Q1 2026 update of Scorpio Tankers Inc. (STNG)

Dear fellow value investors,

In today's review, we will analyse the unaudited financial results of Scorpio Tankers Inc. (STNG) and apply NAV valuation to understand if the business’s stock price is currently fairly valued, overvalued or undervalued and make an informed value investing decision.

We recently had a deep dive discussion about STNG (please read the relevant analysis posted on May 5th, 2026).

STNG

Q1 2026 results

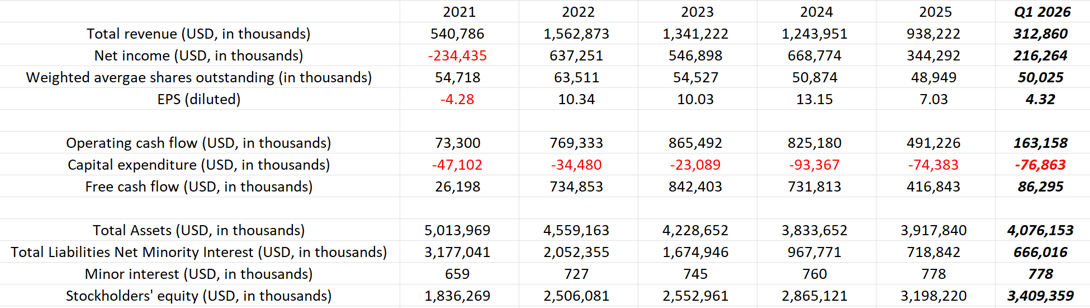

The business of STNG has been running as usual, with some divestments of older units during the Q1 2026 period, which we shall touch upon later. Meanwhile, looking at our internal analysis, due to the current situation in the Middle East, the Q1 2026 results came in very strong:

Source: Internal analysis based on STNG reports

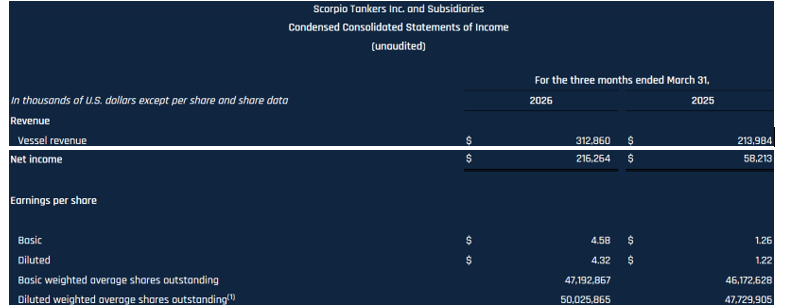

The revenue, net income and FCF are stellar. If we compare the results of revenue and net income with the period ending Mar 31, 2025, we get the following picture (1):

Source: Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

As mentioned above, the company has been divesting its old units. During Q1 2026, STNG sold eleven units (3 of which were reported in the previous post related to STNG) worth USD 500 million (2). Now the fleet consists of 87 product tankers with an average age of 10.2 years. The company also has 10 newbuilding deliveries as mentioned in the previous post.

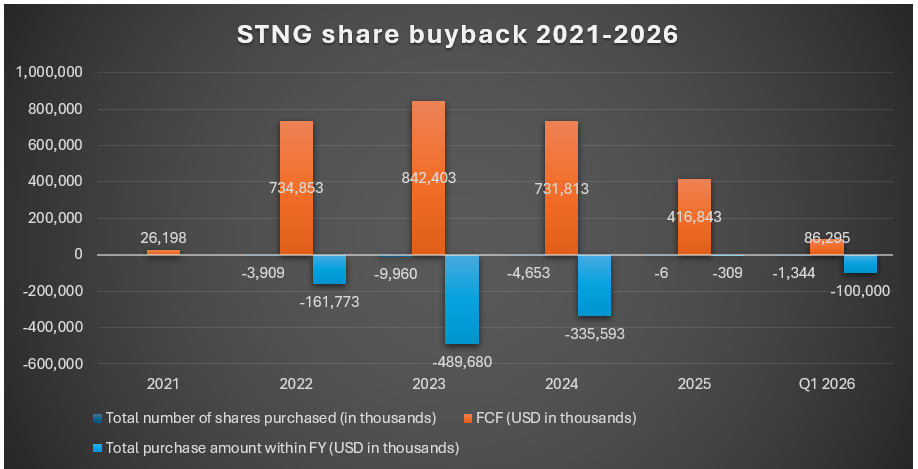

As you can see from the updated shares buyback chart, the company purchased around 1.3 million shares worth USD 100 million:

Source: Internal analysis based on STNG reports

They intend to increase the Share Repurchase Program up to USD 500 million (from USD 400 million basis the 2023 Securities Repurchase Program). As per the company’s comment during the Q1 2026 earnings call, the management advised that they repurchased around 1.4 million shares worth USD 100 million. We shall include this comment in our NAV valuation.

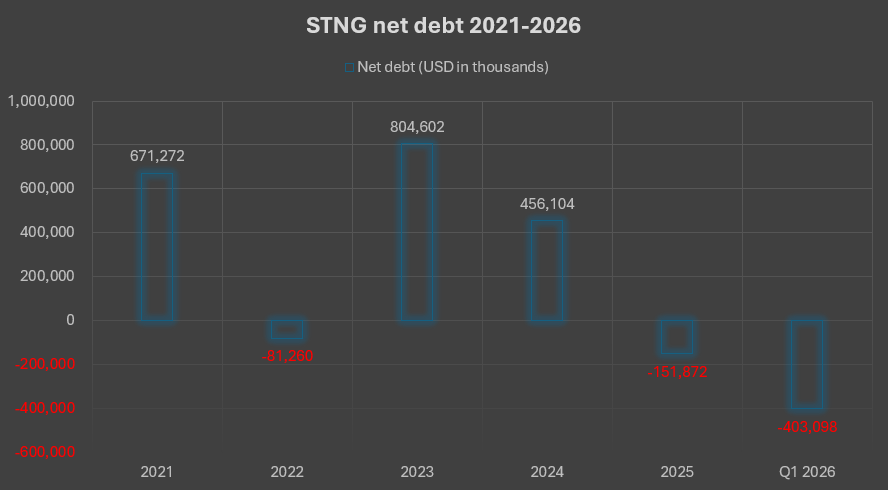

Let’s have a look at the net debt:

Source: Internal analysis based on STNG reports

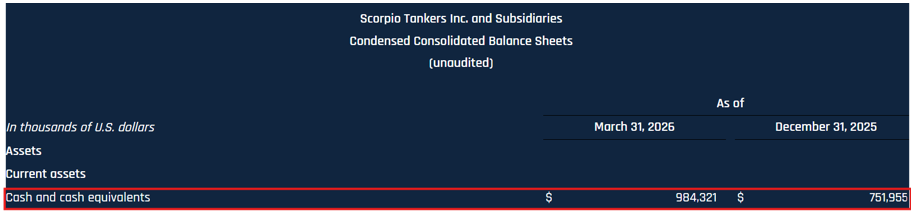

As you can see, after deducting the cash and cash equivalents from the total debt, we get a positive net cash position of USD 403 million. But by looking at their cash position, it stands at USD 984 million:

Source: Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

If we add to the above the available revolving credit facilities of USD 712 million, we get around USD 1.7 billion. That is excellent financial liquidity and a created fortress.

It is worth noting that STNG’s breakeven is around USD 11,000 per day, meaning that the company can weather any downturn period, as it is a super low metric. Implying that if the daily earnings/TCE are USD 25,000 per day, the company’s cash flow/profit is USD 14,000 per day.

Now, let’s look at the management’s outlook.

Guidance

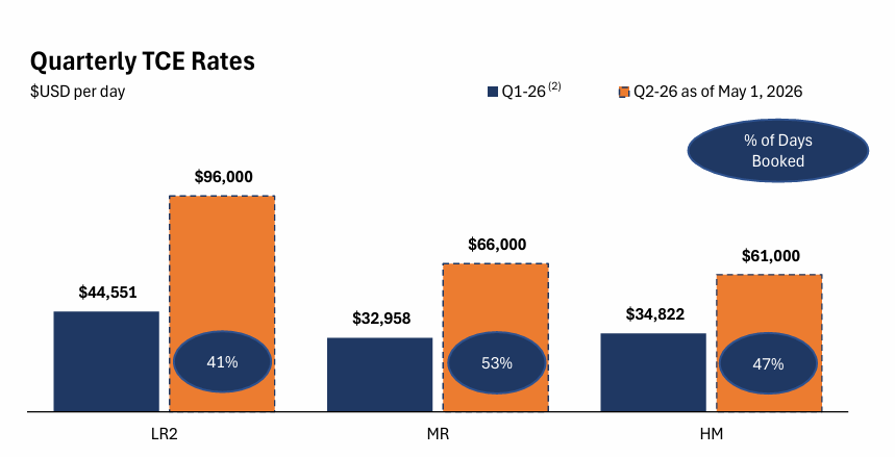

As per STNG’s guidance, the company’s product tanker segments (LR2, MR and Handymax) started in Q2 2026 stronger than in Q1 2026. Namely, if we assume that the breakeven is USD 11,000 per day, then the daily cash flow/profit from the fleet shall definitely be better than the Q1 2026 basis the below chart:

Source: Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

Let’s see how the second quarter progresses. But the prospects are looking positive already.

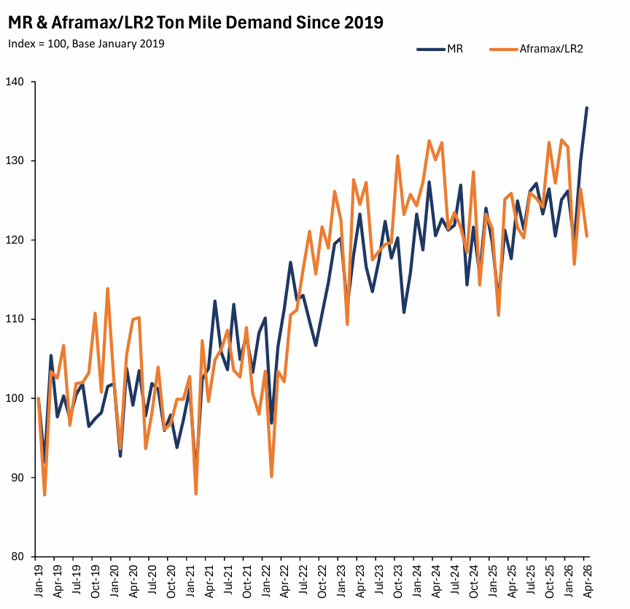

The ton-mileage demand for MR and LR2/Aframax has been increasing since 2019, based on the fundamental factors we discussed in our previous analysis of STNG:

Source: Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

And since the effective closure of the Strait of Hormuz, the consumers have to source petroleum products further away. This lengthens the utilisation of petroleum product tankers, thereby tightening the supply of vessels.

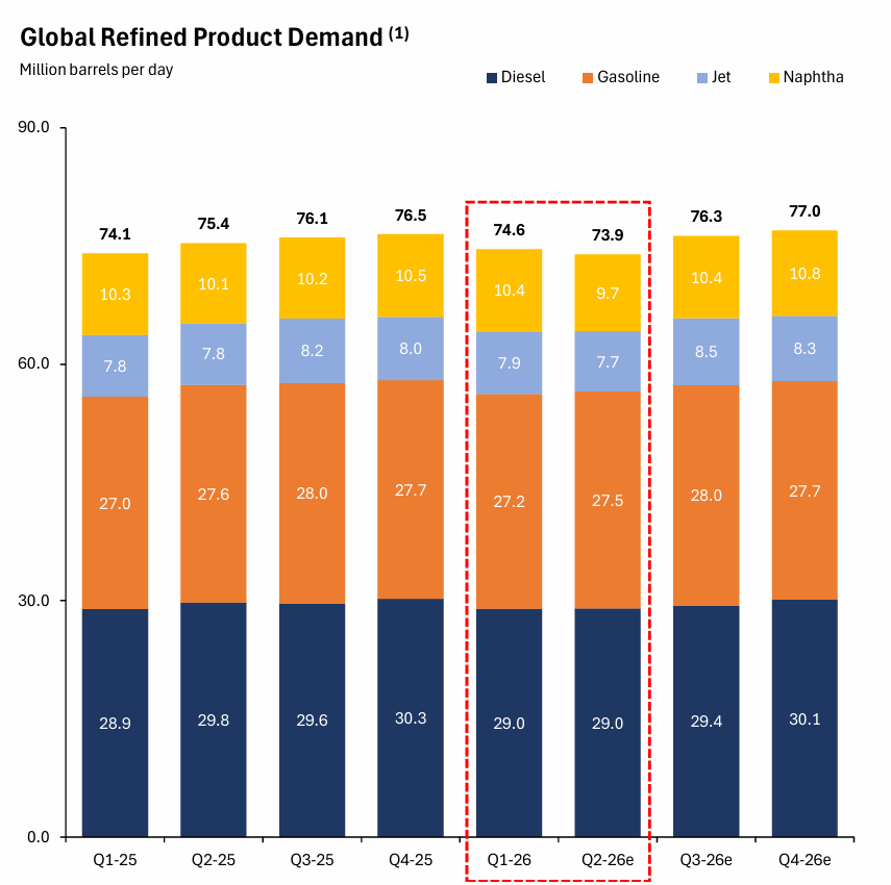

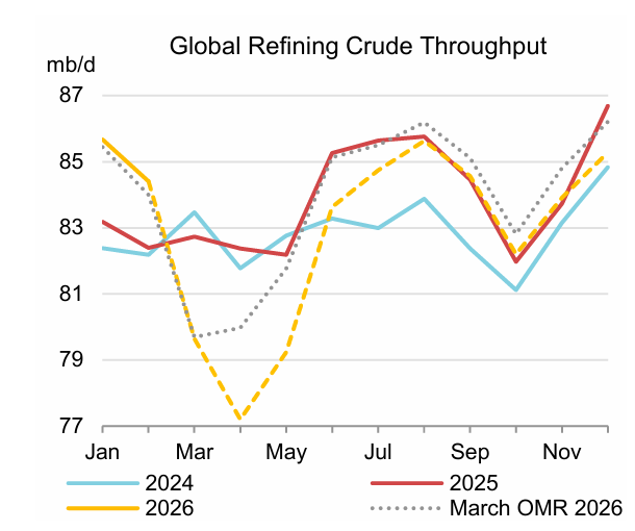

According to the company, the global products demand is expected to fall in Q2 2026 and then is expected to rebound in Q3 2026:

Source: Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

The same forecast has been published by IEA (3):

Source: IEA

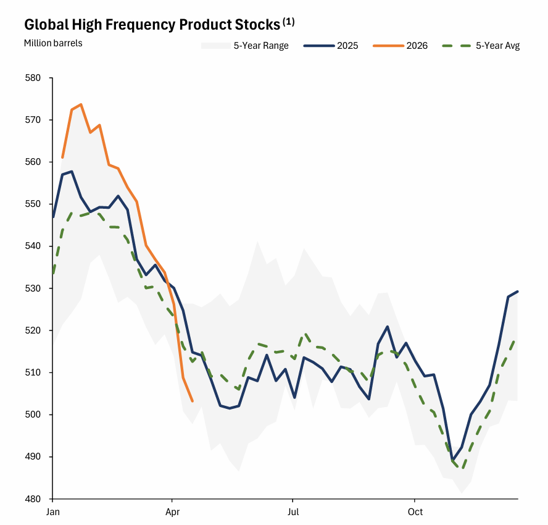

If and when the Middle East crisis is solved, and the Strait of Hormuz opens again, the company expect the restocking of global inventories:

Source: Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

The only thing to add is that the above view is also applicable to crude oil, LNG and LPG inventory replenishment. In theory, it should support freight rates of crude, petroleum products, LNG and LPG carriers. As of today, the situation remains fluid and changes daily, if not hourly.

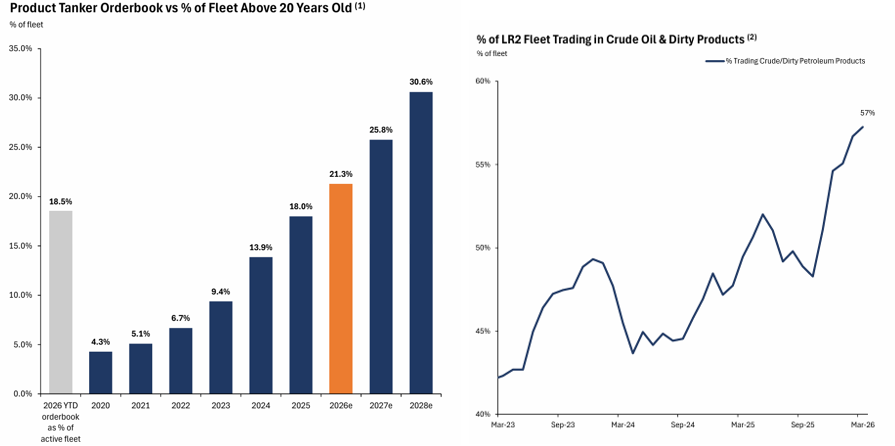

If we look at the global product tanker fleet, the situation has not changed since our latest deep dive research. We shall reiterate the same points, such as the ageing fleet and the majority of LR2 tankers trading crude oil or dirty products cargoes:

Source: Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

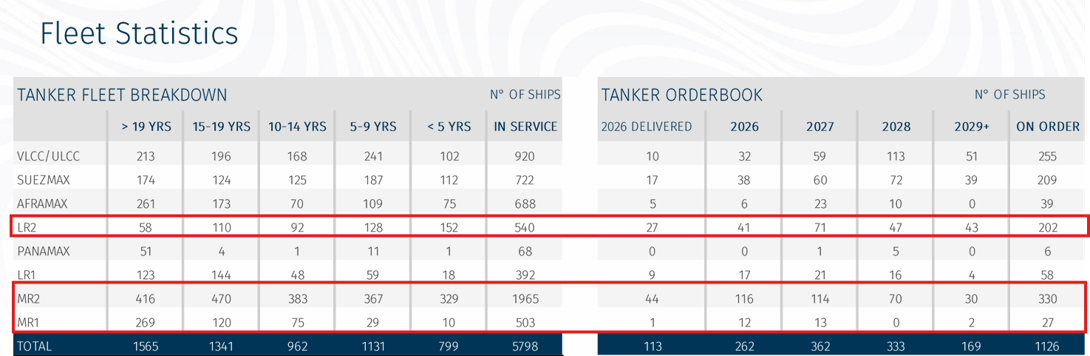

As of today, the product tanker supply has the following picture (4):

Source: BRS

We have a very constructive outlook with fundamental factors such as increased distances between the refineries and the consumers, and the ageing fleet with limited supply growth.

Stock valuation

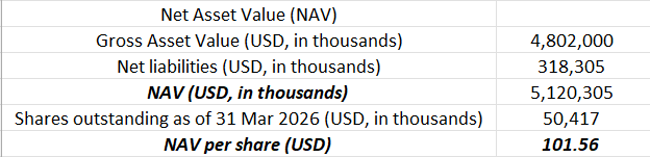

As we mentioned above, the company has been repurchasing the shares outstanding. Let’s have a look at the NAV per share:

Source: Internal analysis

As you can see by reducing the shares outstanding by 1.3 million shares and increasing the net cash position, our NAV increased by USD 14.58 per share, from USD 86.98 per share (from the latest analysis) to USD 101.56 per share.

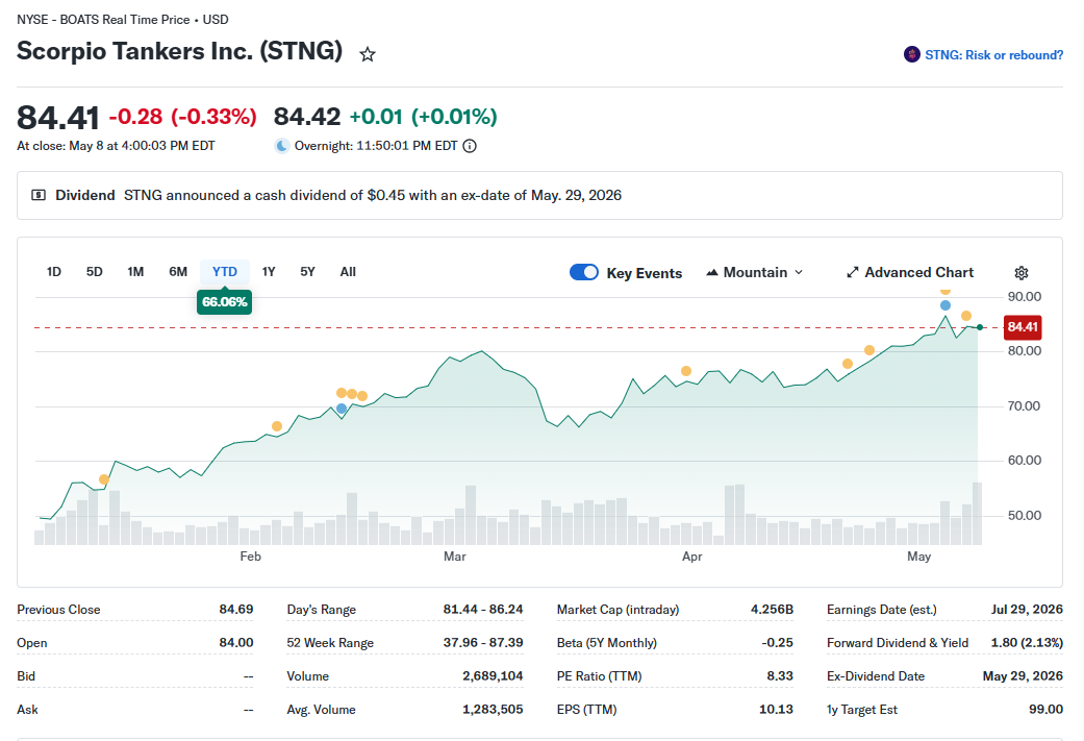

At the time of writing (11 May 2026), the price of STNG closed on 08 May 2026 at USD 84.41 per share:

Source: Yahoo Finance

If we compare the current price of the business with our NAV per share, we have a potential upside of 20 per cent. But, from a value perspective point of view, we have to be conservative. As per analysts’ 12-month price target, it ranges from USD 95 to USD 99 per share. But in any case, the subject business’s current price seems undervalued compared to NAV per share or analysts’ price targets. The question is: what rate of annual return does one consider good for oneself?

One shall bear in mind the risks discussed and laid out in one of the previous posts related to STNG.

After analysing several businesses in the shipping industry, we found a few companies that were undervalued and offered low-risk/high-reward options according to our analysis and were added into our model portfolio at that time.

But as I mentioned before, it is up to you, my fellow value investors, to decide how a position fits your portfolio, considering your risk/reward perspective.

If you have any questions, don't hesitate to get in touch with me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 Scorpio Tankers Inc., First Quarter 2026 Earnings Presentation, May 5, 2026

2 Scorpio Tankers Inc. Announces Financial Results for the First Quarter of 2026, the Declaration of a Dividend and an Increase to its Securities Repurchase Program

3 https://iea.blob.core.windows.net/assets/515f3128-df1a-4d6c-beb4-fd91d2434bef/-14APR2026_OilMarketReport_Free_version1.pdf

4 BRS Weekly Tanker Newsletter, Apr 27, 2026