Value investing and cyclical stocks

(published on Substack on 27 Mar 2026)

Dear fellow value investors,

In this post, we will discuss the value-investing approach to cyclical stocks. There is a notion that the value investing philosophy is solely applicable to a specific type of stock. For example, it is considered that growth stocks, such as Apple, are not value stocks. This does not hold true, in my opinion.

Peter Lynch, who is one of the most successful investors, applied the value investing approach to various types of stocks. Namely, according to his book “One Up On Wall Street”, he observes a few types of stocks:

1. Slow growers;

2. Stalwarts;

3. Fast growers;

4. Cyclical stocks;

5. Asset plays; and

6. Turnarounds.

The publicly listed companies in the shipping industry, with their segments, are regarded as cyclical stocks, as well as any other commodity-related companies. This is good for us as value investors because when Mr Market and certain market participants are gloomy (when they tend to overreact and sell the stocks), we can take advantage of these opportunities. The Efficient Market Theory is therefore inapplicable to cyclical stocks, otherwise we would not see any mispriced opportunities.

So, what do we try to achieve here by applying the value investing philosophy to the shipping industry? We are looking at companies that have good management that allocates capital sensibly and lowers the company’s debt. The companies with a strong balance sheet and that offer us a low-risk/high-reward option are the ones that should spark our interest.

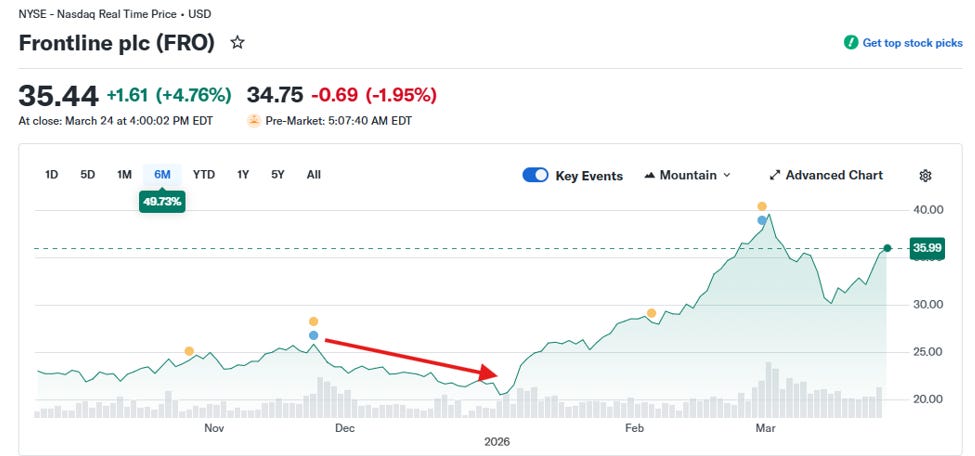

Besides good management, we will look at momentum within the market. Now, for example, the FRO stock (for a deep dive research, please check the post related to FRO dated 24 Mar 2026) over the last 6 months, you can see that Mr Market and certain participants were in a bad mood in November and December 2025:

Source: Yahoo Finance

The stock fell from USD 25.00 per share to USD 21.41 per share. Several factors might have influenced the above trend, but it does not matter to us as value investors, as it is pure noise. We always look at fundamental factors and apply a bottom-up approach. It is worth noting that we are not trying to time the market or predict the market. That will be a waste of our time. However, if the company has the potential to reach a higher market valuation, taking into consideration the industry’s cyclicality and the bottom/up approach, we shall consider buying the stock.

In other words, by applying value investing principles in the shipping industry, we focus on identifying undervalued companies with solid fundamental factors and build and compound our wealth gradually while minimising unnecessary risks.

We shall not forget about the MoS (Margin of Safety), which allows us to have some buffer for errors. Now, what happens if the stock price falls after we purchased it? We have to look at it objectively and understand whether our fundamental analysis was wrong or Mr Market is upset. In the latter case, if our thesis is correct, we shall buy more (please read about price movement in the post “Price movement vs value investing” dated 10 Mar 2026).

By applying the MoS, we limit the downside and increase the upside, which is part of the approach related to the low-risk/high-reward. Mohnish Pabrai famously wrote in his book “The Dhandho Investor: The Low-Risk Value Method to High Returns”: “Heads I win; tails I don’t lose much”. An example of a low-risk/high-reward option can be found in the recent posts related to the companies DSX (the posts “Diana Shipping Inc.” dated 20 Feb 2026 and 10 Mar 2026) and SHIP (the posts “Seanergy Maritime Holdings Corp” dated 10 Feb 2026 and 10 Mar 2026). In these posts, we discussed and elaborated on how these stocks should benefit from various fundamental factors and seem undervalued as of today.

In conclusion, a vital aspect of value investing is the management of the company, as it is responsible for making key strategic decisions, such as capital allocation, and its decisions might impact the financial performance. At the end of the day, the company’s management makes decisions that should be in the best interests of the company and its shareholders.

Nonetheless, the holding period of cyclical stocks is not forever. Moreover, cyclical stocks allow us to compound our wealth within a certain period of time. But when to sell a stock? It is a question each of us, my fellow value investors, has to answer for ourselves by continuously evaluating risk and rewards, considering the industry’s cyclicality.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com