Vessel investment and market cyclicality

(published on Substack on 07 Apr 2026)

Dear fellow value investors,

In this post, we will discuss how investments in vessels/assets affect the shipping industry’s market cyclicality. It is worth noting that if the company gets it right, it can blossom. If the company gets it wrong, it might be detrimental to its financial health.

The shipping industry is highly cyclical and experiences booms and busts. And during the booming period, the management will decide whether to invest or not in new deliveries of vessels. In other words, the management decides whether to expand its vessel fleet or not. It is worth noting that during the boom, a shipping company is flooded with cash, and allocations need to be made.

The shipping industry is highly correlated with the commodity cycle. The tanker segment of the industry is correlated with the oil and petroleum cycle, dry bulk carriers – with dry bulk commodities, such as iron ore, coal, etc.

It is worth noting that any vessel’s life span is around 20-25 years, and it takes around 2 to 3 years to build a new vessel at the shipyard, subject to slot availability. Namely, if the slots at the shipyard are busy with orders, for instance, with container liners and tankers, there won’t be any possibility to build a dry bulk or a gas carrier in the next 2 to 3 years, and this might create a mismatch between the commodity and shipping cycles of a particular segment. In other words, the market conditions might change faster than the supply.

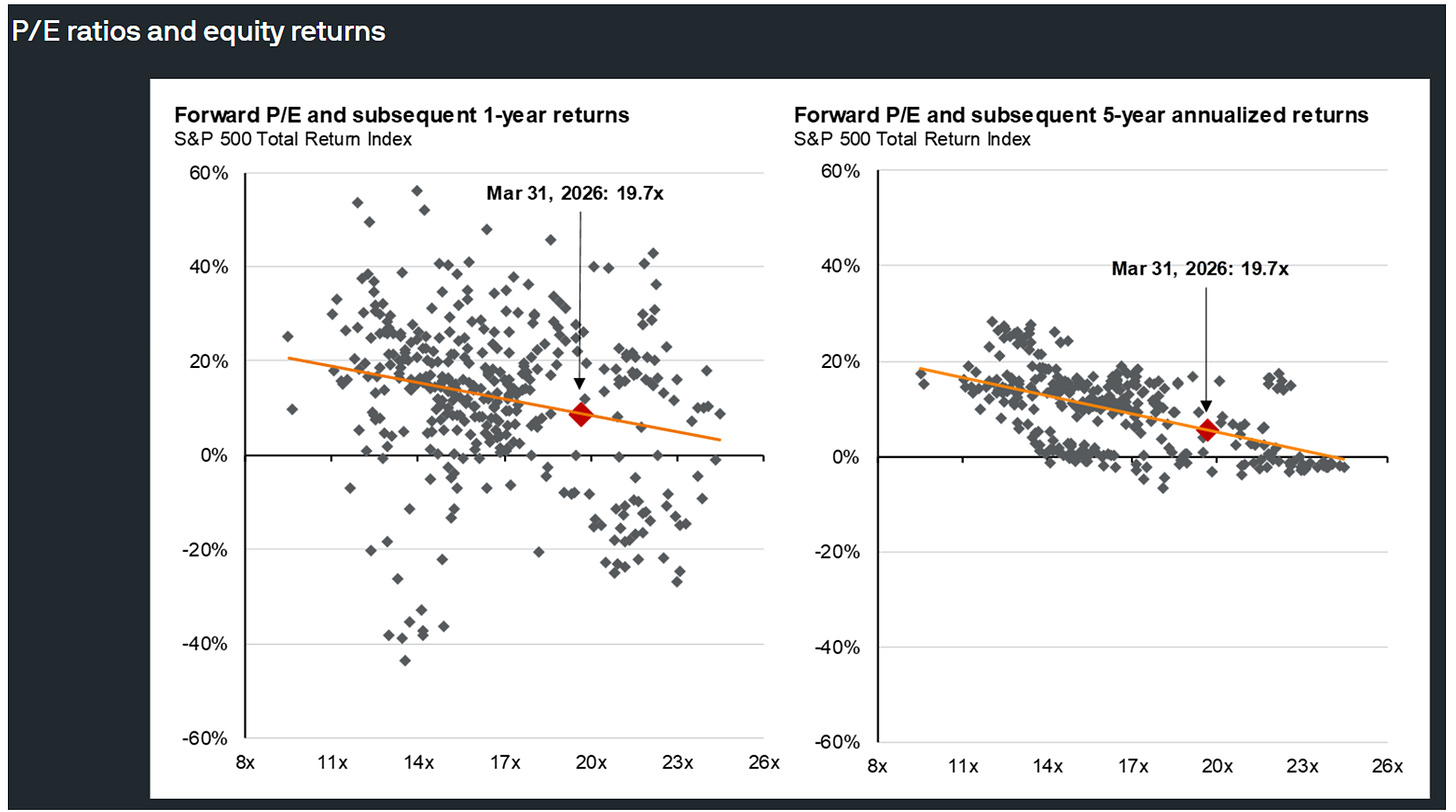

The asset prices and daily earnings/TCE are interconnected. But daily earnings/TCE are more volatile versus asset prices within the same period of time. If TCE is expected to be high, the shipping company should expect higher profits (cash flow) in the future, and higher vessel (asset) valuation. One shall bear in mind that asset valuation does not predict freight rates. In a boom cycle, asset valuation rises faster than earnings, leading to compressed yields. During the bust cycle, valuation drops, leading to a higher yield. You can compare the shipping industry assets to real estate or equities (1):

Source: J.P. Morgan, Guide to the Markets

As you can see from the charts above, the higher the price paid, the lower the annual future return. And this has to be a vital point for the management to decide whether or not to invest in the expansion of its fleet.

When to invest?

Now, let’s have a look at a hypothetical example of management behaviour in the shipping industry:

· Freight rates become high

· Asset values surge

· The company has easy access to financing

· The company rushes to order new vessels (which will be delivered in 2 to 3 years)

· The company pays inflated prices

The result is that the shipping market and its fleet capacity are oversupplied when new vessels are delivered, leading to collapsed rates and, eventually, poor returns.

A perfect example is the current state of the container freight rates and the relevant company’s stock price, such as A.P. Møller - Mærsk AS (for further information, please read the deep dive posted on 24 Feb 2026):

Source: Yahoo Finance

Now, as you can see, the container segment of the shipping industry had a prolonged period of underinvestment in new liners, leading to normal trends of seasonality. And during the COVID-19 pandemic, this played a huge role in boosting the revenues. Hence, the container rates spiked, which was reflected in the huge soar of Maersk’s stock price. From late 2020, when container rates started to rise, there was a flurry in ordering new liners, which were due to be delivered in 2022-2023. According to Container News (2), during the 2020 and 2021 period, due to frenzied orders, the 11 largest container owners were expected to receive 89 large container ships in 2023 (more than 12,000-18,000 Twenty-foot Equivalent Unit, further TEU). Moreover, the total delivery of new liners was 208 (1.4 million TEU) and 54 vessels were demolished (102,000 TEU). The chart below shows the impact of the delivery of new liners on Maersk’s revenue (4) in 2023:

Source: A.P. Møller - Mærsk AS

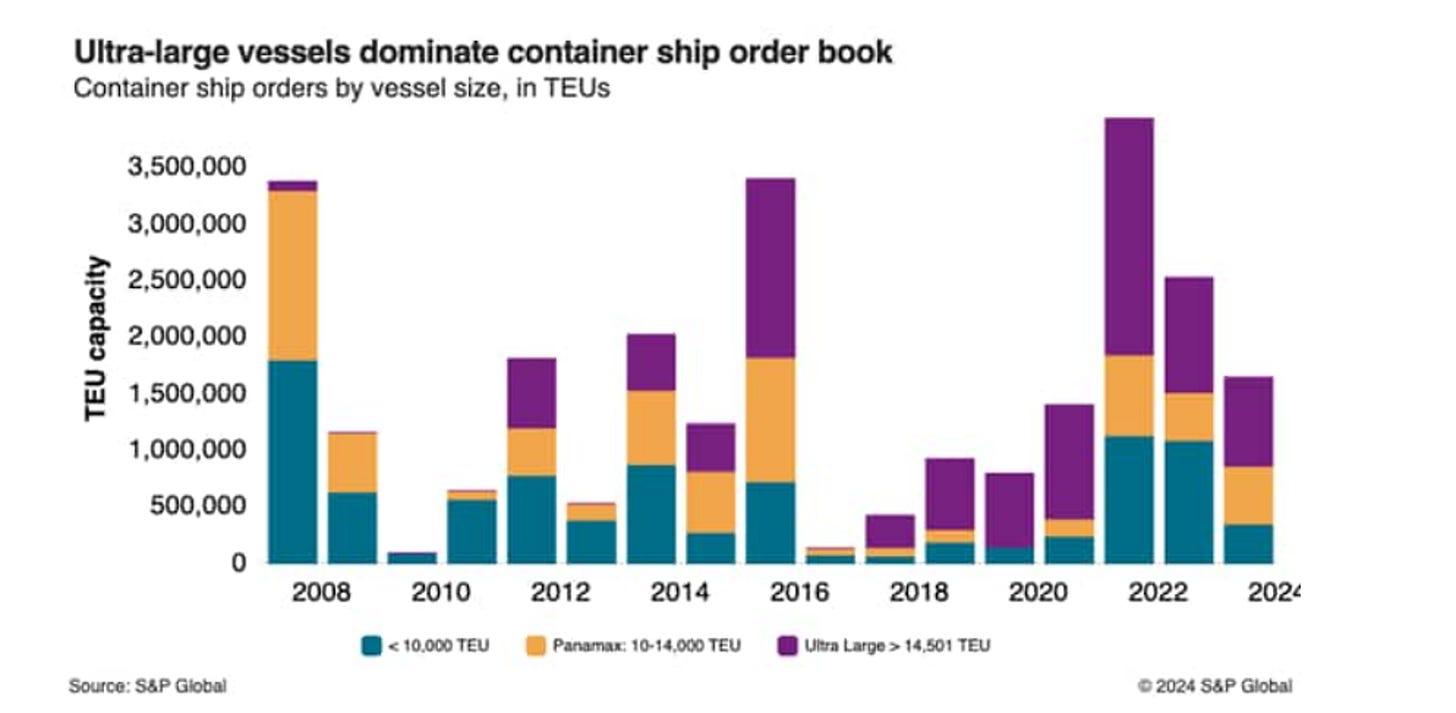

The peak of ordering of new liners was reached in 2022 (5), with delivery due in 2024 and 2025, when orders approached c. 25-30 per cent of the global liner fleet. In 2024, the fleet growth was forecasted at 9.1 per cent (3), despite the gloomy demand forecast for liners. These liners were ordered in 2022 (5):

Source: S&P Global

Now, this growth in the delivery of the new liners was not absorbed by the global growth rate of container transportation, which led to falling container rates and, hence, the relevant stock of publicly listed liner companies.

The above analysis has been discussed and published by Research in Transportation Business and Management called “Carrier profitability influenced by large containerships” (6). The article discussed the clear correlation between low demand for containers and overcapacity in fleet growth, depressing the container freight rates and affecting the company’s profitability.

Below is an example of how companies (in this case, Maersk, but the below applies to all companies in the liner segment or any company in the shipping industry) started to flock to invest in new vessel acquisitions:

Source: Internal analysis

Why is it applicable to all the market players in the liner segment in this particular case? Because otherwise, we would not have seen overcapacity in the delivery of new liners.

Now, when is the best time to acquire new or second-hand vessels or assets? If the cash generated during the boom remained at disposal, then strategic asset players in the shipping industry tend to invest when the freight rates are depressed, the TCE is low, which in turn affects the asset value of the vessels. This potentially should lead to higher returns in the future as the company pays a low price for an asset. As F. Fama & K. R. French (7) and R.J. Shiller (8) showed in their papers, high prices yield lower annualised returns.

So, if the company has a substantial and investable amount of cash, the best way is to avoid buying at the peak of TCE/daily earnings and at the peak of asset values. Otherwise, as mentioned above, the evidence suggests that the higher the prices of an asset, the lower the future returns. If many market participants flock to order new vessels, the freight rates will inevitably be crushed once these vessels hit the water. The best strategy would be to monitor the market and acquire assets based on fundamental factors and cyclicality.

It would be beneficial for companies to divest the older units during the peak and keep the cash, when the cycle is in a downturn, to make a move in terms of acquiring new units. However, it is quite difficult to resist the pressure from the company’s shareholders to refrain from buying newer units. However, as it was mentioned in the paper called “The importance of timing in energy shipping: a case from Cyprus” (9), it is quite daunting to time the investment decision. But it is not impossible.

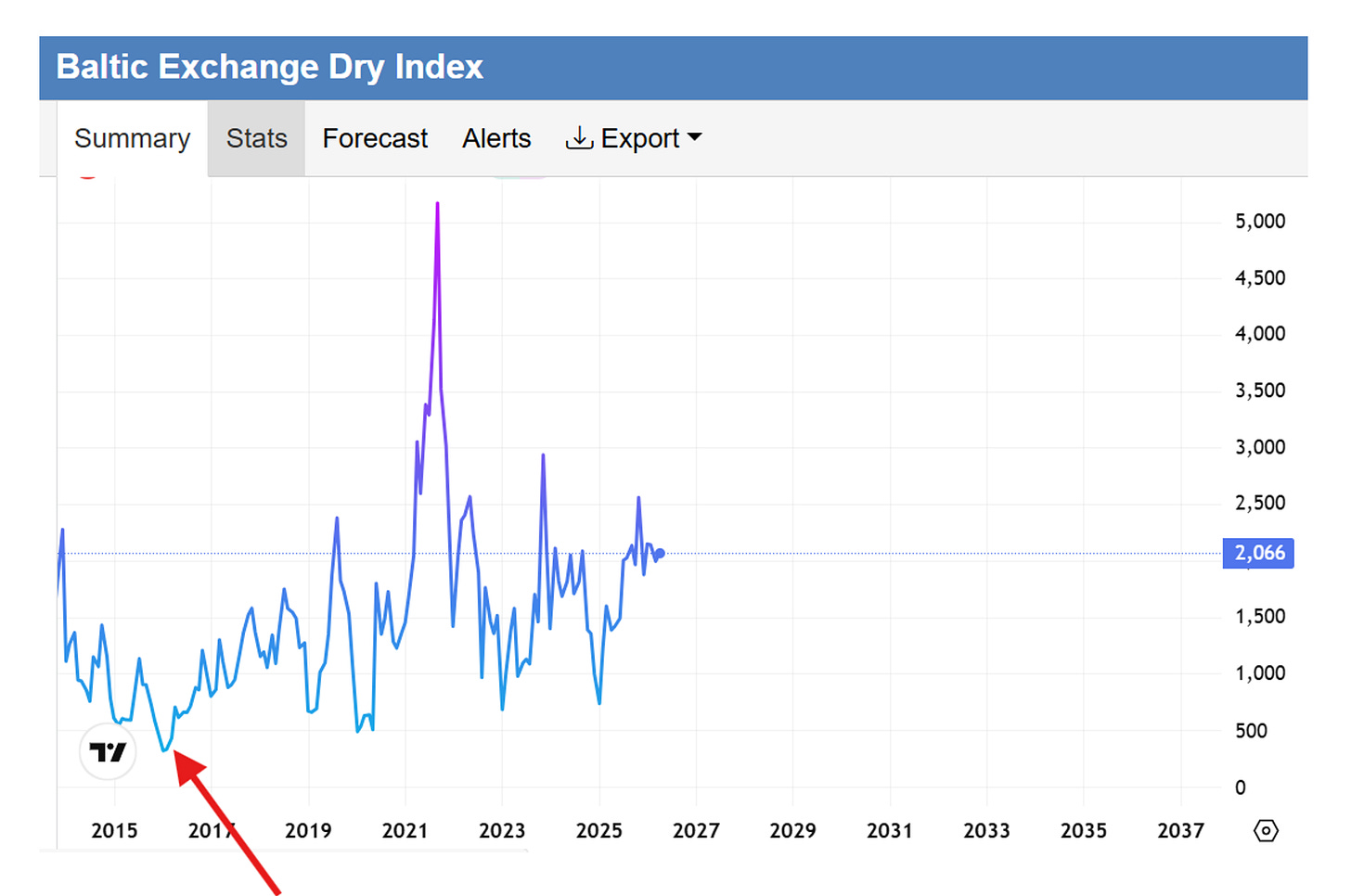

In 2016, the dry bulk rates were almost at all-time lows (10), and the assets were extremely depressed:

Source: Trading Economics

The dry bulk shipping company SBLK started to invest heavily in the acquisition of distressed fleet and thereby positioned itself for a future recovery:

Source: Internal analysis based on SBLK reports

As you can see, the yearly capital expenditures for acquiring distressed assets were reaching almost half a billion per year, but in 2017, the cash flow from operating activities improved.

That is a perfect example of monitoring the market to buy distressed assets at low prices and increasing the probability of high future returns. There are plenty of examples of this kind of successful cases, such as Frontline, as well as Scorpio Tankers, and, of course, the pioneers of shipping, private Greek owners who do not have the pressure of shareholders.

Conclusion

The investment decision for the expansion of the fleet is one of the most crucial decisions that any management of a shipping company or any investor can make. However, it is not an easy one, but if done via due diligence, the company can reap good benefits from buying distressed assets at low prices. It is very similar to value investing in equities or real estate.

We also saw an empirical and academic analysis in various papers, which showed that assets bought at the peak prices lead to lower future returns, and as a proper capital allocation rule, any value investor/management should avoid purchasing assets such as vessels, equities, etc., at their apex levels.

If you have any questions, please contact me or leave comments, and I shall do my best to shed light on the matter.

Thank you for reading,

Value Investor in Shipping

Disclaimer: It is not financial advice but a research-based fundamental analysis.

Substack link: https://valueinvestinginshipping@substack.com

Sources:

1 https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

2 https://container-news.com/top-11-liner-operators-to-receive-89-large-vessels-in-2023/

4 https://investor.maersk.com/static-files/3676346f-38c4-430d-8c28-054919aec478

6 https://www.sciencedirect.com/science/article/abs/pii/S221053951930197X?utm_source=chatgpt.com

7 https://www.sciencedirect.com/science/article/abs/pii/S0304405X14002323

8 https://www.nber.org/papers/w7008

9 https://www.econstor.eu/bitstream/10419/312372/1/1900879433.pdf?utm_source=chatgpt.com