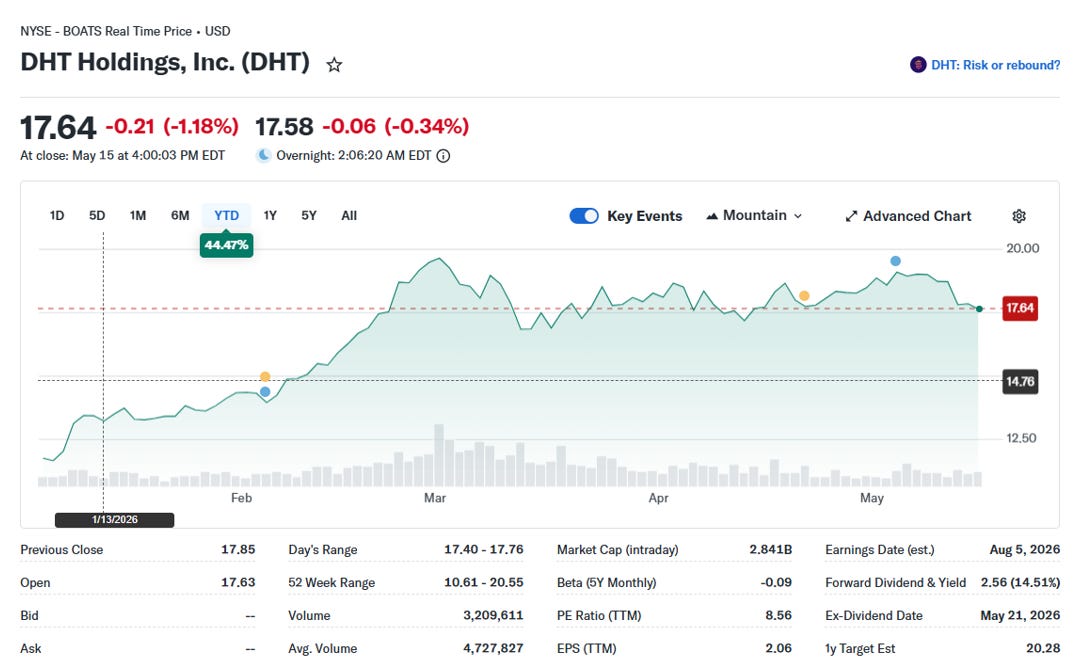

Stock valuation

The stock of DHT at the time of writing (18 May 2026) closed on 15 May 2026 at the level of USD 17.64 per share:

Source: Yahoo Finance

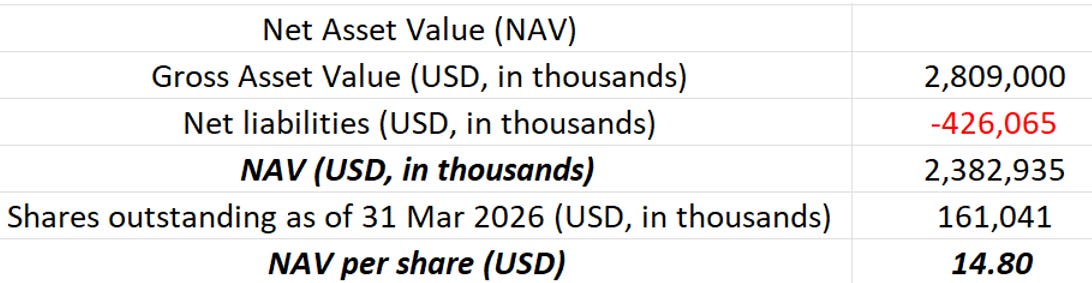

By calculating the NAV per share, we can see that by adding updated inputs such as the increased number of outstanding shares and the net liabilities, we get USD 14.80 per share:

Source: Internal analysis

Now, if we compare our intrinsic value with the current stock price of DHT, we can see that it is overvalued (at the time of writing, i.e. 18 May 2026). Moreover, as per analysts, the 12-month target price is ranging between USD 20 and USD 21 per share, which offers a risky and limited potential upside. It is worth noting that the stock might even reach USD 23 per share.

However, despite fundamental factors laid out in the previous post related to the global VLCC fleet, supply and demand for crude oil and the current geopolitical situation, which have been taken into account by the market stakeholders, and our intrinsic value, the stock seems overvalued from a value investing perspective. Even if we assume (which is a bet) that the stock might reach USD 21 per share, the upside might be 19 per cent with a high-risk/low-reward probability.

It is important to note that upon the resolution of the issue around the Strait of Hormuz, the depleted inventories of crude oil, LPG, LNG and petroleum products should be replenished, which in turn will lead to higher demand for tankers, LPG and LNG carriers and might affect the share prices of DHT and other publicly listed shipping companies positively.

Now, here lies the dilemma for the investor. According to Warren Buffett, we have to resort to Aesop’s parable called “A Bird in the Hand”, which says: "A bird in the hand is worth two in the bush”. Mr Buffett advises us to think about this fable in investment terms as follows. A bird in the hand (your capital) is worth two birds (your potential rate of return) in the bush. The questions we as value investors have to answer are: 1) how many birds there might be in the bush (expected rate of return); 2) when you expect to get these birds (timeline); 3) how sure you are about it (probability).

One shall bear in mind the risks discussed and laid out in one of the previous posts related to DHT and the seasonality of the VLCC tanker segment.

In conclusion, the current price of the DHT stock seems overvalued versus its intrinsic value, and as per recently published posts, we found better alternatives, which offer us better returns with a low-risk/high-reward option.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Please find us on: https://valueinvestinginshipping@substack.com

Sources:

1 DHT Holdings, Inc. First Quarter 2026 Results